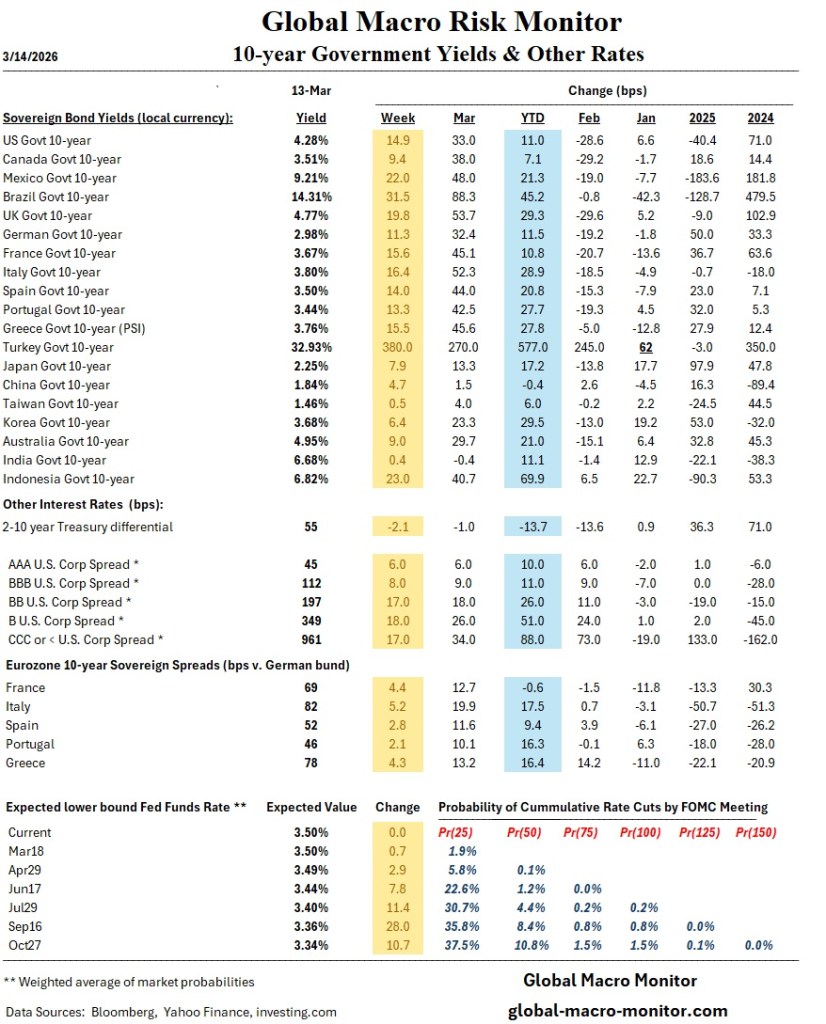

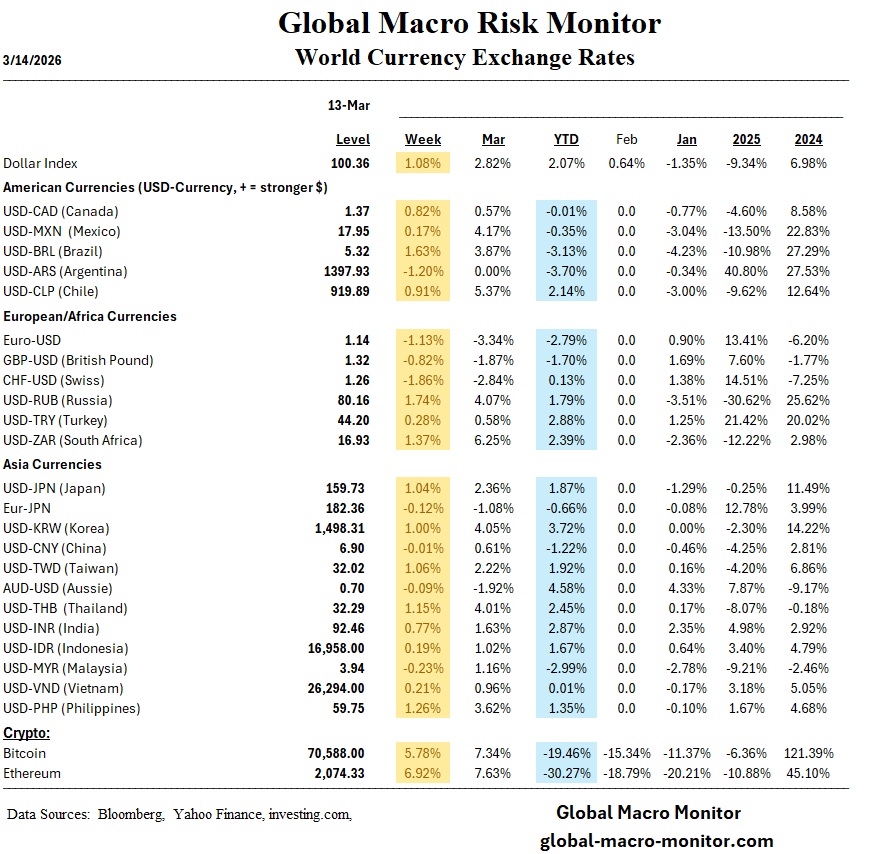

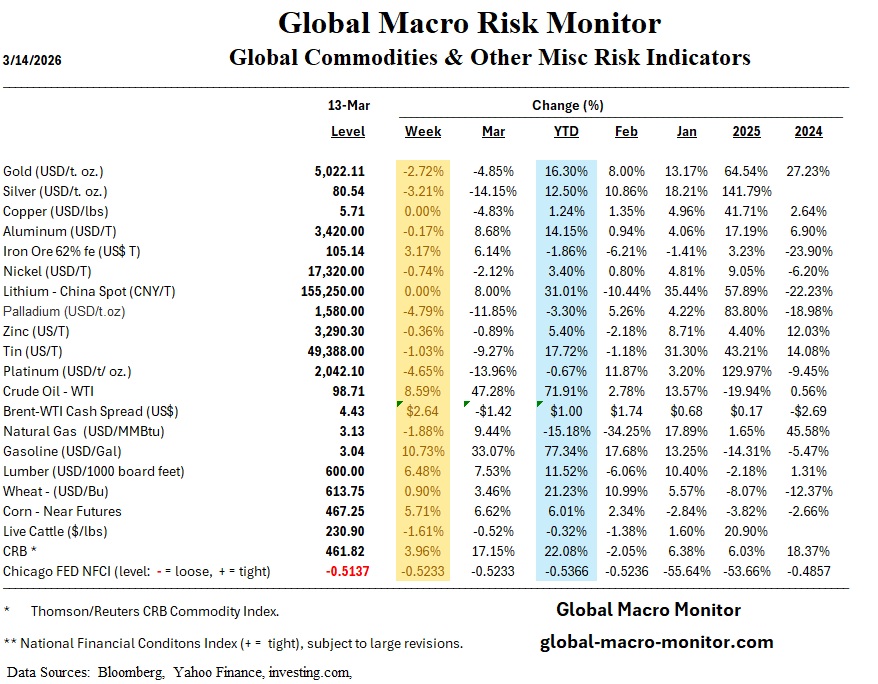

Global markets ended the week in classic late-cycle fashion: equities tried to look composed, while everything underneath them looked increasingly less so. The dominant macro transmission channel was energy. The Iran conflict and the closing of the Strait of Hormuz injected a fresh geopolitical risk premium into oil, with WTI briefly spiking near $119 before settling closer to $98 by week’s end. That oil shock pushed yields higher, strengthened the dollar, widened credit spreads, and forced markets to push out the probabilities of Fed easing to much later in the year, because stagflation worries remain the gift that keeps on giving.

The U.S. macro backdrop deteriorated at the margin. Core PCE rose 0.4% m/m and 3.1% y/y in January, while Q4 GDP was revised down to just 0.7% from 1.4%, reinforcing the uncomfortable mix of sticky inflation and softer growth. Treasury yields rose sharply, with the 10-year ending the week around 4.28%, as markets absorbed both geopolitical inflation risk and reduced odds of near-term rate cuts. Housing was mixed rather than outright broken: existing home sales rose 1.7%, housing starts gained 7.2%, but affordability remains restrictive and single-family demand is still hardly a picture of vigor.

