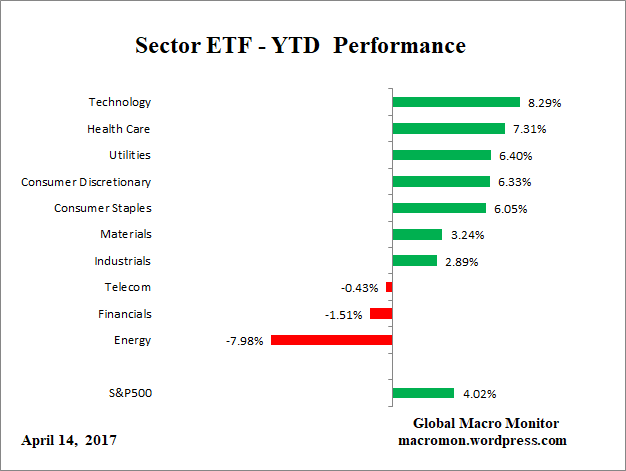

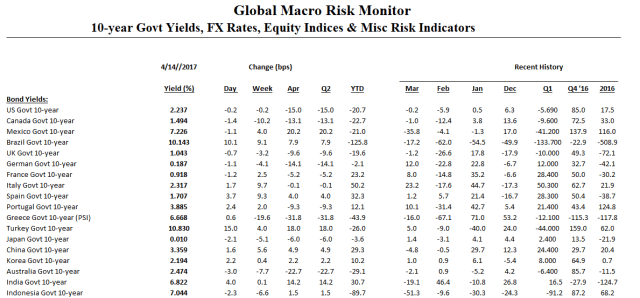

Click on table to enlarge and for better resolution

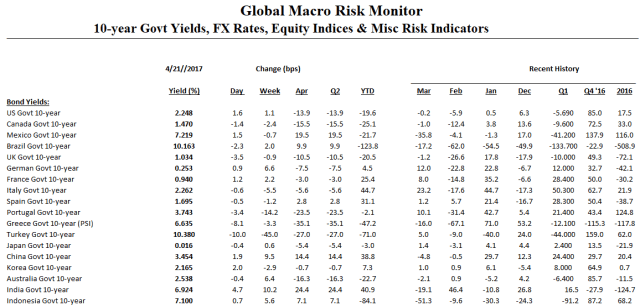

Click on table to enlarge and for better resolution

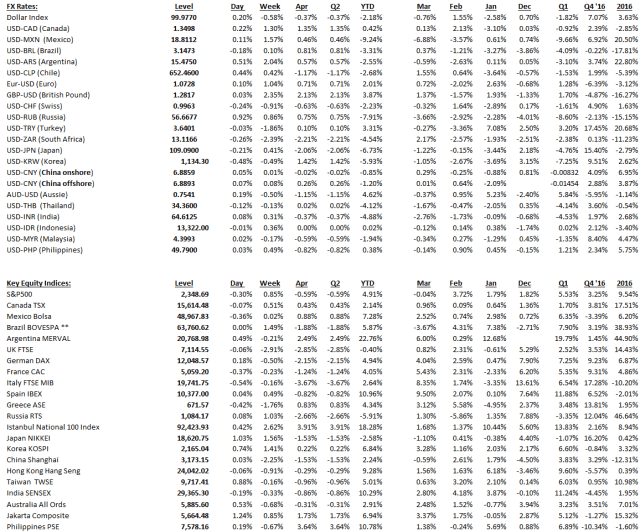

Hot from the latest International Monetary Fund’s, World Economic Outlook. Looks like not many of the projects out there making money at $50 bbl.

(COTD = Chart of the Day)

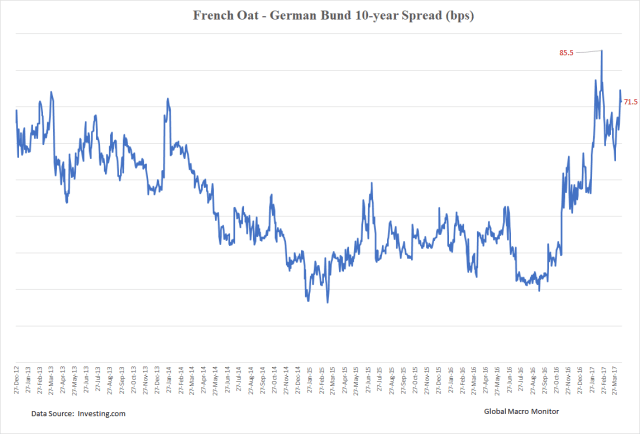

The Oat-Bund yield spread widened out about 7 bps this past week. Hard left anti-EU candidate, Jean-Luc Mélenchon, is making a late charge turning the first round of the presidential election into a 4-way horse race. Though Le Penn and Macron are ahead in the polls and favored to make the second round, their leads are just outside the margin of error. And 33 percent of French voters are still undecided.

A Mélenchon-Le Pen second round run-off would really spike volatility as the center would be up for grabs, increasing the probability of a Le Pen or Melenchon anti-EU presidency and thus an existential threat to the Eurozone and EU.

The favourites to make the second-round runoff on 7 May remain far-right Front National candidate Marine Le Pen and the independent centrist Emmanuel Macron. But with up to one-third of France’s 47 million voters undecided, and another 30% so disillusioned with French politics that they say they will abstain, the field is still wide open.

Two months ago any suggestion that Mélenchon, head of La France Insoumise (Unbowed France), could be a serious contender for the Elysée would have been thought laughable. Now it is no joke. Mélenchon’s popularity is running level with the beleaguered, scandal-hit Fillon in some polls, higher in others.

