Alec Stapp’s chart isn’t just data—it’s a geopolitical pulse check. China is gobbling up global electricity capacity like it’s at an all-you-can-generate buffet, now pushing past 2,500 GW while the U.S. idles near 1,300 GW. That’s not just scale—it’s intent. China is building everything: solar fields that can be seen from orbit, wind farms taller than skyscrapers, and yes, still some coal, because energy security’s their religion.

Meanwhile, the U.S. is making respectable renewable gains, but in relative terms? It’s bringing a garden hose to a fire hydrant fight. China’s capacity additions are so massive they’ve turned the global clean energy transition into a national industrial strategy—and they’re winning. Fast.

Why does this matter? Because whoever electrifies fastest sets the rules. They control the tech, the supply chains, and the climate narrative. The chart is the plot twist: the West keeps talking net zero, but China’s building it—at scale, at speed, and with steel.

Ignore the chart and you’ll miss the future. This isn’t just about electricity—it’s about leverage, emissions, and economic dominance.

And right now, Beijing’s playing chess. Washington? Still arguing over the rulebook.

Anyone who has observed the last two decades of history in the Middle East would think hard about unleashing such an attack. You would want to think several steps ahead, and there is no evidence that the President has done that. His tweet and his public comments have given the impression that this is the end of war and the commencement of peace, but I suspect the Iranians think differently. – Karim Sadjadpour, Carnegie Endowment for International Peace

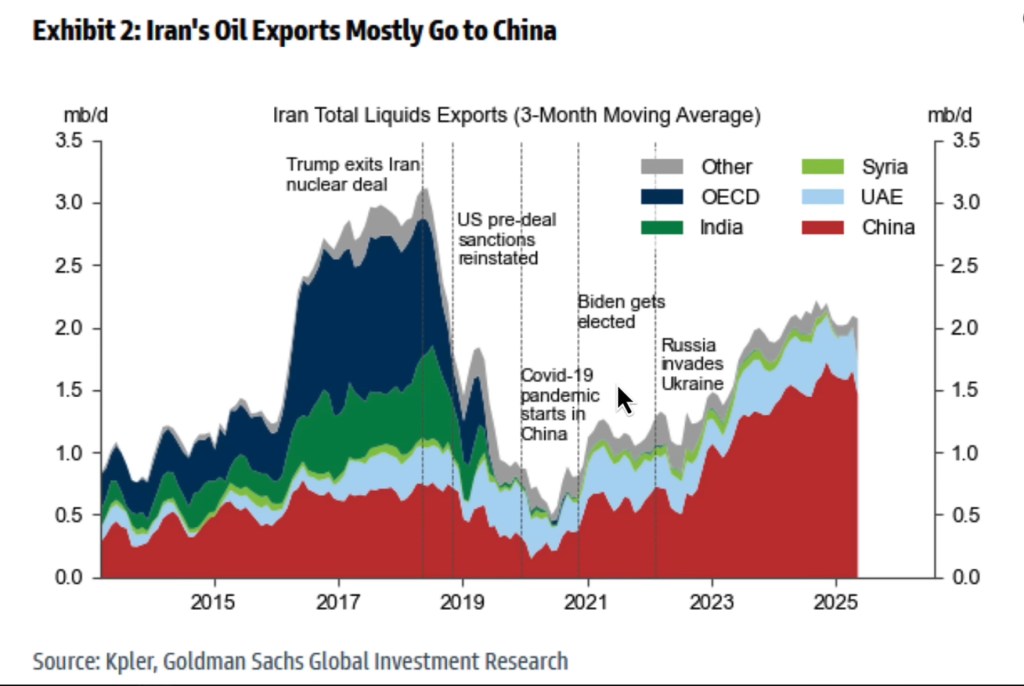

China’s role in the Iran‑Israel conflict isn’t born of strategic grandstanding, but of pragmatic energy calculus. Iran, tightly constrained by Western sanctions, has increasingly tethered its oil lifeline to Beijing, now accounting for approximately 85 percent of its oil exports. This near‑monopsony suits China: discounted crude in exchange for geopolitical reticence.

