Summary

- Euro periphery spreads continue to come in

- U.S. 10-year yield 10 bps higher

- German bund 8 bps higher

- U.S. curve 4 bps steeper on the week

- U.S. credit continues to rally. Watch this space

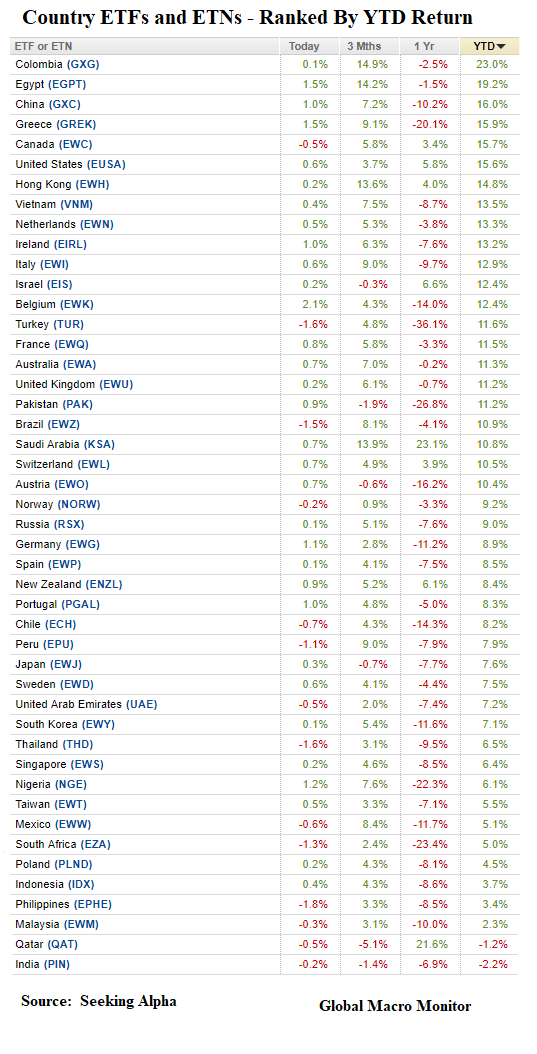

- EM FX x/Asia weaker led down by Brazil

- China and Euro stocks outperform global equities

- Major Latin stocks hit hard

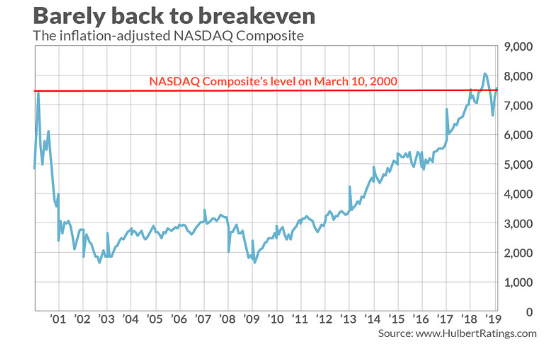

- Nasdaq outperforms U.S. major indices

- Financial conditions continue to loosen

- Natural gas leads commodity complex higher, now up almost 11 percent since we cited the “widow maker” was freakishly low and deserved a “stab”

Commentary: The S&P500 was able to close above the 2800 level for the first time since November 8th, which is was huge. The highest close since the Q4 crash is 2813.89 on November 7th. The highest intraday level is 2816.94, which was tagged on October 17th. The stock rally is confirmed by the credit markets with spreads coming in and it does appear 2816 will be taken out sometime soon, making the path of least resistance higher and a new high. The biggest risk is that POTUS and/or President Xi gives us a negative surprise on their trade deal.

We are watching the National People’s Congress in Beijing this week; comments from Mario Draghi at the ECB meeting; retail earnings in the U.S, including Costco, Target, Kroger, and Dollar Tree. Salesforce will be big in the tech schpace, and the economic data culminating in nonfarm payrolls on Friday. Also, keeping an eye open for German factory orders, Italy GDP, and China trade balance.

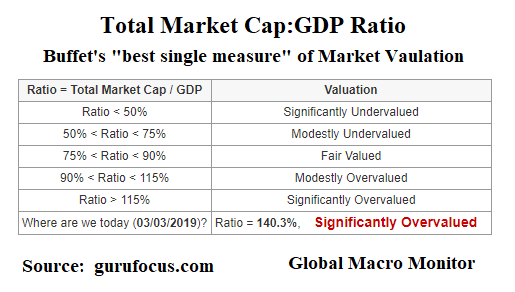

Though the short-term trade looks to be higher, and almost everyone is on board, by the way, we are watching the 10-year note yield carefully as we maintain a rise in real long-term interest rates is what concerns the market most. Our view remains that long-term investors should be selling into strength, reducing risk, and waiting for a yuge wash out. Valuations are at or close historical extremes as measured by the Buffet Indicator below and the major shifting geopolitical/economic tectonic plates are moving the wrong direction to put on long-term equity risk. Waiting for much lower prices.

Let the traders be traders.