This commentary will necessarily be speculative. Trading this week will likely be dominated by the breakout of war with Iran. However, markets do not trade in the short-term on logic; they trade on positioning, leverage, and emotion, often in that order. That caveat matters more than usual following the reported killing of Iran’s supreme leader. If confirmed and the result is protracted war, the event introduces an immediate geopolitical risk premium into global markets just as risk appetite was already fraying.

The setup heading into the weekend was fragile. U.S. equities were internally deteriorating despite flat headline performance. The S&P 500 was down modestly on the week, the Nasdaq Composite is now negative year-to-date, and AI-related enthusiasm has shifted from euphoria to existential anxiety. Even Nvidia’s “beat and raise” quarter failed to stabilize sentiment. Meanwhile, private credit concerns broadened, hitting software-related equities and financials.

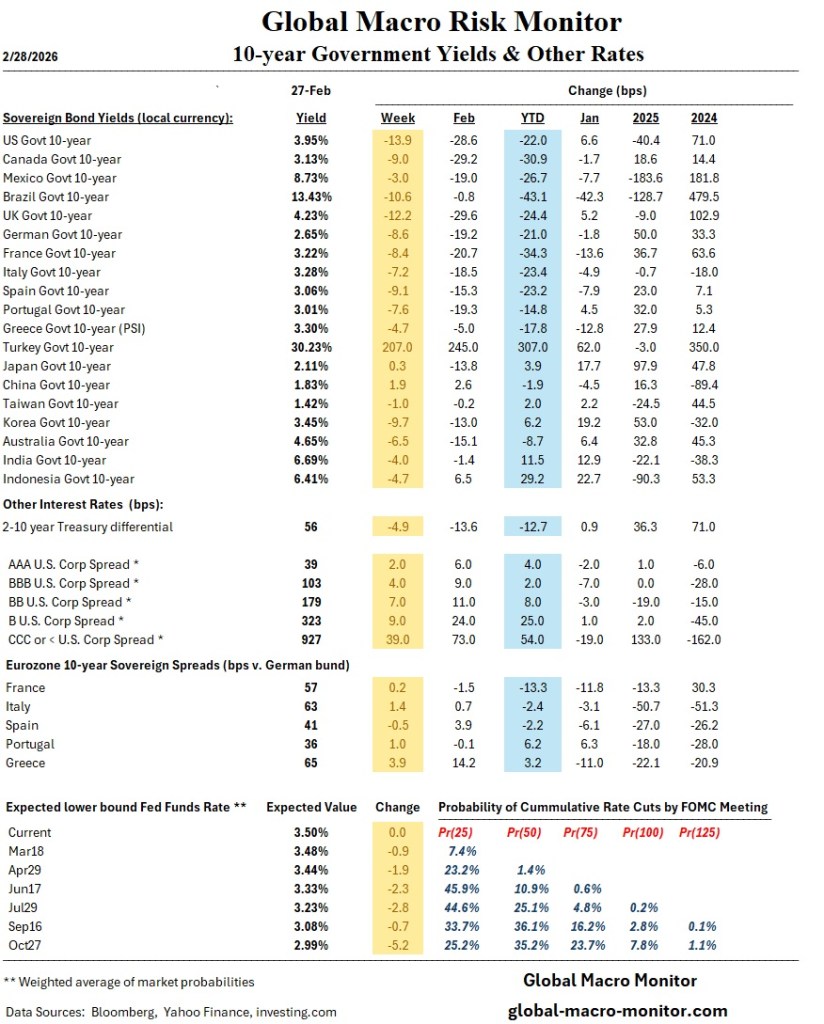

Underneath, bonds told a different story. The global bond market rallied; U.S. 10-year Treasury yields fell below 4% for the first time since November. Credit spreads widened slightly. That combination, falling sovereign yields and widening spreads, rarely signals optimism.

