#CKStrong

America’s Federal Reserve has suffered a hair-raising loss of control. – Economist

#CKStong

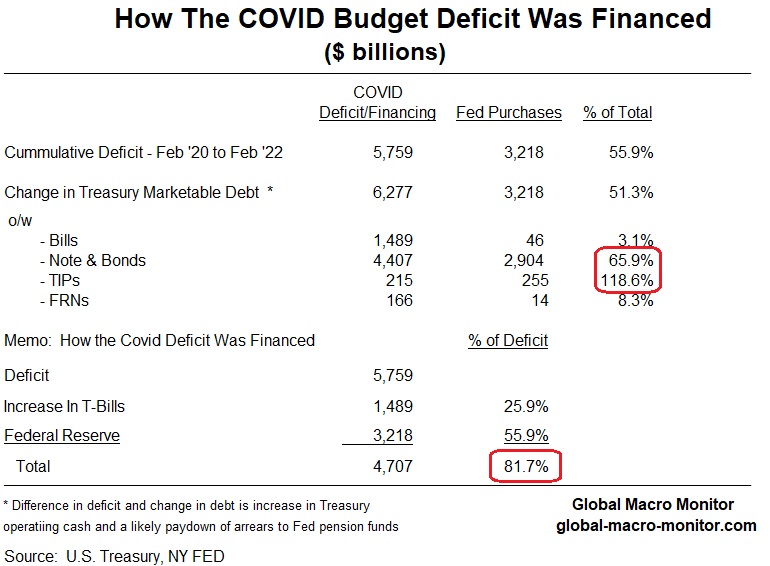

Imagining A Treasury Market Without Central Banks

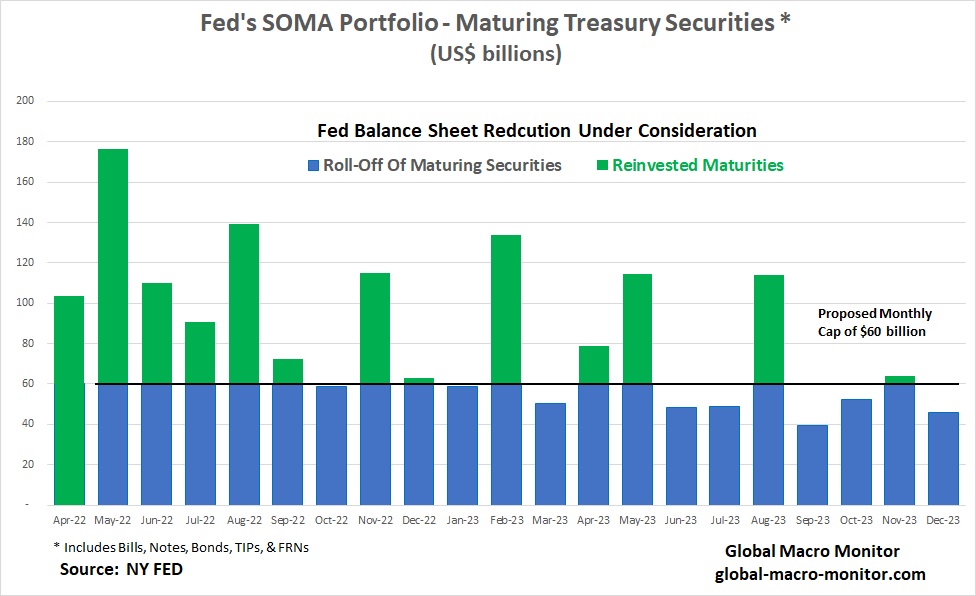

In their discussion, all [FOMC] participants agreed that elevated inflation and tight labor market conditions warranted commencement of balance sheet runoff at a coming meeting, with a faster pace of decline in securities holdings than over the 2017–19 period. – FOMC, March ’22 Minutes