As reported by DW, Chinese foreign policy architect William Figueroa characterizes Beijing’s posture as disinterested—“no appetite to be involved”—not out of moral high ground, but capacity constraints. China lacks the regional military flexibility to act without risking broader escalation.

Still, China’s leverage through energy dependence is undeniable. Iran’s oil-for-infrastructure deals and shadowed military nods were strategically banked on Beijing’s commitment. Yet today, when conflict flares, China leans on diplomacy, not arms. It presses for de‑escalation, cautioning both Tehran and Jerusalem to respect sovereignty, even rarer is criticism of either side .

The energy dependency is a double‑edged sword for Iran. Beijing’s near‑total reliance on Iranian oil funds Tehran’s missile program and nuclear ambitions, aggravating Israel’s security paranoia. But it also binds China into a delicate balancing act: supporting Iran’s financial engine, while publicly prioritizing stability over alliance.

China’s strategic calculus is clear: high stakes in Middle Eastern energy flows, particularly through the Strait of Hormuz, where Iranian turbulence can rattle global oil markets. Yet China remains reluctant to step into the fray militarily. For Iran, this means continued economic lifelines without the military umbrella it may have hoped for .

China, the unwilling oil financier, perches on the periphery holding Tehran’s purse-strings but keeping its own hands clean. China offers Iran economic oxygen, but not military shelter, its cowed neutrality now the least risky of many bad options.

Recent intelligence from June 2025 confirms a sharp uptick in Iranian cyber activity directed at U.S. critical infrastructure, particularly the electrical grid. As Iran ramps up its offensive cyber operations, utilities and cybersecurity officials have observed increased phishing attempts, credential harvesting, and infrastructure scanning.

These intrusions remain largely within the IT domain, but their timing and intensity suggest Tehran is employing cyber operations as a deniable yet strategic tool of retaliation. Rather than risk overt military confrontation, Iran appears to be leveraging digital asymmetry to test U.S. resilience, probe for vulnerabilities, and signal resolve amidst intensifying geopolitical friction.

Ted Koppel’s Strategic Warning

Ted Koppel has long flagged the grid as a national vulnerability. In his 2017 Boston lecture, he stated: “The largest threat … is the electrical grid,” not terrorism in isolation. Lights Out pushes this further, warning that a focused cyber strike on one of the U.S.’s three power interconnections could trigger a collapse of much broader infrastructure. Koppel argues that, unlike nuclear threats, there exists no deterrent like mutual assured destruction in cyberspace, making the grid uniquely exposed.

Iranian cyber units—such as APT33 and OilRig—have demonstrated the ability to infiltrate utility IT systems through credential-spraying and phishing. While current operations remain focused on reconnaissance and IT infiltration, the shift in posture suggests a calibration phase: mapping defenses, identifying ICS/SCADA weaknesses, and building access. As conflict with Israel unfolds, the risk evolves from espionage to disruption.

The U.S. Grid’s Structural & Defensive Hardening

The U.S. grid is unusually resilient: decentralized across Eastern, Western, and Texas interconnections; regulated by over 3,200 utilities. Post-Colonial Pipeline and Texas freeze, the Department of Energy, NERC CIP standards, and regular exercises like GridEx have fortified both cyber and physical defenses. Moreover, improvements in detection, incident response, and public–private intelligence collaboration help counter emergent threats.

The Absence of Cyber “Mutually Assured Destruction”

Koppel draws on Cold War lessons; unlike nuclear arsenals, cyber platforms lack clear, visible retaliation mechanisms. The U.S. cannot credibly threaten proportional digital retaliation against Tehran. This imbalance of asymmetric risk may embolden Iran to deploy cyber tactics as a strategic lever, particularly if its kinetic options head south.