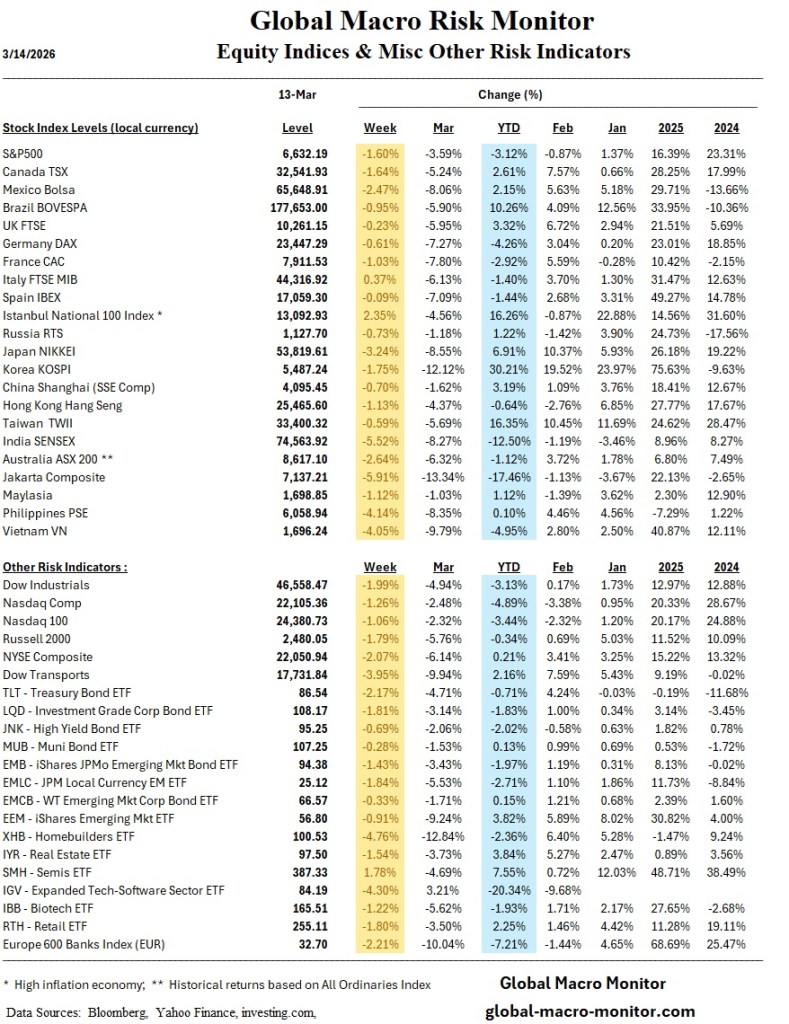

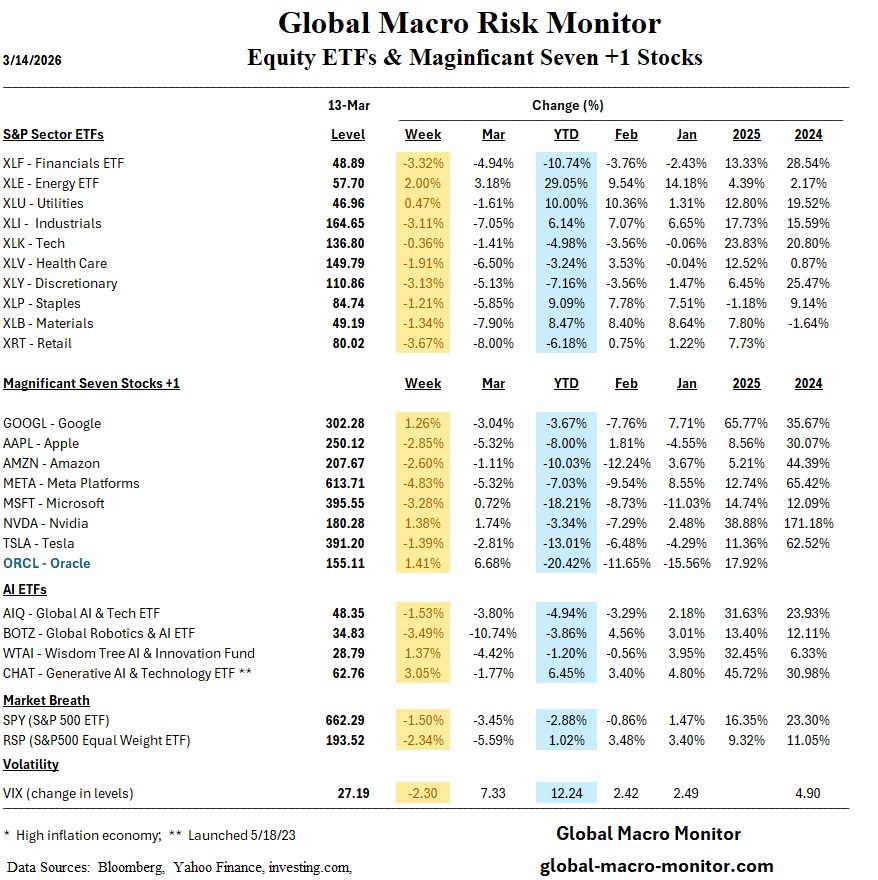

Cross-asset performance sent a clearer signal than the index-level noise. U.S. equities fell for a third straight week, with cyclically sensitive segments such as transports, homebuilders, software, and financials under pressure. Credit spreads widened, private-credit worries resurfaced, and breadth deteriorated materially. The VIX eased to roughly 27, which is less reassuring than it sounds; when markets are this jumpy and the volatility gauge falls, it often says more about positioning quirks than genuine calm. Meanwhile, commodities did what commodities do in geopolitical shocks: crude ripped higher, gasoline surged, and gold failed to deliver a clean safe-haven performance.

Outside the U.S., regional performance was uneven but revealing. Europe struggled under the combined weight of energy exposure and weak industrial data, with the STOXX Europe 600 down modestly and Germany particularly soft as factory orders and exports disappointed. The UK economy was flat in January, adding to the sense that higher imported energy costs are arriving at exactly the wrong time. Japan’s equities sold off as higher oil, yen weakness, and rising JGB yields complicated the BoJ outlook, even as Q4 GDP was revised up to 1.3%. China was the relative macro bright spot: exports surged 21.8% y/y in January-February, CPI picked up to 1.3%, and AI enthusiasm supported parts of tech, though producer prices remain deflationary and Hong Kong lagged. Latin America appears comparatively better positioned where higher oil supports fiscal revenues, though that cushion will vary country by country

Regional Performance

- United States – Equities:

The S&P 500 closed at 6,632.19, down 107.83 points on the week and -3.12% YTD. The Nasdaq ended at 22,105.36 (-4.89% YTD), while the Dow Jones Industrial Average finished at 46,558.47 (-3.13% YTD). The Russell 2000 is roughly flat for the year at -0.34% YTD. The pullback was broad-based, with transports, software, financials, and homebuilders underperforming as rates rose and oil surged. - United States – Rates & Macro:

Treasury yields climbed with the 10-year near 4.28%, reflecting persistent inflation pressures and rising geopolitical risk premiums. Core PCE inflation rose 0.4% m/m and 3.1% y/y, while Q4 GDP was revised down to 0.7%, reinforcing a slow-growth/sticky-inflation environment. Housing data were mixed: existing home sales rose 1.7% and housing starts increased 7.2%, though affordability remains restrictive. - Canada:

