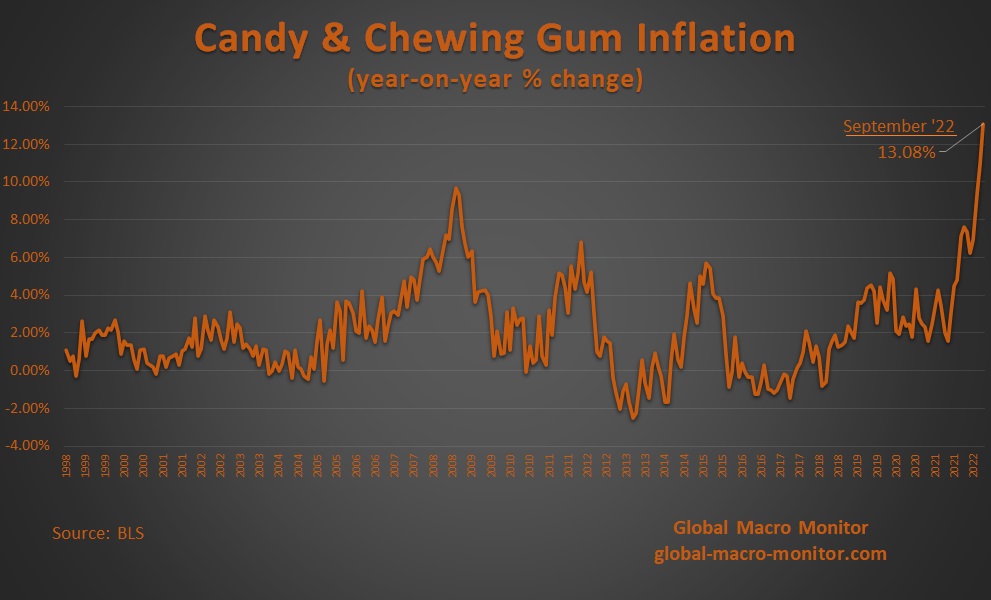

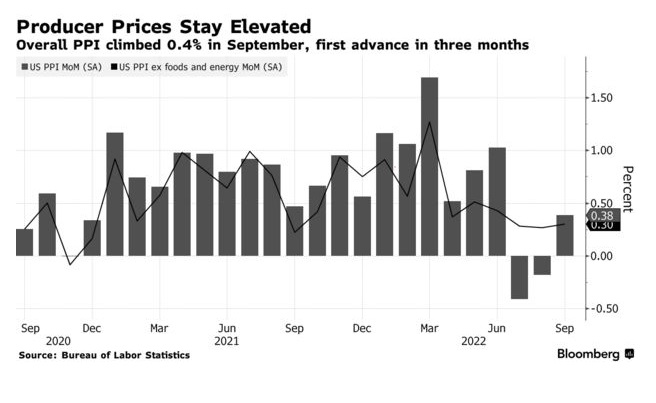

No doubt kids will be disappointed this Halloween as they empty their candy bags after a night of trick or treating and find their packages of M&Ms have shrunk precipitously, from around 22 pieces to, say, 15, as candy companies try and hide inflation with shrinkflation.

Can’t you hear the wailing next Monday night?

Mom, Dad, who shrunk my Kit Kat bar?!!!!

Check out the spike in candy prices. Try ‘splaining “transitory” to a 7-year-old. Good luck with that.

Must view, folks. So apropos to trading and investing, where one must be, all in one, an economist, financial analyst, historian, mathematician, political scientist, sociologist, futurist, and old testament prophet.

The following exchange took place between President Reagan and reporters after the market close on Black Monday, October 19, 1987. Leaving to visit the First Lady in the hospital, President Reagan spoke just after the market lost over 20 percent of its value on the day.

Q: What about the market? Tomorrow will it go down again? President Reagan: I don’t know. You tell me.

Q: Is the market your fault? President Reagan: Is it my fault? For what, taking cookies to my wife?

Q: Reaganomics?

President Reagan: I just told you. Good Lord, we reduced the deficit over last year by $70 billion. And all the other things I’ve told you about the economy are as solid as I told you. So, no, I have no more knowledge of why it took place than you have.

Thirty-three years ago today, now infamously known as Black Monday, my grandfather, M. Peter McPherson, was Deputy Secretary of the U.S. Treasury and acting Secretary that day, while Treasury Secretary James Baker was in the air traveling to Europe. McPherson was the most senior Treasury official left in Washington to handle the crisis.