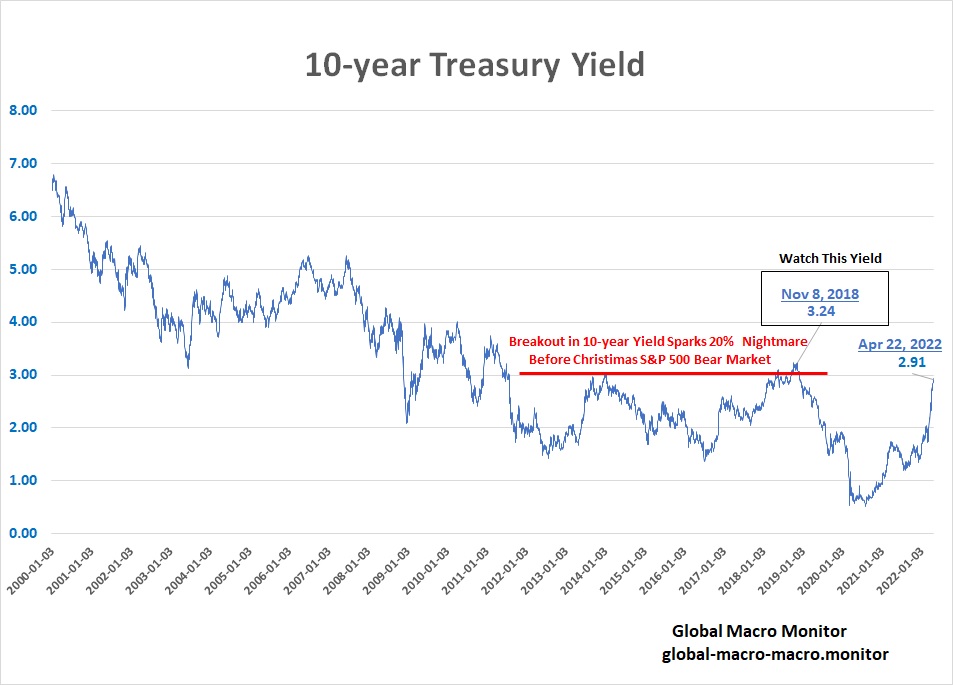

The 10-year yield is up 172 bps (144 percent) since our July 2021 post, Ignore The Bond Market Flapdoodle. Bond yields had collapsed almost 40 bps in less than a month, bringing out the “doom and gloom” crowd preaching “the bond market is signaling something bad is about to happen in the economy.” Like, inflation?

To which we countered,

Longer-term Treasury yields are so distorted by central bank buying they are now and have been for years worthless in providing any sound economic signal. – GMM, July 2021

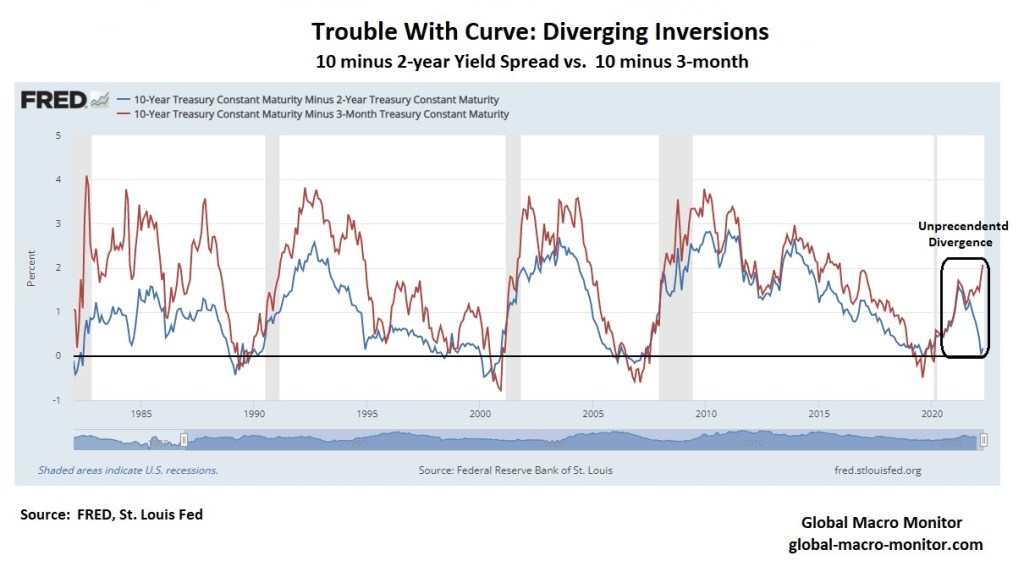

The 10-year is up 37 bps since the April 6th FOMC release of their minutes detailing a more aggressive balance sheet reduction. Before the announcement, the doom and gloomers were out with their “recession is imminent” call as the 10 minus 2-years spread inverted (went negative). Someday there will be a recession, but we doubt we will divine it from a severely distorted yield curve. Until then the bond market will be busy pricing in a new inflation and monetary regime.

