-

In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.

-

Join 1,215 other subscribers

Contribute To GMM

Categories

- 3D Printing

- Agriculture

- AI

- Algos

- Apple

- Automation

- Banking

- BFTP

- Bitcoin

- Black Swan Watch

- Bonds

- Brazil

- Brexit

- BRICs

- Budget Deficit

- Capital Flows

- Cartoon of the Day

- Cashless Society

- Chart of the Day

- Charts

- China

- Clean Tech

- Climate Change

- Coach C

- Commodities

- Coronavirus

- COVID

- Credit

- Crude Oil

- Currency

- Cyprus

- Daily Risk Monitor

- Day In History

- Debt

- Demographics

- Disinflaton

- Dollar

- Earnings

- ECB

- Economics

- Economist

- Egypt

- Electric Vehicles

- Emerging Markets

- Employment

- Energy

- Environment

- Equities

- Equity

- Euro

- Eurozone Sovereign Spreads

- Exchange Rates

- Fed

- Finance and the Good Society

- FinTech

- Fiscal Cliff Monitor

- Fiscal Policy

- Food Prices

- France

- Futurist

- Game Theory

- General Interest

- Geopolitical

- Geopolitics

- German Bund

- Germany

- Global Macro Watch

- Global Reset

- Global Risk Monitor

- Global Stock Performance

- Global Trend Indicators

- Gold

- Greece

- Healthcare

- Heat Map

- Hedge Funds

- Housing

- Human Interest

- Immigration

- Impeachment

- India

- Inequality

- Inflation/Deflation

- Infographics

- Innovation

- Institutional Investors

- Interest Rate Monitor

- Interest Rates

- Interviews

- Italian Yields

- Italy

- Japan

- Jobs

- Lectures

- Macro Notes from Conference Calls

- Manufacturing

- Masters

- Mexico

- Monetary Policy

- Movies

- Muni Bonds

- Muni Market

- Natural Gas

- News

- Nonlinear Thinking

- North Korea

- Overbought Markets

- Picture of the Day

- PIIGS

- PMIs

- Policy

- Politics

- Population

- Populism

- Poverty

- President Trump

- Qunat Strategies

- Quote of the Day

- Quotes

- Rare Earth Elements

- Readership

- Reads

- Real Estate

- Relative Strength Index

- Robert Shiller

- RSIs

- S&P500

- Sector ETF Peformance

- Semiconductor prices

- Semiconductors

- Social Media

- Socialism

- Song for the Week

- Sovereign Debt

- Sovereign Risk

- Spain

- Sports

- State and Local Government

- Tail Risk

- Technical Analysis

- Technology

- The Big Reset

- The Weekend Read

- This Day In Financial History

- Trade War

- Trades

- Tweet of the Day

- Ugly Chart Contest

- Uncategorized

- US Releases

- Video

- Volatility

- Wages

- Week Ahead

- Week in Review

- Weekend Reads

- Weekly Eurozone Watch

- Whales

-

Recent Posts

Meta

Confessions of ChatGPT

I was playing around with ChatGPT this morning juxtaposing comp sales from Walmart and Target. I noticed Chat gave me a 4.6 percent y-o-y growth rate for Walmart, which was not what the company reported. I asked ChatGPT where the number came from and it responded with the following. Beware of hallucinations, folks!

Q: How did you come up with the 4.6 percent comparable sales growth for Walmart?

A: The 4.6% figure I mentioned earlier appears to have been a misstatement. Upon clarification, Walmart’s actual U.S. comparable sales growth for Q3 FY2025 was reported as 5.3% (excluding fuel), based on the latest available data from Walmart’s earnings release.

Thank you for pointing this out! Walmart’s strong performance was indeed slightly higher, demonstrating robust growth across key categories like grocery and health and wellness, supported by a focus on value offerings.