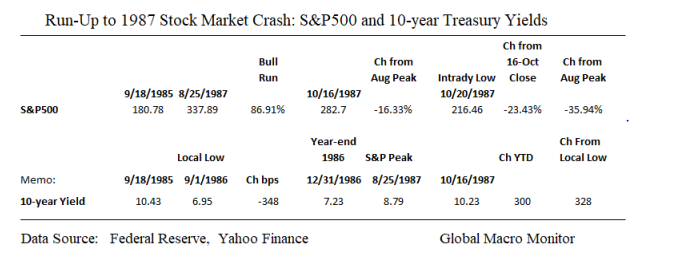

The stock market had already peaked in August after an almost 100 percent rally in the prior two years. By late August, the DJIA had gained 44 percent in a matter of seven months, raising concerns of an asset bubble, and had become very volatile as interest rates had been rising rapidly since bottoming in September of the prior year.

Similar to 1929, where the stock market peaked in early September, the markets had already begun to unravel, foreshadowing the record losses that would develop that Monday in October.

As the markets around the world began to crash, my grandfather convened with the U.S. Treasury’s Undersecretary of Domestic Finance and the Department Chief of Staff to discuss the government’s appropriate response. The Dow Jones eventually closed 508 points down, or a 22.61 percent, almost double the historic Crash of 1929, where the Dow fell 12.8 percent in one day.

Government Kicks Into Action

According to my grandfather, the situation demanded that his team put together a plan to calm the markets. The economy was doing fine, and there were no signs of recession. Real GDP growth came in at 3.5 percent in 1987.

Jitters about the U.S. trade deficit, rising interest rates, and the path of the U.S. dollar during the Plaza Accord are oft-cited as the fundamental reasons that triggered the crash, but nobody knows for sure. Trees don’t grow to the sky, and neither do markets. Stocks markets do what stocks markets do, keep their own schedule, and march to their own drummer.

The team’s conclusion at Treasury that day was the market was under severe strain for technical reasons and complicated by the new computerized program trading related to portfolio insurance. Nevertheless, the steep losses were causing significant dislocations in the financial markets.

Many large firms were under heavy liquidity pressure and were dangerously close to not making their margin calls and on the brink of failure.

My grandfather and his team placed a call to the then-new Federal Reserve Chairman, Alan Greenspan, only two months into the job, to encourage the issuance of a Fed statement that it would do whatever it takes to provide the liquidity to keep markets functioning.

It wasn’t the time to think about the policy’s broader economic implications, such as the potential moral hazard, as the plane was on fire and going down and desperately needed a rescue plan.

It was also clear Greenspan had been thinking along similar lines.

Fed officials drafted much longer statements for release, but Greenspan reasoned that a short, clear message would do the most to stabilize markets.

It is also important to point out that when Secretary Baker arrived in Europe late that day, he immediately began communicating with key finance ministers, such as those from Germany, Japan, France, and the UK to coordinate a global response to the financial crisis.

October 20

Greenspan issued his statement the next morning, October 20,

“The Federal Reserve, consistent with its responsibilities as the Nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the economic and financial system.” – FRB

In typical Greenspan fashion, the statement was vague in methodology yet resolute in purpose.

The market opened down and continued falling, there were no buyers and it appeared, at one point, the global financial system was headed for a complete meltdown.

“Tuesday was the most dangerous day we had in 50 years,” says Felix Rohatyn, a general partner in Lazard Freres & Co. “I think we came within an hour” of a disintegration of the stock market, he says. “The fact we didn’t have a meltdown doesn’t mean we didn’t have a breakdown. – WSJ

Then at about 12:38 pm, with many stocks not trading and pressure growing to close the markets a miracle seemed to happen.

With the closing of the Big Board seemingly imminent and the market in disarray, with virtually all options and futures trading halted, something happened that some later described as a miracle: In the space of about five or six minutes, the Major Market Index futures contract, the only viable surrogate for the Dow Jones Industrial Average and the only major index still trading, staged the most powerful rally in its history. The MMI rose on the Chicago Board of Trade from a discount of nearly 60 points to a premium of about 12 points. Because each point represents about five in the industrial average, the rally was the equivalent of a lightning-like 360-point rise in the Dow. Some believe that this extraordinary move set the stage for the salvation of the world’s markets. – WSJ

The rest, as they say, is history.

My grandfather felt that the Treasury’s phone call contributed to Greenspan’s thinking and as he made the decision to issue a statement to calm the market. The statement was the most critical event in stabilizing the markets and preventing substantial economic damage to the U.S. and the global economy.