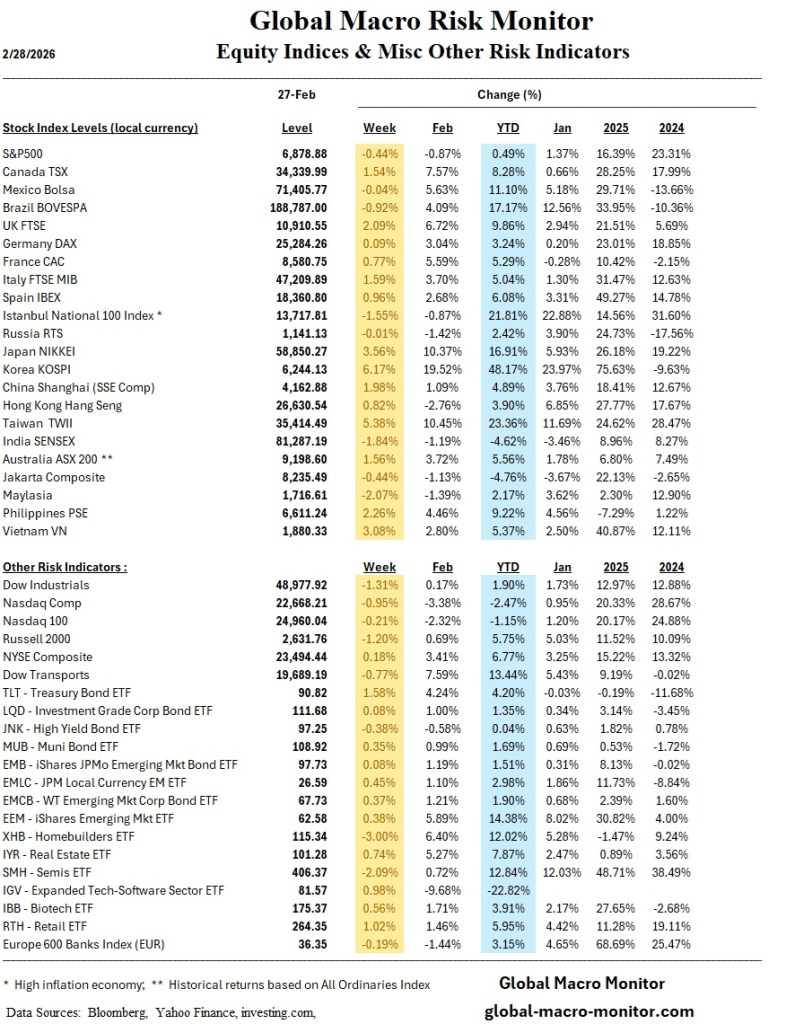

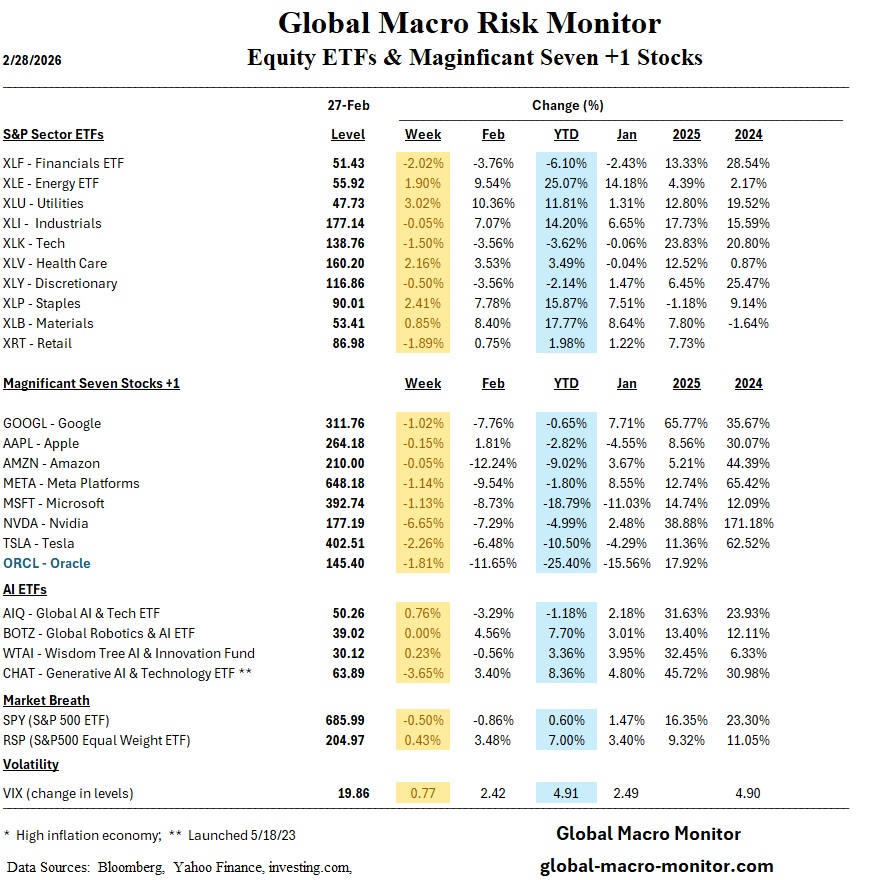

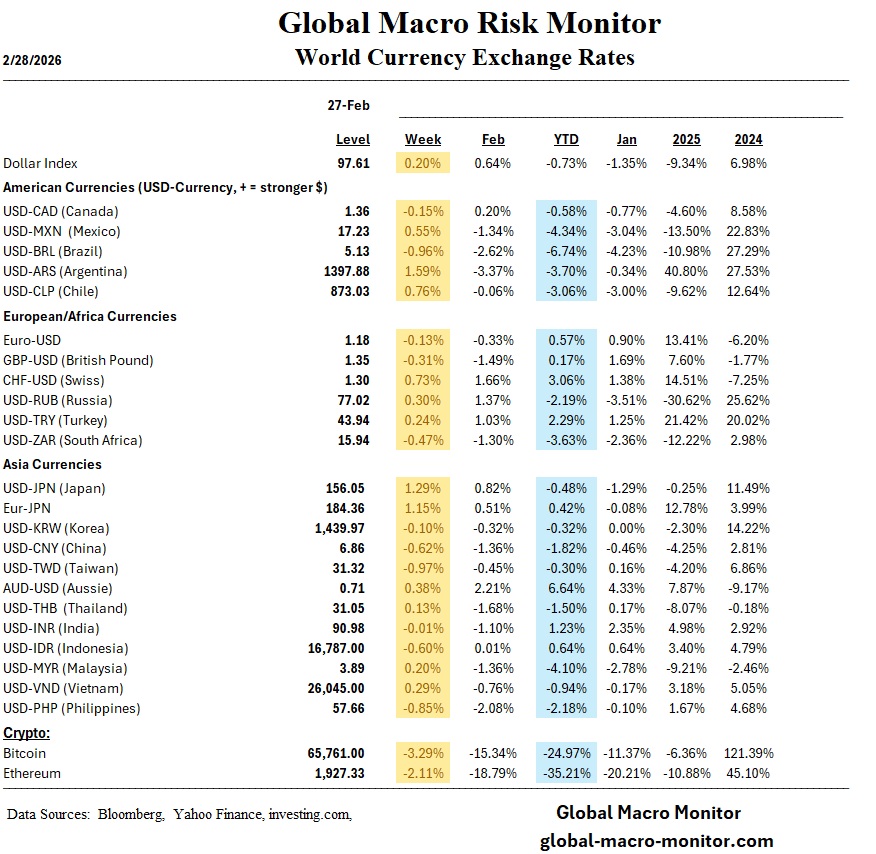

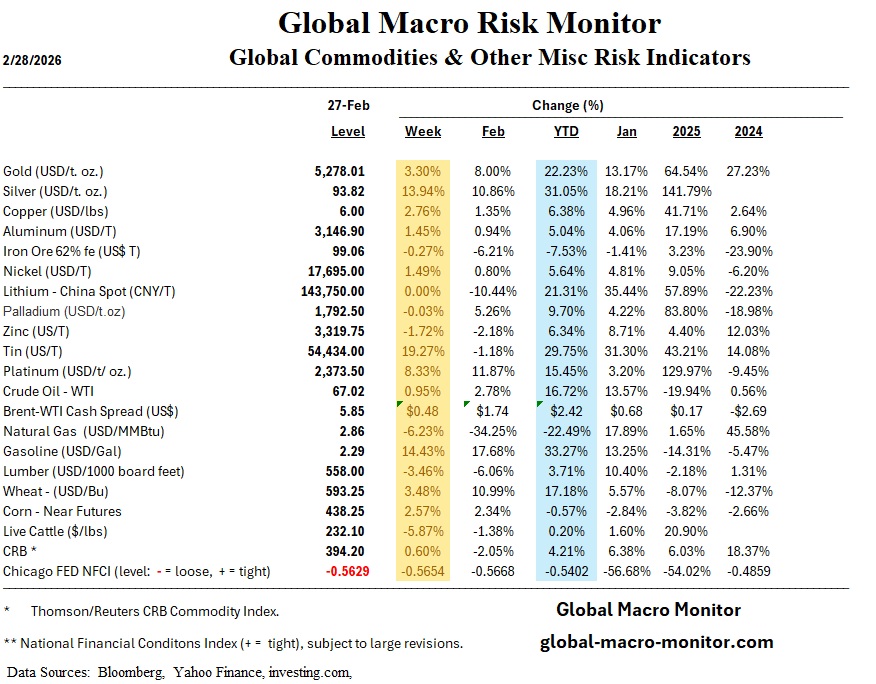

This year’s significant moves are striking. The S&P 500 ETF is up just 0.6% YTD, but the equal-weight S&P is up 7%. The Dow Transports are up 13% while the Nasdaq is down 2.5%. Energy (XLE +25%) and materials/staples (+15% range) are leadership; technology (XLK -4%) and financials (-6%) lag. The so-called Mag 7 are no longer magnificent—Microsoft down 19%, Amazon and Tesla down ~10%. Gold (+22% YTD) continues to outperform Bitcoin (-25%), a notable reversal in the “digital hedge” narrative. Traders and investors are ditching the digital hedge for “boomer rocks.”

Internationally, U.S. markets are lagging badly. Korea is up nearly 50% YTD, Taiwan +23%, Brazil and Mexico double digits, Canada +8%. Europe is grinding higher on earnings resilience.

Continued escalation with Iran risks oil volatility, further safe-haven flows into Treasuries and gold, and renewed stress in high-beta equity segments. That said, markets have repeatedly faded geopolitical spikes unless supply chains are materially disrupted. Watch the Straits of Hormuz and potential attacks on the U.S. power grid. Predicting the durability of any move is inherently uncertain.

Stay frosty, folks.

Regional Performance

United States

- S&P 500: –0.6% week; ~flat YTD

- Nasdaq Composite: –2.5% YTD

- Dow Transports: +13% YTD

- Russell 2000: +6% YTD

- Equal-weight S&P 500: +7% YTD vs. cap-weight +0.6%

