Today’s close above 3125 takes us out of our short position, which we started scaling into at 3025. We are still fairly confident that this market can be bought at much lower prices at some point in the next 18 months. We hate getting squeezed out up here, which is probably a sign of the top and it won’t be the first time.

We’re going to the beach and patiently waiting with our long-term money and we will be on alert to the downside when the fever and market breaks. Maybe the MoMo takes the S&P up another 1-2 percent but we don’t know, nor does anyone else, and we have limited pain tolerance.

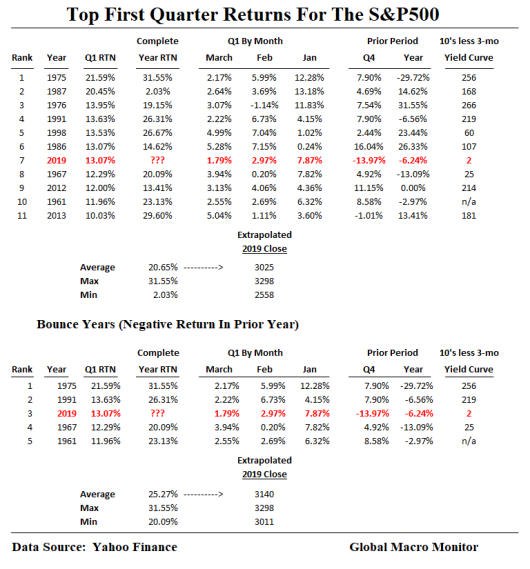

S&P500 Returns

The S&P500 closed today, up exactly 25 percent on the year. An up year after the ugly Q4 2018 crash and a subsequent strong first-quarter bounce is no surprise, folks.

There has not been one year since 1950, not one, where the S&P has increased by more than 10 percent in Q1, after experiencing a negative prior year, which didn’t close the year up less than 20 percent. It’s Newton’s Q1 Law of S&P Momentum. – GMM, April 1, 2019

By the way, the data in the above table illustrate how we calculated 3025 as the beginning of the selling zone. It was our extrapolation of the average return for years with similar short-term histories. Our trade worked out twice this year before the latest ramp.

The above data also show that this year’s strength is a mirror image of the extreme weakness in Q4 2018 but look at the yield curve at the end of Q1 versus the other years.

If the market closes here for the year, it would be the 13th best annual price move for the S&P since 1950. Another 60 S&P points higher by year-end would move it into 6th or 7th place.

Really? Does the economy and earnings justify these gains?

Yield Curve

The yield curve is almost meaningless in a world where central banks own half of the U.S. Treasury coupon curve though their positions in bills are very light historically. At the end of 2007, for example, before the Fed moved from an OMO to a QE monetary policy, the U.S. and foreign central banks held 44.05 percent of outstanding T-bills versus just 12.64 percent at the end of September. This, of course, distinguishes between repos and asset purchases on the Fed’s balance sheet.

We suspect this is a major reason for the cash crunch in the money markets. More in later post.

Why Is The Market Rising?

It is for silly reasons that the market is rising or, should we say, the prevailing narrative of why it is moving higher.

Expectations of some sort of faux-China trade deal, which we get — any cessation of economic hostilities between the two world superpowers is a good thing but the market has rallied quite a bit already. There will be no resolution to the economic competition and long-term conflict between Chimerica, which has been the main driver of corporate earnings and global growth for the past 25 years. The world economy will be much weaker than when the trade war began with no resolution in sight, and we don’t think a “Phase 1” deal is going to move the real economic needle much.

Furthermore, the Fed’s massive repo intervention (SOMA portfolio has not grown much) to stabilize the money markets is not exactly positive in our book. It is a signal the monetary distortions and huge debt issuance over the past decade are beginning to come home to roost.

Nevertheless, the markets can remain irrational longer than we can remain solvent.

The market strength has been more of a technical matter, in our opinion. Lack of supply as corporates have taken out massive stock with buybacks, the move to passive investing, and the greed & fear of FOMO.

Sustainable Levels

This market needs some very accelerated global economic growth to sustain these levels. Growth is difficult in such a highly indebted world, however, as interest rates can’t move higher to their equilibrium levels. The large stock of debt is going to act as a governor on growth as a break out in market rates will break the market and break the economy. And that, folks, is why the central banks are in their current feeding frenzy.

What will be the big negative shock that shakes the tree loose? Your guess is as good as ours but it shall come.

Cut Quick And Keep Losses Small

Our total loss in the short position is a little over 2.3 percent. Keeping losses small allows you to fight another day. We know it’s pretty tight stop but that’s the downside of playing with leverage.

Moreover, we are more comfortable to be flattish and missing another, say, one or two percent but will continue to move our target sale prices higher and wait for the market to break.

As my first trading boss on Wall Street used to preach to me almost daily, ” I don’t like being long when the fundamentals are not supportive. The bottom can drop out of the market.”

Hear ya’, boss.

On to the next trade and, now, it over the woods and through the snow and to Grandmother’s house, we go.

Have a great Thanksgiving, folks.

Pingback: S&P’s Great Run…What Next? | Global Macro Monitor

Pingback: Beware Of Market Tops And Trump’s Race For Stock Market History | Global Macro Monitor

Pingback: Two Charts Keeping Us On The Beach | Global Macro Monitor

Pingback: Stages Of A Pandemic: Denial, Panic, Fear, and Rationality | Global Macro Monitor

Pingback: Context and Stock Valuations | Global Macro Monitor