Implications & Strategic Tasks

Key Points:

Iranian cybersecurity activity is on the rise, closely tied to U.S.-Israel dynamics.

Koppel’s insights underscore the existential stakes: grid disruptions could cascade into systemic collapse.

The U.S. has improved defenses, but cyber escalation remains plausible absent stronger deterrence and attribution capabilities.

Implications:

Cyber-to-physical escalation may occur: IT breaches morphing into ICS attacks during flashpoints.

Investment in active defense, public attribution campaigns, and legal/policy frameworks for cyber deterrence is essential.

Timing is critical: If a major conflict with Iran erupts, let’s hope we have shored up our vulnerabilities, improved real-time detection, and have a credible response wrapped and packed.

Iran’s evolving cyber posture, when combined with geopolitical friction over Israel, mirrors exactly the grid-threat scenario Koppel warned against. The U.S. must no longer treat cyber as a secondary battlefield—it is now the frontline of national resilience.

We have no confidence that the current Administration has thought this through. It must be the 5D chess.

In 30 minutes, crude oil futures will flicker to life, and this isn’t just another session. With tensions between Israel and Iran hitting kinetic levels, traders are watching the Strait of Hormuz like it’s the Nasdaq in March 2020. One headline from Tehran and the whole thing re-prices. Fast.

Straight of Hormuz

Let’s not forget where we are: the Strait of Hormuz is the world’s oil aorta. Two narrow shipping lanes, 21 miles wide — Iran to the north and Oman to the south– carrying nearly 20.5 million barrels of crude per day, about 30% of all seaborne oil. If the global energy market has a single point of failure, this is it.

And Iran knows that. They’ve known it for decades.

Iran has used the Strait as both shield and sword.

1980s Tanker War: Iranian and Iraqi forces attacked over 400 tankers, dragging in the U.S. Navy. Operation Earnest Will turned the Gulf into a Cold War naval theater.

2011–2012: As sanctions piled up over Iran’s nuclear program, top generals threatened a full closure. Brent jumped, premiums widened, and war-risk insurance exploded.

2019: In response to U.S. withdrawal from the JCPOA, Iran didn’t close Hormuz—but it did detain tankers, mine the waterway, and use drones on Saudi facilities. Brent surged $10 in a matter of hours.

Notice the pattern? Full closure isn’t necessary. Tehran only needs to look serious.

From Threats to the “Taco Trade”

Now we’re hearing traders talk about the “Taco trade” again—only this time, it’s less “Trump Always Chickens Out” and more “Tactical Action, Crude Oil.” But don’t discount the political pressure valve: a spike to $120 per barrel could put the “fear of Allah” into Trump and force his hand toward de-escalation. For Tehran, the bet is simple—weaponize oil, drive markets into a panic, and make Washington blink.

It’s the idea that Iran, boxed in by regional war and domestic unrest, will use crude prices as a bargaining chip.The setup:

Hint at closure

Launch a proxy drone or detain a tanker

Send Brent up $30–$50 in a week

Let the West sweat, while Tehran tightens its grip on negotiations

Iran is considering closing the Strait of Hormuz, Iranian news agency IRINN has reported, citing key conservative lawmaker Esmail Kosari, as the conflict with Israel intensifies. – Al Jazeera

This isn’t an oil trade—it’s a geopolitical hostage negotiation wrapped in barrels.

What the Tape’s Telling Us

We’re already seeing stress on the curve.

Brent in backwardation, meaning the market is pricing tight near-term supply.

Options market loading up on $85–$100 calls.

Tanker insurance costs have doubled.

API and EIA data showing steep inventory draws.

And crude hasn’t even opened yet.

What to Watch in the Next Hour

Any fresh intel on tanker disruptions = +3–5% price pop

Western or Gulf military response = volatility spike

Diplomatic olive branch = profit-taking, but elevated floor

This is the Taco moment—if Tehran pulls the lever, every macro desk from London to Singapore will pivot from equities to energy.

