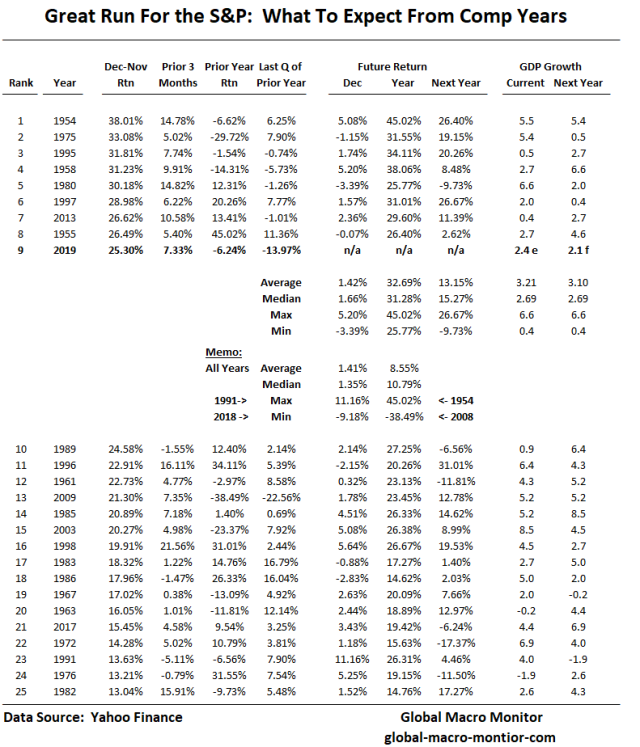

The S&P500 price index is up 25.30 percent going into December, the 9th best performance for the index from January to November since 1950. What makes this year’s rally unique to the prior big years is that it launched from the nastiest Q4 and December, in particular, in the preceding year. So in some sense, much of the rally has been a reflexive bounce back from the crash in Q4 2018 and has also been goosed by the Fed reversal to easing and big repo operations in the money markets.

What to expect in December and next year after such a great run?

We don’t know but do look too similar markets from the past for some guidance. We crunched the data and though past is not always prologue, we do know that the algos look to history for patterns in their predictive analytics and to set trading and market perimeters.

The data show that the S&P return for December in the years with such momentum in the first eleven months average a 1.42 percent, which is almost exactly what the average return is for all the Decembers in the data set (1950-2018).

Next year? The average return for S&P for the proceeding year in the eight years of 26 percent-plus returns from January to November is 13.15 percent, which is about 500 bps above the average return for the S&P for all years.

Valuations

Given that valuations are at, or close to record highs, we suspect the prospective returns that history suggests are a bit too bullish.

Source: Mark Hulbert, MarketWatch

Maybe the inertia and the increasingly positive narrative that “things are turning up” pushes the S&P a bit higher into the New Year, which of course will also be determined by I f the Chinese get their rollback on some tariffs and President Trump does not impose the new round of tariffs scheduled for December 15th.

We are waiting for a better set up to sell this market after getting stopped out at 3125.