Posted in Uncategorized

Leave a comment

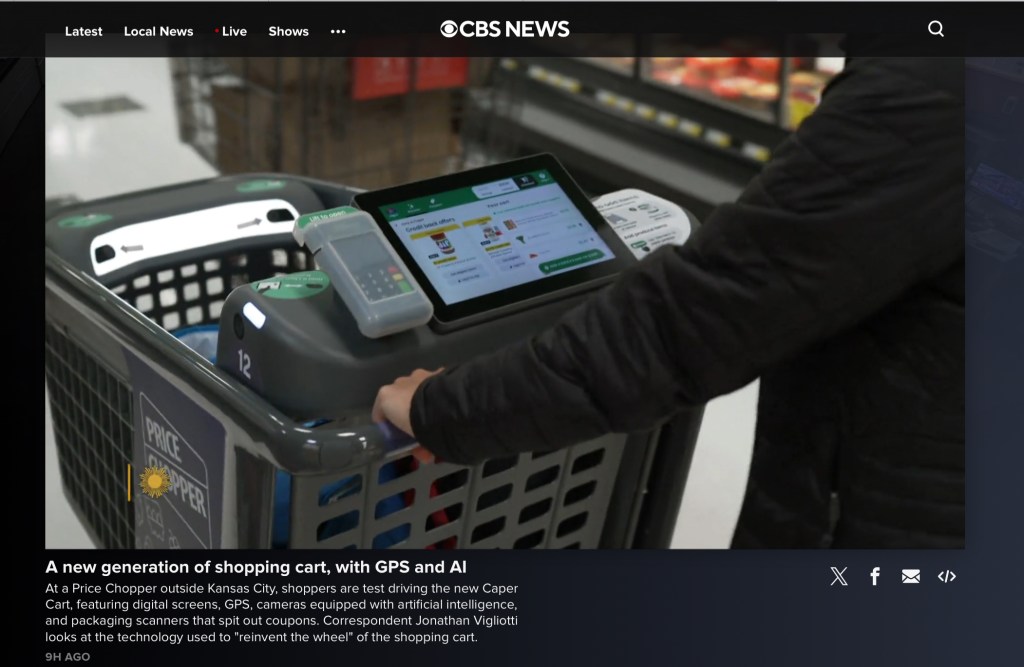

Nonlinear Thinking: Shopping Cart Disruption

Click here to view video

Posted in Uncategorized

Leave a comment

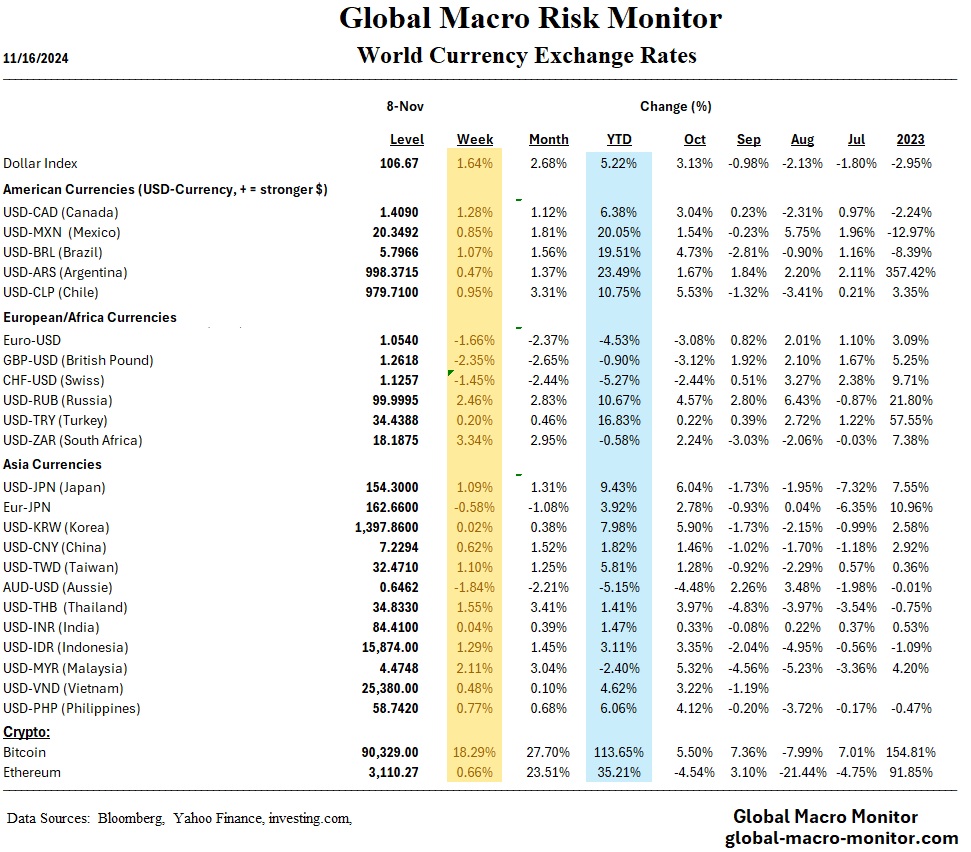

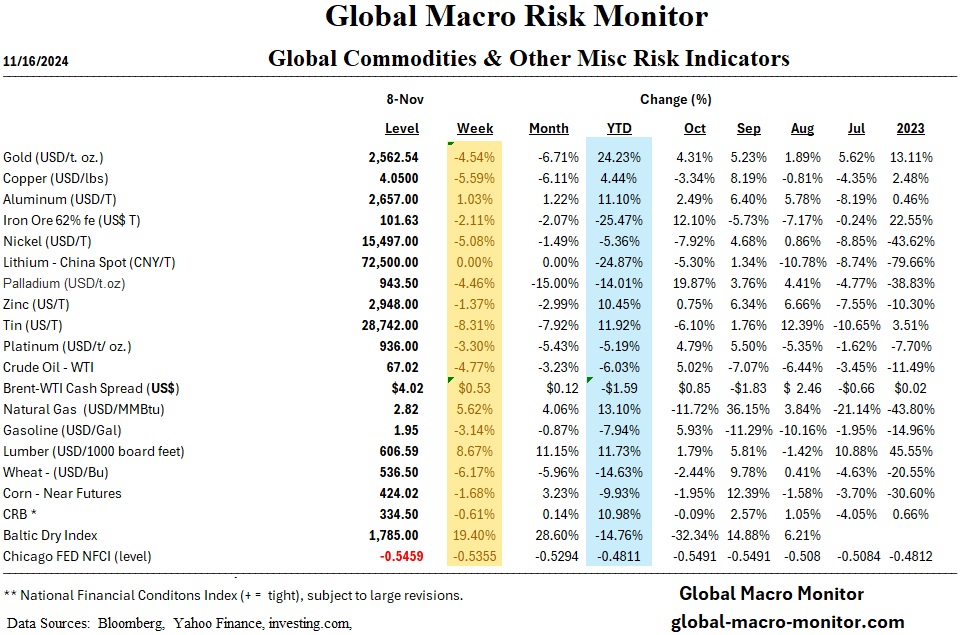

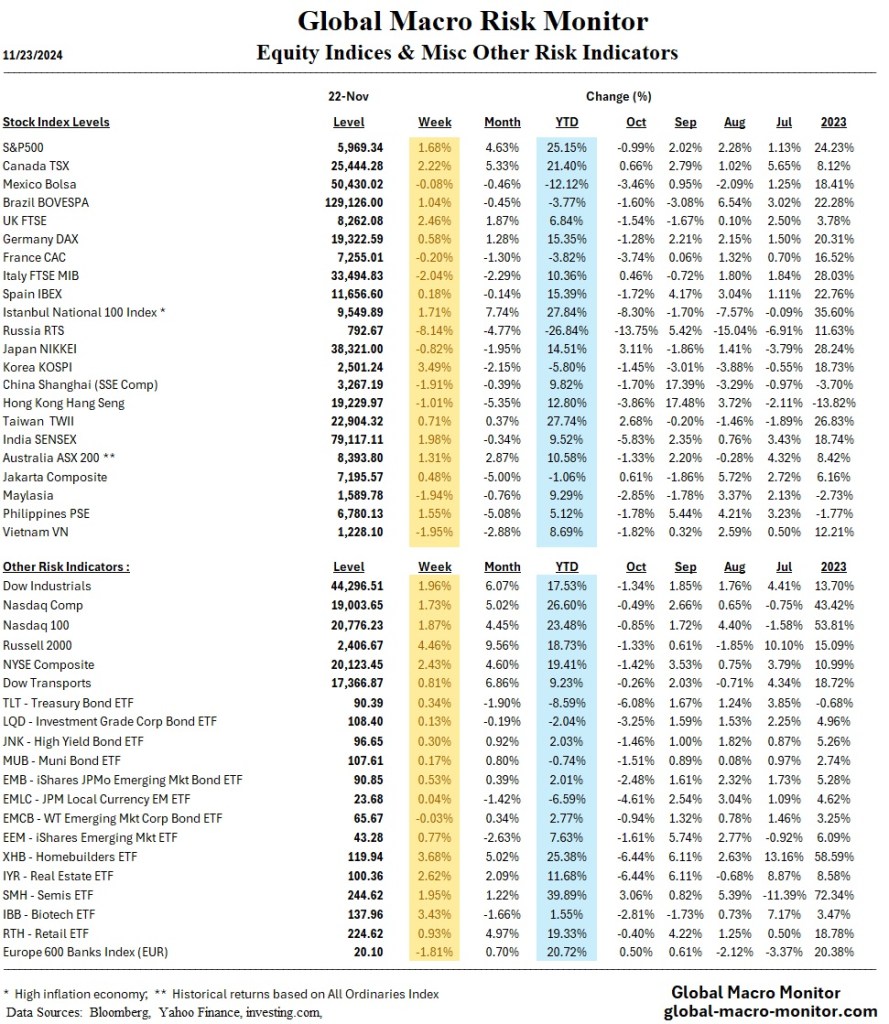

Global Risk Monitor: Week In Review – November 22

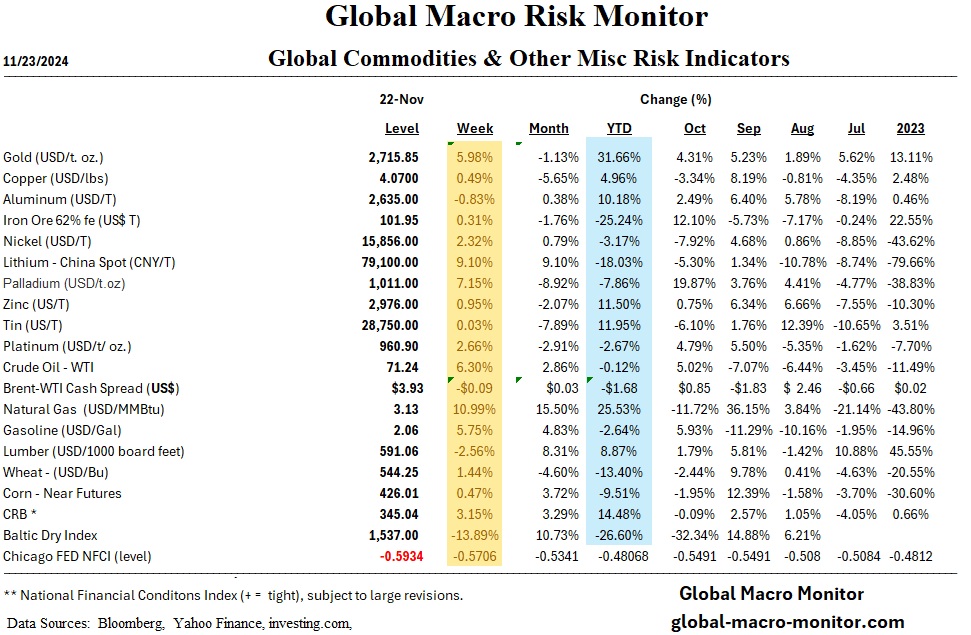

Financial conditions in the United States, as measured by the Chicago Fed’s National Financial Conditions Index (NFCI), have reached their