Final Thought: The Strait Is the Strategy

Iran doesn’t need to win the war. It just needs to raise the price of fighting it. And that price? Measured in barrels.

Crude opens in 30. The Strait of Hormuz may already be priced for peace. But one fast boat, one drone, or one headline from the IRGC—and the whole tape rerates.

This week presented a paradox that seasoned portfolio and hedge fund managers will recognize immediately: risk is rising, but price action remains oddly composed. With geopolitical tensions escalating in the Middle East, oil surging, and inflation data surprising to the downside, equity markets continued trading with a deceptive calm, masking deeper structural vulnerabilities. Behind the headlines, the mechanics of the market tell a more precarious story: asset managers appear to be increasingly short of their benchmarks, systematic and discretionary shorts remain crowded, and positioning seems light after months of defensive hedging. As we approach Monday’s open, it may serve as a key inflection point where positioning, policy, and geopolitical risk converge. Nevertheless, beneath it all, the AI trade remains as the secular theme and trend underlying driver of markets, in our opinion.

Geopolitics and Risk Sentiment: Asset Markets Shrug—for Now Despite Israel’s direct military strike on Iranian nuclear sites and Iran’s retaliatory missile fire, financial markets barely flinched. Crude oil, however, jumped over 7% on Friday, settling at a four-month high, and gold briefly rallied. However, equity markets, including the S&P 500 (-0.39% for the week) and Nasdaq (-0.63%), showed minimal reaction. However, as Iran’s missiles fell on Tel Aviv late in Friday’s trading session, equities began to wobble with the S&P 500 closing below the key 6,000 level. According to Barron’s, even traditional risk havens such as the dollar and Treasurys saw muted inflows. The message? Investors are treating the latest Middle East clash as a headline risk rather than a macro driver, at least for now.

This complacency belies the risk of escalation. A disruption to the Strait of Hormuz could send oil prices beyond $120 a barrel, which would sharply reprice inflation expectations and destabilize rate outlooks. Strategists from Barclays and T. Rowe Price caution that the current market narrative, pricing in disinflation and Fed cuts, is vulnerable to oil-induced shocks.

Positioning Dynamics: Short Exposure at the Core The price action doesn’t reflect fear, but it does reflect fragility. Major institutional portfolios remain underexposed to equities. According to data from Manulife and Schwab, large active managers are significantly short their benchmarks, with many hedge funds maintaining net short exposures. Systematic funds, having reduced risk throughout Q2, are underweight equities by the widest margin since 2022.

That leaves markets highly sensitive to squeezes and reactive flows. Friday’s bounce in oil and slight bid in equities may not reflect conviction, but rather a short-covering reflex. Monday’s open becomes the critical test: if geopolitical risk deepens or oil pushes higher, the pain trade could swing in either direction, either a risk-off cascade from re-leveraged volatility funds or a violent rally if shorts are forced to unwind into low liquidity.

Macro Fundamentals: Mixed, Not Assuring CPI and PPI both came in below expectations, offering temporary comfort. Core CPI rose just 0.1% MoM and 2.8% YoY, reviving bets on Fed rate cuts later in 2025. FOMC members are likely to stay cautious, however, particularly given the risk of second-round inflation effects from energy. Powell’s upcoming press conference and the Fed’s Summary of Economic Projections will likely reinforce the narrative of “higher for longer with optionality,” keeping duration markets on edge. The market is pricing in a 99% probability the Fed does nothing at this week’s FOMC.

Treasury yields fell through most of the week, but rose Friday as the oil spike unsettled rate expectations. Jamie Dimon’s warning that the U.S. bond market is on track to “crack” under the weight of rising debt should not be dismissed. With the deficit now structurally over $1.5 trillion, and tax policy still used as a blunt political tool, the bond market’s patience is thinning.