Canada’s economy continues to walk a tightrope between slowing growth and persistent inflation pressures. High household leverage and housing affordability challenges remain structural headwinds. Energy price spikes offer some support to the terms of trade, though domestic demand is moderating. - Euro Area – Broad Performance:

The STOXX Europe 600 fell 0.47%, reflecting weak industrial momentum and energy sensitivity. European growth continues to lag the U.S., with manufacturing data soft and credit conditions tightening. Rising oil prices add another layer of discomfort for a region already struggling with fragile growth. - Germany:

The DAX declined 0.61%. Germany’s export-driven industrial sector remains under pressure as factory orders and industrial production disappoint. Higher energy costs pose a disproportionate risk to German manufacturing competitiveness. - France:

The CAC 40 fell 1.03%, reflecting broader European risk-off sentiment and concerns about weakening consumer demand. - Italy:

The FTSE MIB rose 0.37%, making Italy a rare bright spot in Europe. The market benefited from relatively stronger banking sector performance and continued fiscal stimulus effects. - United Kingdom:

The UK economy remained flat in January, highlighting persistent stagnation risks. Higher imported energy costs and tight monetary conditions continue to weigh on growth. - Japan:

The Nikkei fell 3.24% and the TOPIX dropped 2.36%. The yen weakened to around 159.5 per dollar, while 10-year JGB yields rose to about 2.22%. The Bank of Japan signaled readiness to intervene if FX volatility accelerates, underscoring the delicate balance between monetary normalization and currency stability. - China:

Performance was mixed. The CSI 300 rose 0.19%, while the Shanghai Composite declined 0.70% and Hong Kong’s Hang Seng fell 1.13%. The macro picture improved marginally: exports surged 21.8% y/y in the January–February period and CPI increased to 1.3%, although producer prices remain deflationary. Technology and AI-linked equities provided pockets of resilience. - Hong Kong:

Hong Kong equities lagged mainland markets as global risk appetite weakened and international investors remained cautious toward Chinese assets. - Latin America:

Several Latin American economies may benefit from higher oil prices through improved fiscal revenues and trade balances. However, tighter global financial conditions and stronger dollar dynamics could offset some of these gains. - Emerging Markets – Broad Trend:

Emerging markets showed mixed performance. Commodity exporters benefited from rising energy prices, while import-dependent economies faced worsening terms of trade and currency pressures.