Le Monde says France is in the unusual situation of having four presidential candidates, any one of whom could win. Like Le Pen, Mélenchon is appealing to young voters with his hologram meetings, his upbeat election messages and his entertainingly forthright approach to televised debates. – The Guardian

.

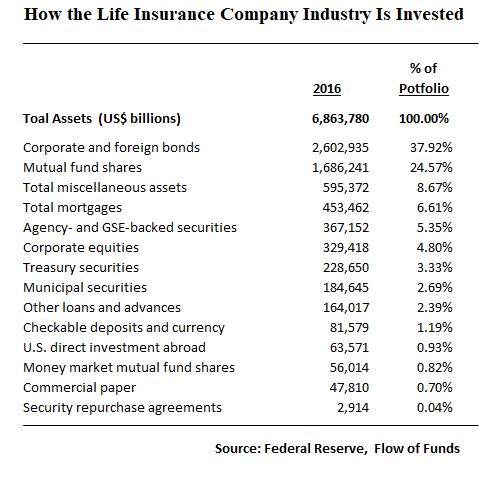

Click on table to enlarge and for better resolution

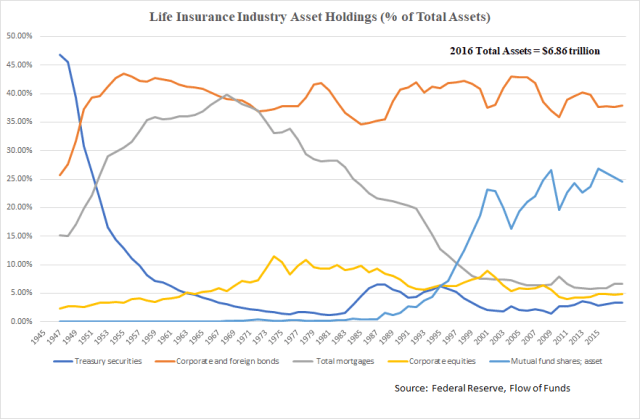

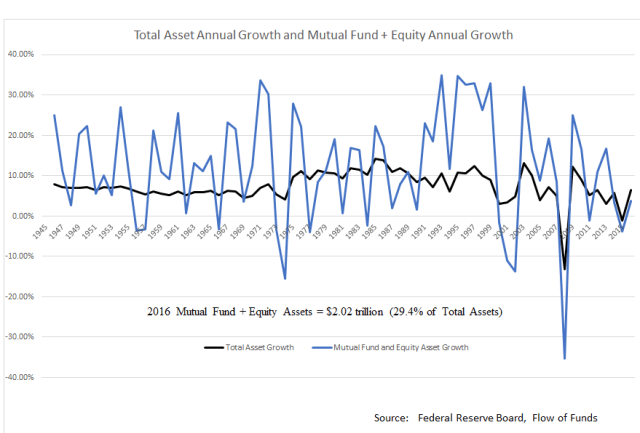

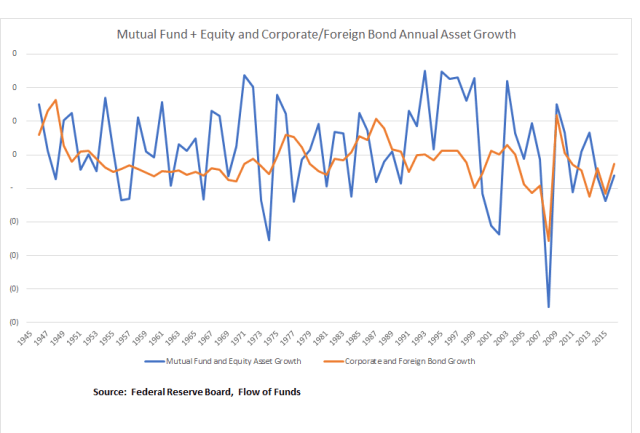

We have been busy crunching some very interesting data on pension funds from the most recent Federal Reserve’s, Flow of Funds Accounts. Check out the charts below.

Interestingly, the last time Private and State & Local Government Pensions were fully funded was at the end of the stock market bubble in 2000. Pensions were 25 percent overfunded in 1999.

However, even with stocks making new highs, these pensions remain $2.33 trillion, or 27 percent of their assets, underfunded at the end of 2016. Surprising.

One would think the slope should be headed south as stocks rise, no? Just as it was from 1995 to 2000. On the contrary, unfunded entitlements are heading parabolic north.

Could be a combination of low interest rates, an under-allocation to equities since the dot.com and financial crash (see charts) and rising pension entitlements, mainly in state and local government retirement funds. Probably more the result of the later.

The Upshot? It seems the only way out of the pension mess — other than massive contributions, tax increases, or defaults — is a humungous equity bull market with pensions appropriately positioned. In aggregate, they seem to be gun shy after the financial crisis with their average aggregate equity allocation only about 50 percent of what it was at the start and first few years of the new millennium.

One caveat is the allocation data can be distorted and deceiving as equities are measured at their market value where some of the other assets are not.

The question is: Will Janet Yellen and President Trump do “whatever it takes to preserve” the pensions? And will it be enough?

The Greek historian’s metaphor reminds us of the attendant dangers when a rising power rivals a ruling power—as Athens challenged Sparta in ancient Greece, or as Germany did Britain a century ago. Most such contests have ended badly, often for both nations, a team of mine at the Harvard Belfer Center for Science and International Affairs has concluded after analyzing the historical record. In 12 of 16 cases over the past 500 years, the result was war. When the parties avoided war, it required huge, painful adjustments in attitudes and actions on the part not just of the challenger but also the challenged.

…When a rising power is threatening to displace a ruling power, standard crises that would otherwise be contained, like the assassination of an archduke in 1914, can initiate a cascade of reactions that, in turn, produce outcomes none of the parties would otherwise have chosen. — Graham Allison