Policy and Political Volatility: Structural Risk Rising Behind the immediate headlines, a more concerning trend is reemerging: the growing influence of erratic policy as a macro variable. Trump’s tariff and trade threats, including a fresh proposal to tax EU goods at 50% and Apple devices at 25%, have reignited fears of supply chain disruptions. His past business tactics, such as his aggressive yet self-defeating maneuvering in the USFL, echo today’s approach to policy: short-term vanity wins and optics at the expense of long-term system coherence.

Markets may not be pricing it yet, but these moves risk undermining global trade architecture and investor confidence. Meanwhile, China’s rare-earth export cap and renewed nationalism further complicate the landscape for U.S. manufacturers and multinationals.

Monday as the Moment of Truth Markets appear calm on the surface, but they are floating on unstable fundamentals and fragile positioning. Shorts are heavy, benchmark underweights are deep, and sentiment remains skeptical. With geopolitical tension simmering, bond market fragility rising, and oil threatening to re-anchor inflation expectations, Monday’s open will be a litmus test. Will shorts cover? Will funds re-risk? Or will volatility return with a vengeance?

For portfolio and hedge fund managers, the message is clear: stay nimble, manage tail risk, and prepare for binary market moves. The surface may look still—but the undercurrent is anything but.

Markets

U.S. Market Analysis

Equity markets finished modestly lower amid heightened geopolitical tensions and cautious Fed commentary, with the S&P 500 down 0.39% for the week.

The Nasdaq and mega-cap tech stocks showed resilience, while small-cap and cyclical sectors underperformed amid volatility in rates and oil.

Positioning remains light and defensive; large institutional asset managers continue to trail their benchmarks, and hedge fund net exposure is well below historical averages.

Monday’s open is being closely watched as a potential inflection point, given persistent short interest and asymmetric risks tied to geopolitical news flow.

Global Market Analysis

Global equities held steady despite Israel-Iran missile exchanges, suggesting investors currently view the conflict as localized and contained.

European markets outperformed slightly, supported by improving services PMIs and relief from falling inflation.

Asian markets were mixed, with Chinese equities supported by continued stimulus measures, though investor sentiment remains fragile amid weak industrial and retail data.

Oil-sensitive markets showed some resilience following crude’s rally on fears of Middle East supply disruption.

Economics

U.S. Economic Overview

May inflation data showed core CPI and PPI readings below expectations, reinforcing market hopes for a Fed pivot later this year.

Jobless claims rose modestly, and consumer sentiment dipped, reflecting cautious household sentiment as inflation moderates but wage growth slows.

Treasury yields declined on the week, driven by soft inflation and dovish rate expectations, though they spiked on Friday following an oil-driven risk-off move.

The Fed is expected to hold rates steady at the June meeting, with markets now pricing in nearly two 25-basis-point cuts by year-end.

Global Economic Overview

Eurozone industrial production rebounded modestly, but weakness in manufacturing continues to weigh on broader economic growth.

Japan’s economy shows signs of softening as consumer spending stalls and inflation expectations remain elevated.

China imposed rare-earth export restrictions while reporting a contraction in exports, signaling both economic pressure and strategic posturing.

Oil price volatility remains a key macro risk, particularly for net importers and emerging markets, with Brent crude nearing $85/barrel.

Week Ahead

Key U.S. & Global Events

The FOMC decision and Powell’s press conference will be the central focus, especially regarding the tone on inflation risk and growth outlook.

G7 leaders will meet to discuss geopolitical tensions and trade realignment in response to China’s export restrictions and the evolving Middle East conflict.

U.S. retail sales and industrial production reports will offer further clarity on economic momentum entering Q3.

Monitoring for any escalation in Middle East hostilities or new U.S. tariff announcements will be critical to assessing near-term volatility.

Upcoming Economic Data

Tuesday: U.S. Retail Sales (May), NAHB Housing Market Index