Codependency is characterized by a person belonging to a dysfunctional, one-sided relationship where one person relies on the other for meeting nearly all of their emotional and self-esteem needs. It also describes a relationship that enables another person to maintain their irresponsible, addictive, or underachieving behavior. — Pysch Central

Preface

Let us preface this post by first stating, thank goodness the central banks, especially the Fed, for their bold and decisive actions during the Great Financial Crisis (GFC). Their behavior prior to, and after the GFC is more suspect but we know how close the global markets came to a total collapse, not just once but many times during the crisis. This comes from our sources at the highest levels of policymaking.

Collapse, not as in the S&P500 falling another 20 percent, but a complete meltdown of the global payments system, rendering trade in goods and services in the marketplace almost impossible. The hijacking of Safeway trucks and martial law probably only a few days later.

Maybe the Fed could have done things different, more effective, more efficient, and more sustainable but act they did and kept most of us from living under a freeway and eating bark for the rest of our lives.

Stay with us if you disagree for the rest of the post. We are willing to listen to your arguments if you have better information. We are very confident in ours.

One of our twitter mates, who resides in the home country (led by a man named Justin) of the team that stole the NBA championship from our Warriors, tweeted out the WSJ article with the above headline.

We immediately replied with something close to the following but with much fewer characters,

When will the central bankers learn? That they can’t solve structural economic problems with their limited cyclical toolbox — no matter how large, no matter how expanded.

Trying to do so only exasperates the unintended consequences, such as political stress and the blowback caused by the increasing wealth inequality. Not to mention the growing blackhole of negative yielding debt in the global bond market. We suspect the consequences of negative yields will not, let’s just say, be optimal in the long run.

Can the Fed and ECB arrest the decline in the international liberal economic order, which may plunging the global economy into a deep recession, with more quantitative easing?

We believe it would behoove central bankers to stop enabling the politicians and go on something similar to a “sex strike,” forcing governments to implement the painful but necessary structural reforms to put their economies on more stable and sustainable trajectories.

Govenments don’t like to make the tough choices, especially given the current state of the western democracies, and this would take some major stones by central bankers as bullying from political leaders would become intense.

Do you think Chairman Powell would/has passed that test?

The codendency of the monetary authorities, coupled with the addictive behavior of most governments to debt and deficits is a very toxic brew. We don’t think it ends well.

Here are some data on the unintended consequences of quantitative easing.

Wealth Ratio of Top One Percenters To Bottom Fiddy Skyrockets

(Note not all of the wealth inequality is due to asset inflation but a large portion is.)

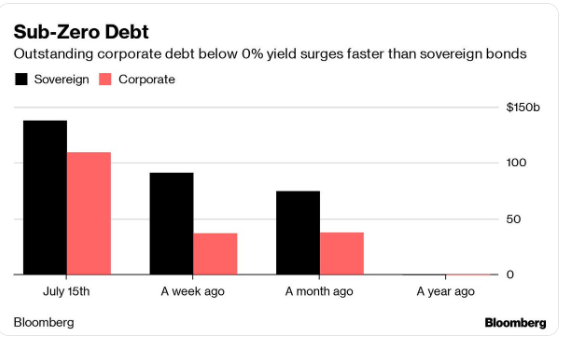

Negative Yielding Debt Spikes

EM Corporates Now With Negative Yields – Are You Kidding Me?

It’s time for the global central bankers to kick that Bear Off The Balcony At Bretton Woods and meet in New Hampshire to construct a plan to force their governments to act on structural reform.

By the way, the Raptors are a class act. Sorry to see their star leave for the Clips. Wonder if Microsoft stock was affected?

Pingback: Are Central Banks Ready To Break Their Codependency? | Global Macro Monitor