The Week Ahead

Markets move into the coming week with three dominant themes: central bank signaling, the persistence of inflation pressures, and geopolitical risk filtering through energy markets. Investors will be watching whether policymakers acknowledge the uncomfortable mix of slower growth and still-elevated inflation. In other words, markets are once again asking whether the soft landing narrative still holds—or whether the runway is getting shorter.

Key Macro Catalysts

- Federal Reserve (FOMC Meeting – Wednesday)

The Fed is widely expected to hold rates steady, but the real focus will be the updated Summary of Economic Projections (SEP) and Chair Powell’s press conference.- Markets will scrutinize the dot plot for clues on how many cuts remain in the Fed’s base case.

- With core PCE still running around 3%, the Fed has little incentive to rush into easing.

- Any shift toward fewer expected rate cuts could reinforce upward pressure on Treasury yields and strengthen the dollar.

- Industrial Production (Monday)

- Consensus expects modest contraction in February output, reflecting weakening manufacturing momentum.

- If confirmed, it would reinforce the narrative that global growth is slowing while inflation risks remain sticky.

- U.S. Housing Data – New Home Sales (Thursday)

- Housing activity has shown signs of stabilization due to lower mortgage rates and builder incentives.

- However, affordability remains stretched, and any renewed increase in mortgage rates could stall the recovery.

Global Central Bank Watch

- Bank of Japan (BoJ)

- Markets will monitor signals regarding currency intervention if the yen continues to weaken.

- Rising Japanese bond yields suggest the BoJ may allow further normalization of policy.

- European Central Bank (ECB)

- The ECB remains trapped between weak growth and persistent services inflation.

- Investors will watch for hints about the timing of potential rate cuts later in the year.

Commodity & Geopolitical Risks

- Oil Markets Remain the Wild Card

- Ongoing tensions surrounding the Strait of Hormuz continue to inject volatility into energy markets.

- A sustained oil spike would likely push inflation expectations higher and complicate central bank policy.

- Energy Pass-Through Effects

- Rising gasoline and energy costs could quickly translate into higher headline inflation prints globally, forcing markets to reconsider expectations for rate cuts.

Market Signals to Watch

- Treasury yields: Further increases could pressure equity valuations, particularly in technology and rate-sensitive sectors.

- Credit spreads: Widening spreads would signal growing concern about corporate balance sheets and private credit exposure.

- Equity market breadth: Continued deterioration beneath headline indices would suggest a more fragile market structure than surface-level index stability implies.

- Volatility indicators: A complacent VIX in the face of rising macro risks may indicate positioning imbalances.

Tactical Takeaways for Investors

- Expect higher volatility. Energy shocks and central bank uncertainty are rarely conducive to calm markets.

- Watch the dollar. Persistent strength could tighten global financial conditions further.

- Stay alert to cross-asset signals. Commodities, credit spreads, and bond yields are currently sending clearer macro signals than equities.

Bottom Line

The coming week is less about a single data release and more about the progression of the Iran War and the policy tone and market sensitivity to inflation shocks. If oil prices remain elevated and central banks lean hawkish, markets may need to reassess the assumption of monetary easing anytime soon. For investors, the message is straightforward: the macro environment is becoming less forgiving, and risk assets may have to work harder to justify current valuations.

Return of Principal

At moments like this, an old market line, variously attributed to Mark Twain, Will Rogers, and half the trading desks on Wall Street, starts making the rounds again:

“I’m not so much interested in the return on my principal as I am in the return of my principal.”

That quote usually resurfaces when markets stop debating valuations and start worrying about liquidity. We’re not quite there yet, but the atmosphere is changing. Energy shocks are back, central banks remain boxed in by stubborn inflation, and financial conditions are quietly tightening beneath the surface.

In other words, the cocktail for a volatility spike is being mixed right in front of us.

History suggests that when sentiment shifts from complacency to caution, it rarely does so gradually. Markets tend to move from orderly selling to disorderly liquidation faster than most risk models anticipate.

For now, investors are still giving the benefit of the doubt to the soft-landing narrative. But if oil stays elevated and rates remain sticky, that narrative could unravel quicker than expected.

So as the old traders used to say:

Stay frosty.