They shall beat their swords into plowshares, spears into pruning hooks, [and shipping containers into homes] – Book of Isaiah (paraphrased).

According to shipping analytics firm Windward, 20% of the world’s roughly 9,000 active container ships are currently sitting in traffic jams outside congested ports. Close to 30% of that backlog alone is in China—double the domestic congestion rate in February—where a virulent Omicron wave is snarling supply lines. – Forbes

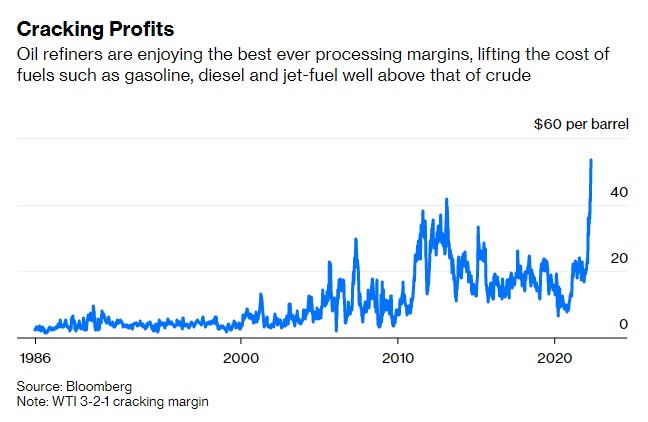

Right now, the traditional relationship between crude and refined products is broken. WTI is anchored around $100-$110 a barrel, suggesting that — in barrel terms — gasoline, diesel and jet-fuel prices shouldn’t be much higher, once you add the average refining margin.

In reality, they are a lot more expensive. Take jet-fuel: in New York harbor, a key hub, it’s changing hands at the equivalent to $275 per barrel. Diesel isn’t far away, at about $175 a barrel. And gasoline is at about $155 a barrel. Those are wholesale prices, before you add taxes and marketing margins.

…Oil refineries are complex machines, capable of processing multiple streams of crude into dozens of different petroleum products. For simplicity’s sake, the industry measures refining margins using a rough calculation called the “3-2-1 crack spread”: for every three barrels of WTI crude oil the refinery processes, it makes two barrels of gasoline and one barrel of distillate fuel like diesel and jet-fuel.

From 1985 to 2021, the crack spread averaged about $10.50 a barrel. Even between 2004 and 2008, during the so-called golden age of refining, the crack spread never surpassed $30. It rarely spent more than a few weeks above $20. Last week, however, the margin jumped to a record high of nearly $55. Crack margins for diesel and other petroleum products surged much higher.

From 1985 to 2021, the crack spread averaged about $10.50 a barrel. Even between 2004 and 2008, during the so-called golden age of refining, the crack spread never surpassed $30. It rarely spent more than a few weeks above $20. Last week, however, the margin jumped to a record high of nearly $55. Crack margins for diesel and other petroleum products surged much higher. – Bloomberg

The map [below] allows you to see the median home price for each county. Applying the House Price Index growth from FHFA to the latest housing data from the American Community Survey (ACS), we calculated a median home value for 3,119 counties and county-equivalents in the United States. Home values represent the value of all homes instead of home sales.

Here is the list of the counties with the highest median home values in the 4th quarter of 2021:

True Confessions: We don’t know, and neither does anyone else, including Chairman Powell and the FOMC.

What Is the Neutral Rate?

The neutral rate is the theoretical federal funds rate at which the stance of Federal Reserve monetary policy is neither accommodative nor restrictive. It is the short-term real interest rate consistent with the economy maintaining full employment with associated price stability.

You won’t find the neutral rate quoted on your computer screen or in the financial section of the newspaper. The neutral rate is an “inferred” rate—that is, it is estimated based on various analyses and observations. – Robert Kaplan, Former Fed Official , Oct ’18

Interestingly, Kaplan qualifies the neutral rate as the short-term “real” interest rate. We assume “real” is consistent with the convention economic definition, nominal minus inflation.