- Energy (XLE): +25% YTD

- Financials (XLF): –6% YTD

- Semiconductors (SMH): +12% YTD; Software (IGV): –20%+

- 10-year Treasury yield <4%; curve flattening with global bond rally

- Credit spreads modestly wider

- Gold +22% YTD; Bitcoin –25% YTD

Europe

- STOXX Europe 600 modestly higher; new highs

- Italy and UK outperformed; Germany mixed

- Inflation trending below ECB target in parts of eurozone

- Growth stabilizing near trend

Asia

- South Korea: +~50% YTD; strongest global market

- Taiwan: +~25% YTD; semiconductor-driven

- Japan: equities higher; yen weakness and BoJ policy debate ongoing

- China: modest gains; policy easing and property support measures underway

Emerging Markets / LatAm

- Brazil & Mexico: double-digit YTD gains

- Hungary: rate cut; election risk rising

- Colombia: rising political volatility impacting FX and bonds

The Week Ahead: Geopolitics, Data, and a Fragile Tape

1. Geopolitics Comes First

Oil is the tell.

The market’s reaction to developments involving Iran will matter more than any single economic data point this week. If crude sustains a breakout above recent highs, that reinforces energy leadership and puts renewed pressure on consumer cyclicals.

A genuine risk to the Strait of Hormuz would not be a headline event — it would be a global growth event. That would force a material reassessment of inflation, supply chains, and policy trajectories.

2. U.S. Macro: A Dense Calendar

This week’s data flow is heavy:

- ISM Manufacturing

- ISM Services