My grandfather spoke about how the simplicity of the message prevented speculation while instilling confidence. Not unlike ECB President Mario Draghi’s, “whatever it takes” July 2012 speech, which saved the Euro currency, the European banking system, and ultimately the European Union during their debt crisis in 2011-12.

The Birth Of Stock Market Moral Hazard

Some argue, including one of the regular authors on this website, the Fed’s response to Black Monday ushered in a new era of faux investor confidence and the moral hazard that the central bank will always backstop falling markets. Thus, forever distorting market risk and real price discovery and contributing to the current boom-bust asset market cycle the global economy now experiences and will be extremely difficult to reverse.

Global Macro Monitor (GMM) often argues, which is not necessarily my own opinion, what was supposed to be a one-off market intervention in 1987 has now become the norm, which monetary policymakers will find it impossible to extract itself from, ultimately resulting in a major market and economic dislocation. We shall see.

President Reagan’s Confidence And Sense of Calm

During the crisis, President Reagan, whose administration my grandfather served several key roles in, was an excellent communicator and never once conveyed a sense of panic in October 1987.

Though not having a financial background, President Reagan did have a degree in economics and understood the nature of markets and how they coveted a sense of calm and leadership from the government during such a crisis.

The following video is President Reagan speaking to the press at the White House on Black Monday as he is preparing to board Marine One to visit the First Lady in the hospital.

Skip to the dialogue, which starts 5:40 minutes in.

Note President Reagan’s incredibly calm demeanor and sense of confidence after the most massive stock market crash in U.S. history.