Chairman Powell recently stated:

That’s why Powell and other Fed officials have said in recent weeks that they want to raise rates “expeditiously,” to a level that neither boosts nor restrains the economy — what economists refer to as the “neutral” rate. Policymakers consider a neutral rate to be roughly 2.4 percent. But no one is certain what the neutral rate is at any particular time, especially in an economy that is evolving quickly. – PBS News Hour

It’s unlikely these “policymakers” consider a “neutral” 2.4 percent Fed Funds as a “real” rate. If so, assuming inflation falls back to 5 percent in the near term, the real neutral rate as defined by Kaplan would be 7.4 percent, about 650 bps higher.

If you haven’t noticed yet, folks, there is a lot of obfuscation in the economics profession.

Are We There Yet?

Where is the neutral rate? Let’s go to the videotape chart.

History tells us the economy has never entered a post-War recession with a negative real Fed Funds rate. The April closing real rate was -8.0 percent, and now a bit higher with the FOMC’s recent 50 bps increase in the nominal rate.

“This time may be different,” but that’s rarely, if ever, bankable.

The Fed And Mount Whitney

I backpacked up Mount Whitney, a 14,505-foot beast and the highest mountain in the contiguous United States a few times as a kid. Talk about altitude sickness!

The markets already have altitude sickness, and the Fed is barely out of base camp!

We don’t believe the volatility spike this year is because markets have suddenly become more efficient, only discounting future rate hikes, for example, as many argue. It’s much more complicated.

New World Order?

The change in monetary regime is a big part of the markets’ nauseousness, but much of the queasiness has more to do with the fact markets don’t know how and what to discount. We have never been here before and the times they are a-changin’.

The real Fed Funds rate, which is basically the fed funds minus the inflation rate, is…negative. Prior to every recession in the last 50 years, it has been positive. So, we have a long way to go. – Richard Bernstein (4 minutes in)

Since CK loved charts, we will honor her with a weekly (consistent as we can) chart series with addition of a few of our comments.

1. Crypto Crash

Rising speculative asset values that are not backed by production are inflationary on the margin as the wealth effect increases demand with no commensurate supply or production. My 19-year-old daughter brags about her friend who bought a new Tesla with his/her crypto winnings. What did he/she produce, we ask? The crypto crash and stock bear market are doing some of the Fed’s work but destroying many true believers’ savings. An example of market-based “money” destruction.

The market capitalisation of crypto has slumped to just $1.3trn, from nearly $3trn in November. On May 18th bitcoin traded at around $29,000, a mere 40% of its all-time high in November; the price of ether, another cryptocurrency, has collapsed just as spectacularly. Six months ago Coinbase, an exchange and the leading crypto-industry stock, was worth $79bn. Now it is valued at just $14bn, and the firm is “reassessing its headcount needs”. – Economist

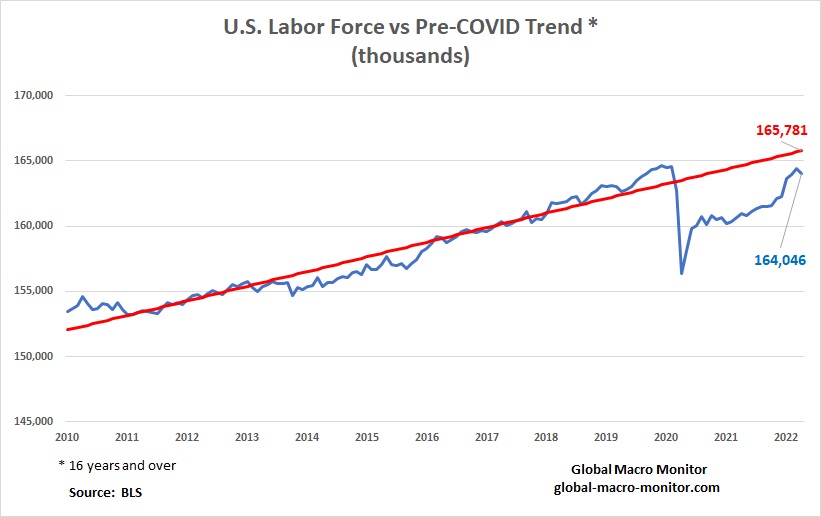

2. U.S. Labor Force Below Pre-COVID Trend

The U.S. labor force is 587K or 0.36 percent below its December 2019 peak and 1.7 million short of its pre-COVID trend. Understanding the economic impact of the post-COVID labor force dynamics cannot be inferred without digging deeper. We have done that and will post it up later this week. Stay tuned.

