Here we go again. The Summer Friday afternoon ramp.

We posted how the S&P tends to ramp into the close in our post on Monday (see below).

No different today. The S&P had traded in a 34.44 point range high-to-low and has been ramping this afternoon. It is now, with about 15 minutes left in the cash session, 30 points off the lows, or 88 percent at the top of the range.

Please show this to the proponents of efficient markets.

Summer Fridays With The S&P500

In our July 26th post, Enter The Selling Zone, which we suspected it was time to start selling and shorting and, by the way, came on the same day of the intraday and closing highs in the S&P, we stated,

We expect the summer Friday afternoon ramp into the close, which will be an opportunity to start letting some go or setting some up. It’s hard to sell strength but much more enjoyable than selling into weakness and into a big hole. – GMM, July 26th

Summer Friday Ramp Jobs

Is there anything to our suspicions of the summer Friday ramp job into the close? Absolutely, especially during the month of July.

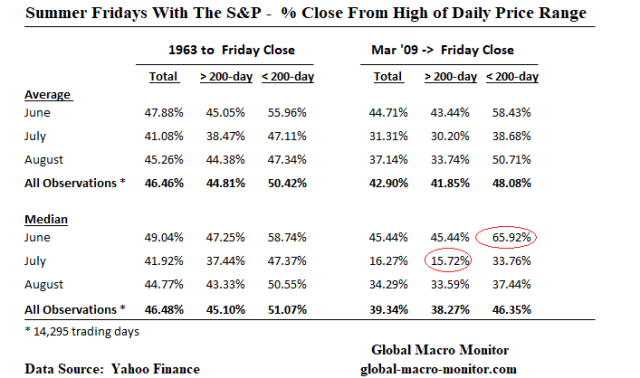

The data below show there are certainly differences from the mean and median daily closes from the high on summer Fridays. Someday when we get our firewall up, our contributors will get more in-depth statistical analysis, which should include a t-test on these data.

Data

To clarify, the data illustrate the mean and median values of where the S&P closed from its high of the day for all Fridays in June, July, and August, broken down by: 1) total observations; 2) above the 200-day moving average; 3) below the 200-day, and 4) broken out since the bull market began in March 2009. We calculated the day range from the low to high price and what percentage was the close of the day off of the high given the range.

For example, in July since the current bull market began, the median percent close from the day high when the S&P was above its 200-day moving average was 15.72 percent. That is the S&P tends to close at or near its high of the day on Friday’s in July since the current bull market began when the index is above its 200-day.

The data distribution for July is also heavily skewed, which reflects long Greek fat tails to the left. Also interesting is the June data when the S&P is below its 200-day, which we suspect reflects skittishness of traders to go home long over the weekend during illiquid summer months.

We also added data for all observations for every trading day since October 1962.

Upshot

Yes, comrades, summer Friday afternoon ramp jobs do exist, especially since the bull market began and when the S&P is above its 200-day. Efficient markets professors will argue this is not possible but take it from a practitioner, who has been trading all kinds of markets for several years: Bulls and traders love to paint the tape on illiquid Friday afternoons during the summer months.

The data show the easy money is made in July.

Stay tuned for similar analysis to come during the week.