- ADP Employment

- Nonfarm Payrolls (consensus expects moderation)

- Retail Sales

The narrative hinges on whether the economy is cooling gently — or proving more resilient than the Fed would prefer.

3. Rates & The Fed: Easing Narrative Under Pressure

Markets are still cautious about near-term cuts:

- March cut probability: ~5%

- June pricing: ~57% for 25 bps

But the latest PPI print (0.8% MoM core) complicates the easing story. Sticky producer prices don’t support an aggressive pivot. The bond market is watching closely — and signaling restraint.

4. Technical Backdrop: No Cushion

The technical picture remains delicate:

- S&P 500: hovering just above the 100-day SMA

- Nasdaq: rejected at its 100-day SMA; near-term bias moderately bearish

- VIX: elevated around ~21

This is not a market with strong downside shock absorbers.

5. Positioning Risk: Hidden Leverage

Under the surface:

- AI dispersion remains wide

- Private credit stress is building

- Crypto volatility remains elevated

Leverage pockets exist — and they’re vulnerable. If geopolitical headlines persist, defensive sectors are likely to continue gaining relative strength.

Bottom Line

The global leadership rotation away from U.S. mega-cap tech is real.

Bonds are signaling caution. Gold is confirming it.

If Iran escalation remains contained, markets may attempt another volatility fade. But if energy supply risk rises, today’s “orderly rotation” could quickly morph into broader risk reduction.

This tape is stable — but not sturdy.