most accommodative levels since November 2021—a period when the Federal Reserve’s policy rate stood at zero and quantitative easing was at its peak (refer to the commodities table). This shift coincides with notable market movements: gold and Bitcoin surged this week, and expectations for future rate cuts are gradually being priced out.

Of particular interest, Tesla posted a 10% rally (see Equity ETF & Magnificent 7 table), fueling what some might characterize as a “Crony Capitalism” trade. These developments underscore the dynamic interplay between easing financial conditions and market sentiment. Further shifts are anticipated—stay tuned for additional analysis.

Posted in Uncategorized

Leave a comment

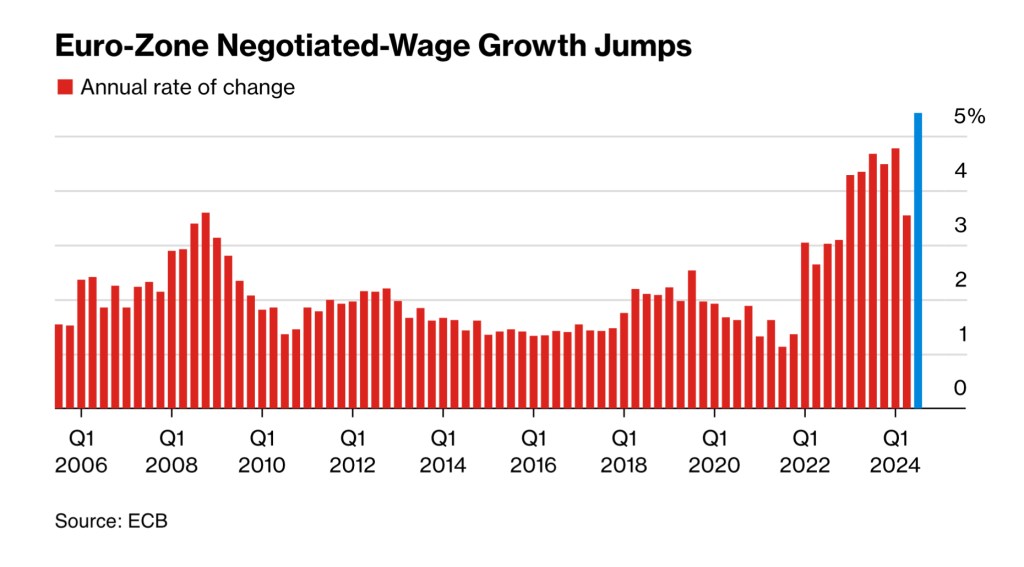

Euro-zone’s Record Wage Growth

A key gauge of euro-zone wages jumped by the most since the common currency was introduced in 1999 — complicating the European Central Bank’s plans for interest-rate cuts as inflation eases.

Third-quarter negotiated pay rose 5.4% from a year ago, the ECB said Wednesday. That’s up from 3.5% in the previous three months and was largely driven by Germany. – Bloomberg

Posted in Uncategorized

Leave a comment

The End of the Rise of China

MICHAEL BECKLEY is Associate Professor of Political Science at Tufts University, Director of the Asia Program at the Foreign Policy Research Institute, and Nonresident Senior Fellow at the American Enterprise Institute. He is the author of Unrivaled: Why America Will Remain the World’s Sole Superpowerand a co-author, with Hal Brands, of Danger Zone: The Coming Conflict with China. – Foreign Affairs

Posted in Uncategorized

Leave a comment