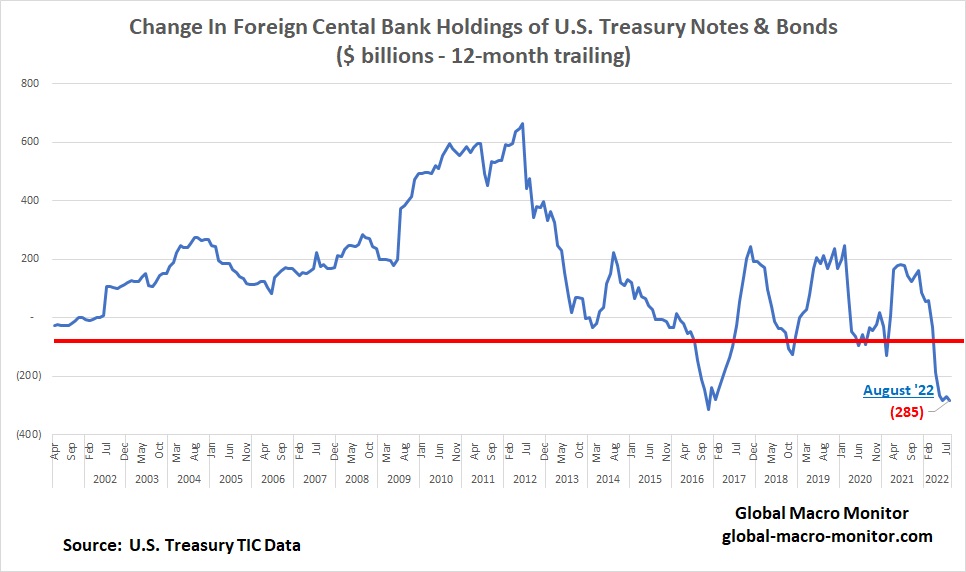

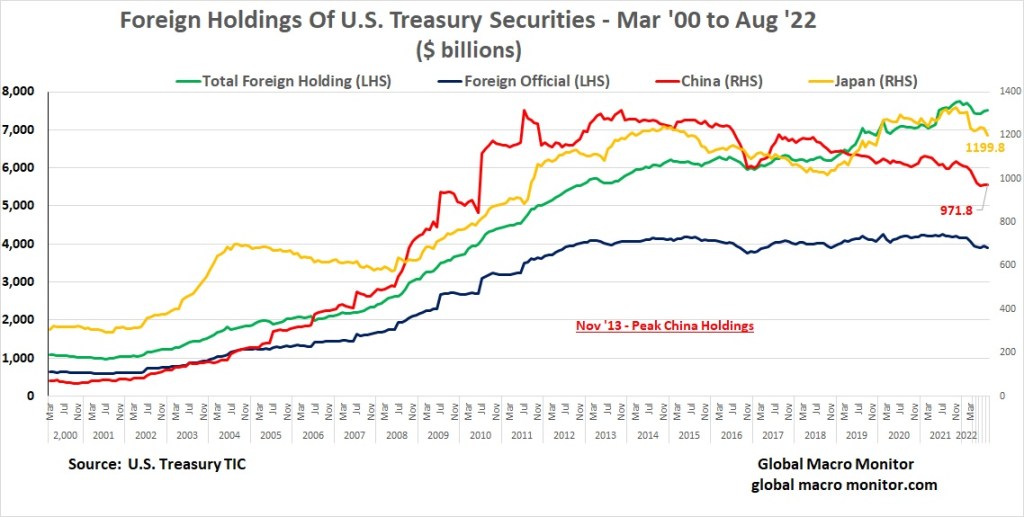

We also have no doubt Japan’s holdings are down from the latest observation in July. – GMM, Sep 29th

Japan, the country (data is aggregated), sold $34.5 billion of its holdings of U.S. Treasury securities in August. China holdings of Treasuries are down 26.2 percent from the November 2013 peak of $1.32 trillion to $972 billion in August.

Central banks have zero price sensitivity to the U.S. bond market, providing, essentially a “free-ride” in financing the U.S. government. This story is in its last chapter and has major repercussions for all markets.

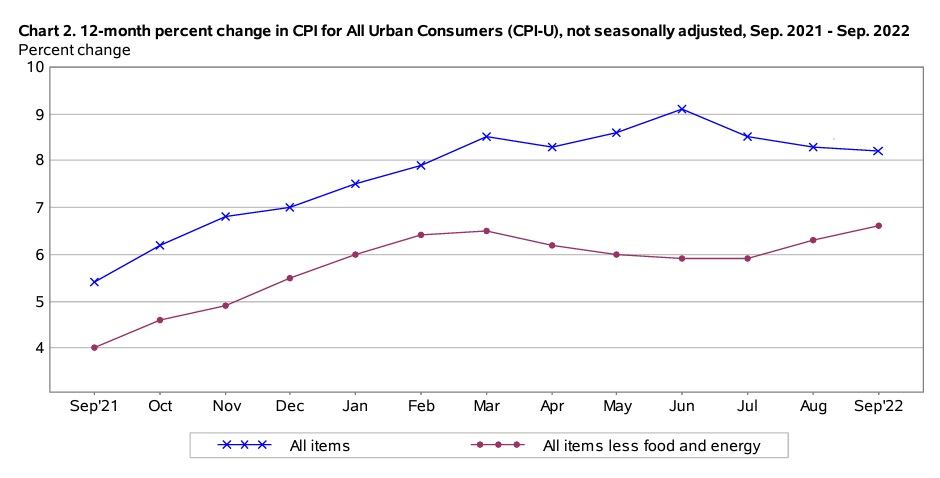

Though not the norm in the U.S., this is the type of inflation I saw in Argentina in the late 1980s for almost all goods and services and is unlikely to be the convention here unless the Fed is forced to support and finance the Treasury market. More likely today than six months ago, but highly unlikely, nonetheless.

‘It was March 2021, and the Federal Reserve Bank of St. Louis president couldn’t find the model he wanted in the local store, which was 90% empty. So he ordered online — only to be asked, when the bike was delivered four months later, for an inflation surcharge of around $200. He refused to pay, but came away distressed.

“The idea that you’re changing prices in the middle of some transaction was alarming to me,” Bullard recalled in an interview last month. “It was very telling about the environment.”’ – James Bullard, St Louis Fed President, Bloomberg

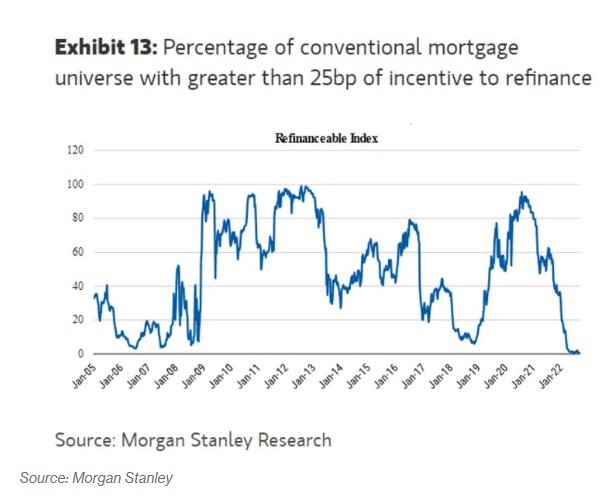

Mortgage Refinancing Bear Market

Mortgage Refinancing Bear Market