3. The U.S. Economy Is Almost Back To Its pre-COVID Trend

The U.S. economy is now back to only 0.80 percent below its pre-COVID trend. Compared to the labor force gap, it is not a stretch to understand what’s driving wage inflation.

4. Housing Inflation Still A Big Issue

Shelter inflation doesn’t capture the true cost of housing in the way Owners Equivalent Rent (OER) is calculated but is starting to show up in the official figures, now one of the main drivers of CPI inflation. As of today, we are still seeing panic buying and all-cash offers to win the bid for houses in NorCal. That money needs to leave the economy, and it will if the Fed backs up its tough talk. We doubt it.

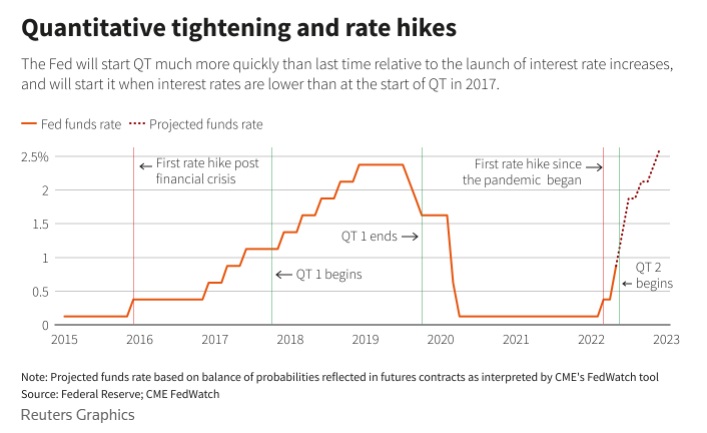

5. Quantitative Tightening Begins Next Week

If the Fed sticks with its quantitative tightening monthly caps – $30 million from June to September and $60 billion after that — we estimate $329 billion will be pulled out of the Treasury market in 2022 and a total of $972 billion through 2023. Estimating the roll-off of mortgages is more complicated and beyond our pay grade, but we can confidently say that the monthly mortgage roll-off cap will be $35 billion after September.

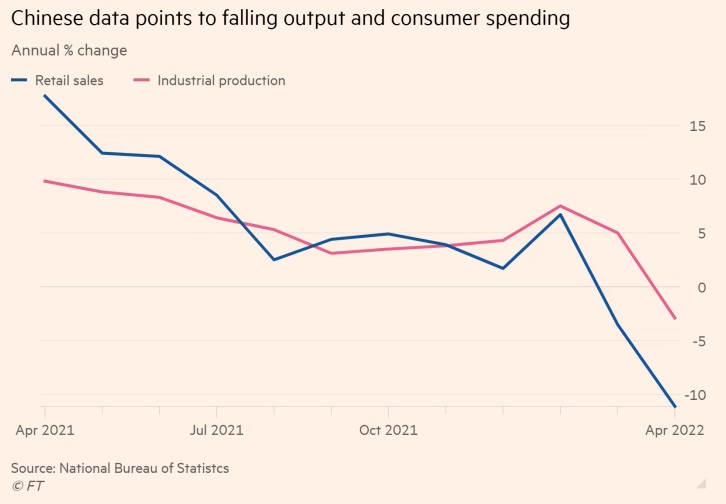

6. The China Syndrome

China is the big economy that most economists are worried about and the past week has seen new data reinforcing concerns about its prospects. Accounting for 19 per cent of the world’s total output, China is now so large that when it catches Covid the rest of the world cannot ignore its pain, especially because of its impact on global supply chains and its demand for goods and services from other countries. – FT

