If Jeff Bezos walks into a bar, the average wealth of the bar’s patrons suddenly shoots up to several billion dollars — but none of the non-Bezos drinkers have gotten any richer. – Paul Krugman

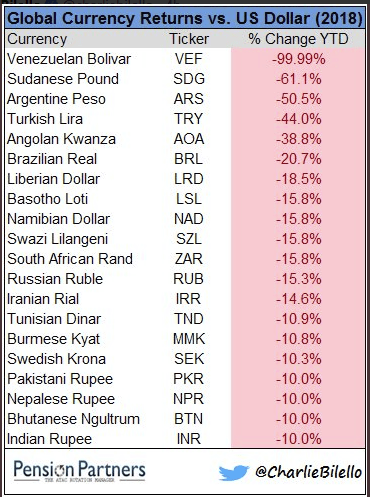

How are the indicator species of the global monetary ecosystem doing?

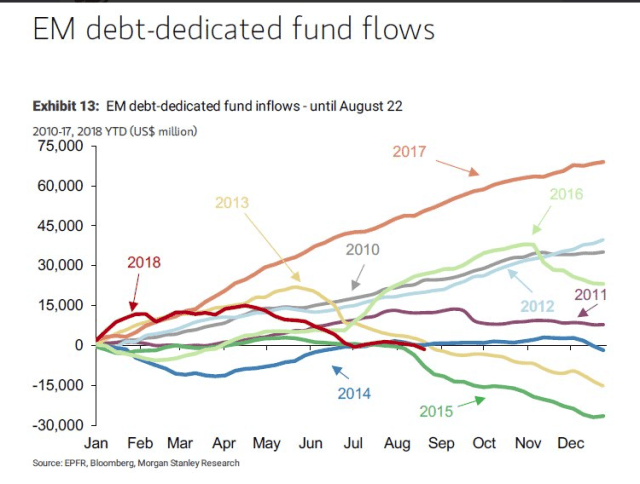

Emerging markets and commodities are the first to feel the impact of tighter global liquidity. – GMM, “Feels Like 1997,” August 15th

Charlie, once again, hits it out of the park with his excellent table.

Looks like we are setting up for a very interesting fall. Double entendre intended.

Everyday the world is legion with these acts of love and kindness.

Even the simplest of things, such as a mom or dad waking their children, making them breakfast, and seeing them off to school. These acts – what we call life — take place in both the poorest and richest of communities, and even during “the worst of times.” Kindness is universal, folks.

Maybe except NYC. Just kiddin’!

Remember this, there is more good news by almost an infinite factor — acts kindness and love – than bad news, which is what usually makes the tape and nightly news.

Keeping it real. Be kind.

After three years in foster care, 10-year-old Ivey Zezulka’s emotional reaction to finding out she would be adopted by her foster family was stemmed by not only joy, but relief as well.

And not just for herself: along with Ivey, her biological brother and sister — Kai, 3, and Lita, 2 — will also be adopted by Paige and Daniel Zezulka of Athens, Georgia. The adoption of all three children was finalized last week.

– GMA

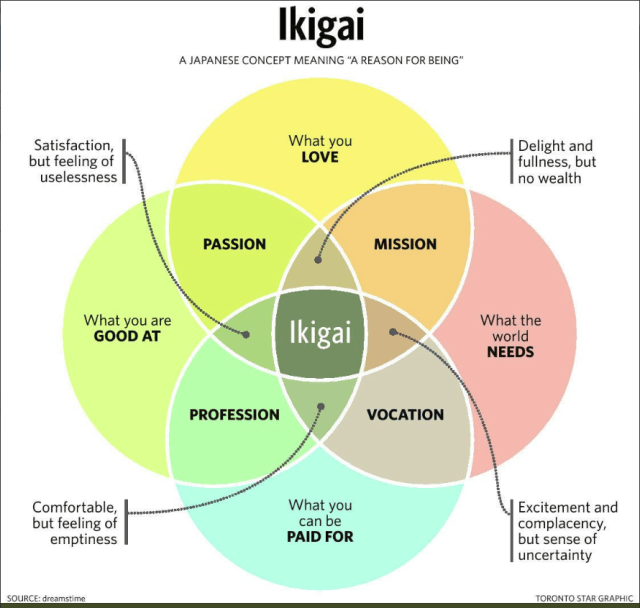

What’s your reason for getting up in the morning? Just trying to answer such a big question might make you want to crawl back into bed. If it does, the Japanese concept of ikigai could help.

Originating from a country with one of the world’s oldest populations, the idea is becoming popular outside of Japan as a way to live longer and better.

While there is no direct English translation, ikigai is thought to combine the Japanese words ikiru, meaning “to live”, and kai, meaning “the realization of what one hopes for”. Together these definitions create the concept of “a reason to live” or the idea of having a purpose in life. – World Economic Forum

Hat Tip: @tracyalloway

The Fibonacci sequence provides the mathematical basis of the Wave Principle. The stock market’s price pattern builds fractally into similar patterns of increasing size. Familiarity with these patterns can prove highly useful to investors. – Elliott Wave International

One of the greatest Americans in our history.