Today at CES showed us Samsung’s new flexible phone (which is also a tablet), Whirlpool’s new high-tech fire pit, and more. Take a look at some of Thursday’s highlights from the show in Las Vegas.

(click here if video is not observable)

Today at CES showed us Samsung’s new flexible phone (which is also a tablet), Whirlpool’s new high-tech fire pit, and more. Take a look at some of Thursday’s highlights from the show in Las Vegas.

(click here if video is not observable)

Note the bottoming of the M1 money multiplier after its long secular decline. The multiplier is effectively the ratio of money created by the banking system (deposits) vs. money created by the central bank (reserves).

It collapsed and fell to below 1.0 after the financial crisis resulting in the current “liquidity trap.” For every dollar the Fed “prints” — i.e., reserves it creates to purchase treasury securities, for example — the money supply (M1) increases by less than the reserve creation or expansion of the monetary base. This is because depository institutions are hesitant to expand credit and have been shrinking their balance sheets while households have been deleveraging. In addition, the shadow banking system has collapsed and effectively shut down.

The excess reserves injected through the central bank’s asset purchases are held by banks earning 0.25 percent (IOER) in an account at the Fed.

The decline in the M1 multiplier prior to the collapse was due to many factors, including the rise of the shadow banking system (securitizaton) , the expansion of activities of financial institutions, international capital flows, and financial engineering. This complicated the execution of monetary policy since Paul Volcker and led to policy errors, which partially contributed to the financial collapse and Great Recession, in our opinion.

Now with increased regulation and the lack of resurrection of the shadow banking system our sense is banking is going to get boring again, dominated by good old fashion lending. The money multipliers may well become an important indicator to think about and start to follow.

If credit markets are, in fact, healing and economic activity picking up, contemplating monetary theory and the consequences of the massive expansion of central bank balance sheets may become a higher priority of Mr. Market. We believe the money created by a healing financial system, coupled with the money created by the Fed with its planned trillion dollar asset purchase program, will provide underlying support to risk assets in 2013.

A risk the market begins to worry about the very things mentioned above and the potential for Fed panic and early exit from the super easy money is not zero. This was reflected in the market jitters after the release of the most recent FOMC minutes.

Monetary policy is increasingly dominated by fiscal policy (many can’t distinguish between the two – witness “the coin debates” — though Krugman does, however), is in uncharted waters, making it difficult to think clearly and consistent about its consequences. It’s early and we could be way off base but we think the time has come to begin focusing the issues of the money multiplier.

Keep it on your radar.

(click here if chart is not observable)

Thank goodness Ireland didn’t cave into German and French pressure to raise their corporate tax rate. We were emphatic back then they not give in to the Eurocrats (see here).

Last week’s Economist gave a nice overview of the “fitter yet fragile” Irish economy,

Helped by a low corporate-tax rate of 12.5%, Ireland continues to attract foreign direct investment (FDI), especially from American firms and particularly in pharmaceuticals, information technology and financial services. The number of new FDI projects in 2012 has been similar to that in 2011, itself the highest for a decade, says Barry O’Leary, the boss of Ireland’s inward-investment agency.

The foreign presence is now a towering one, so much so that Irish exports actually exceed the value of GDP. The contribution from net trade—exports less imports—has more than offset falls in domestic demand, which remains traumatised by excessive debt (households owe 209% of disposable income), continuing austerity and a financial squeeze as the now well-capitalised but unprofitable Irish banks limp along.

The large presence of foreign firms has sparked debate about increased vulnerability to the global economy and how economic activity should be measured. GDP or GNP?

Click here to read the full Economist article.

(click here if video is not observable)

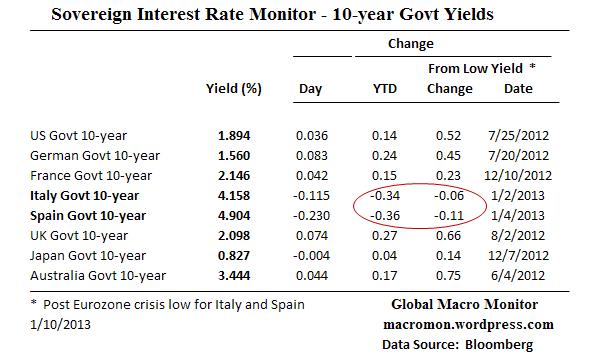

Note the big move down in Italy and Spain’s bond yields.

LONDON, Jan 10 (Reuters) – Spain’s benchmark bond yields fell to 10-month lows on Thursday after Madrid kicked off its challenging 2013 funding programme with a strongly bid auction of mostly two-year debt.

– Bloomberg

And this on the move up in core rates,

FRANKFURT—A united European Central Bank sent a strong signal that it is unlikely to cut interest rates despite economic contraction and record unemployment, suggesting the euro-zone economy must find its own footing without additional help from the central bank.

At his monthly news conference, ECB President Mario Draghi stopped short of declaring an end to the euro bloc’s three-year-old debt crisis or even that the worst has passed, saying “it’s too early” to claim success or weigh an exit from its lending to banks and other existing policies.

“We are now back in a normal situation from a financial viewpoint, but we are not seeing an early and strong recovery,” he said.

– WSJ

(click here if table is not observable)

Today at CES showed us an iPad-controlled air drone camera, a paper computer, the Pebble smart watch, Motorhead-branded headphones, and more. Take a look at some of Wednesday’s highlights from the show in Las Vegas.

(click here if video is not observable)

(click here if table is not observable)

Here’s an update and upgrade to our mid-2011 post.

Lots of noise and imperfections in the Fed’s Flow of Funds data but sure beats the alternative – nothing. The biggest caveat, in our opinion, is the data include holdings of foreign equities by U.S. residents so not a concise measure on how the U.S. stock market is allocated. Also note the household sector is a residual calculation, which includes nonprofits, hedge funds and IRAs, among other noise.

The table below illustrates a large decline in the percentage of the equity market allocated to private pension funds. No doubt there’s noise here and it may also be partially explained by demographics but the decline over the past twenty years is glaring.

The data also show the growth of mutual funds and ETFs since 1990 as households have reduced holdings of individual stocks and increased their allocation to these sectors.

(click here if chart and tables are not observable)

(click here if chart and tables are not observable)

(click here if charts are not observable)

(click here if charts are not observable)

Here is Qualcomm’s CEO Paul Jacobs giving the keynote at the CES, which included a surprise onstage visit by Microsoft’s Steve Ballmer.

“It is the first time a wireless company has opened up the Consumer Electronics Show.”

]Check it out. Well worth your time.

(click here if video is not observable)

(click here if table is not observable)