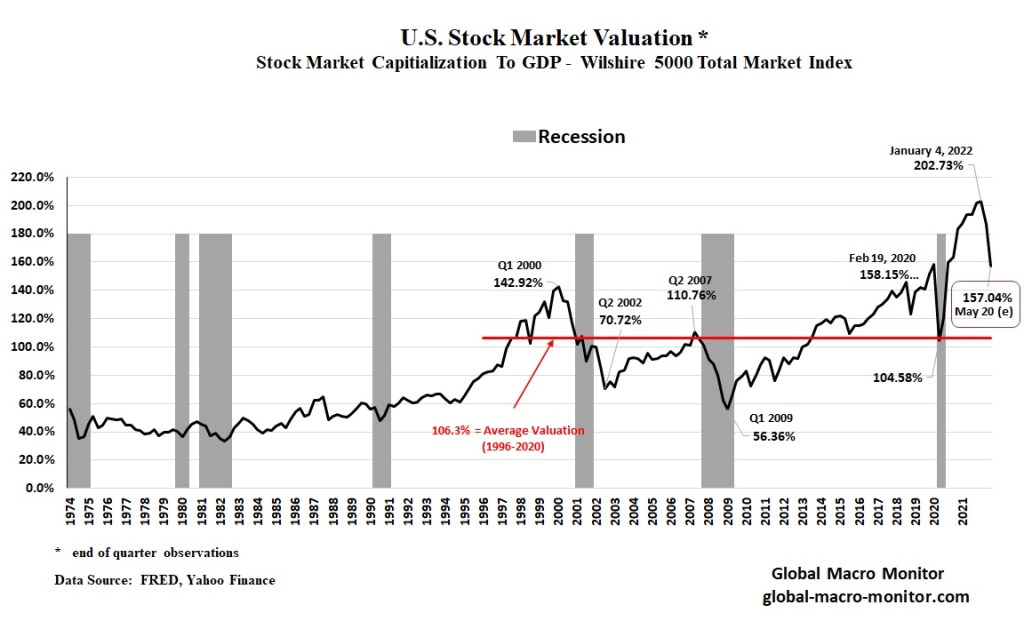

7. Stock Market Valuation: Are We There Yet?

You decide. Inflation is helping a lot.

Please comment or email if you like to see the charts as a weekly feature or if you have any suggestions to make the post better. Thank you.

Rate hikes can slow the flow of endogenous money (market and credit-based), but there is too much base money (central bank created) in the global economy. Much of the supply chain disruptions are from too much demand swamping supply capacity. We are fascinated watching the obfuscation over the cause of the inflation, much driven by politics and CYA.

Grab for the plunger and Drano. Inflation will only be tamed by draining base money through Quantitative Tightening (QT).

Getting monetary policy right is difficult, like threading a needle with boxing gloves on. Try it sometime.

But the real culprit is the demand side. It’s about oodles of money in people’s pockets being spent on everything from sports betting, to meme stocks and crypto, to new houses. I understand that getting the amount of a national bailout right ain’t easy, but I think you can argue convincingly that we overdid it.

And so, cutting to the chase, here’s Summers see going forward:

“I like to try to keep my facts relatively similar,” Summers said this week.

“There’s never been a moment when we had inflation over 4% and unemployment below 4%, when we didn’t have a recession within the next two years. Inflation is now well above 4%. Unemployment is now well below 4%, especially if you adjust for vacancies. So I think it’s pretty likely that we’re going to have a recession sometime within the next two years. I’m more confident about that than I am about what’s going to happen to interest rates. – Yahoo Finance

What a sad commentary on our society at large, which, we infer is partially the result of the messy world the younger generations have inherited from the Boomers. GMM has been writing about the Clash of Generations for years.

Generation Z may end up bringing on a “fur-baby boom” — since most of them don’t want to actually have kids! A new poll reveals seven in 10 young adults in Gen Z would rather adopt a pet than have their own children. – StudyFinds

Shelter inflation doesn’t capture the true cost of housing in t

Shelter inflation doesn’t capture the true cost of housing in t

{kind=link}