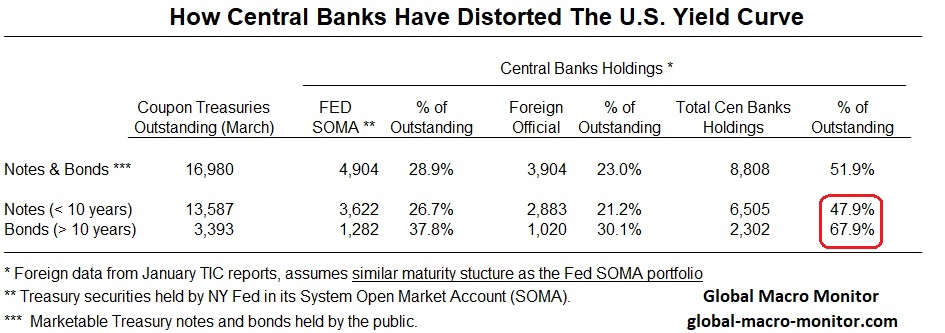

Our analysis assumes that the maturity structure of foreign central banks’ U.S. Treasury portfolios match the Fed’s – about 74 percent in securities less than ten years and 26 percent longer than ten years. It may be off slightly, but it’s the best approximation we can find.

This peculiar behavior in the yield curve leads us to believe that the the entire yield curve is about to shift much higher.

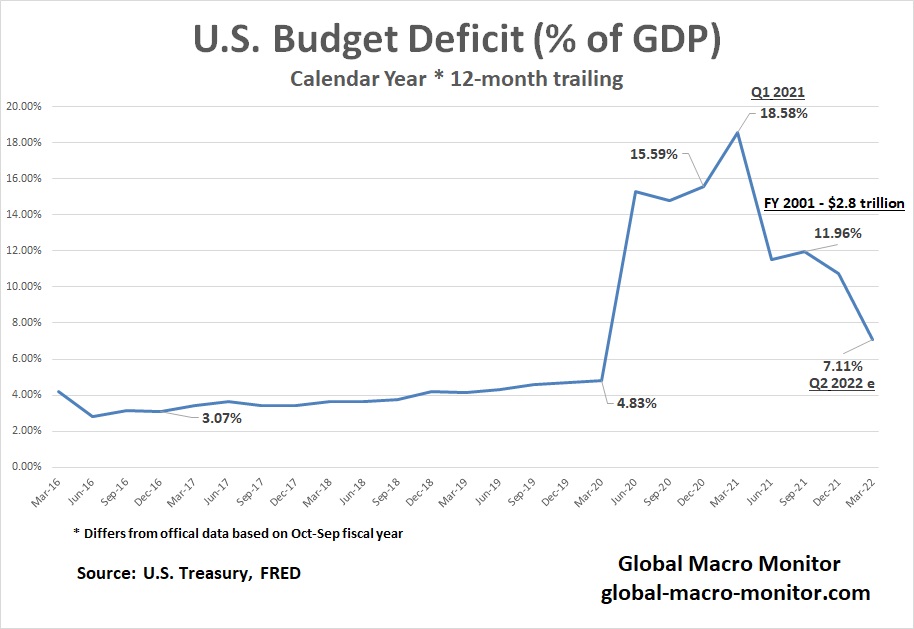

Why we are experiencing high inflation? I spent half my career asking finance ministers and central bankers, especially in high inflation emerging market countries, “What will be your budget deficit this year and how do you plan to finance it.” Large deficits financed by digital money printing without a corresponding increase in production almost always leads to inflation.

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output. – Milton Friedman

Yes, supply shocks matter but much of the supply shocks result from too much demand. Supply shocks generally result in relative price shifts and not a general rise in the price level.

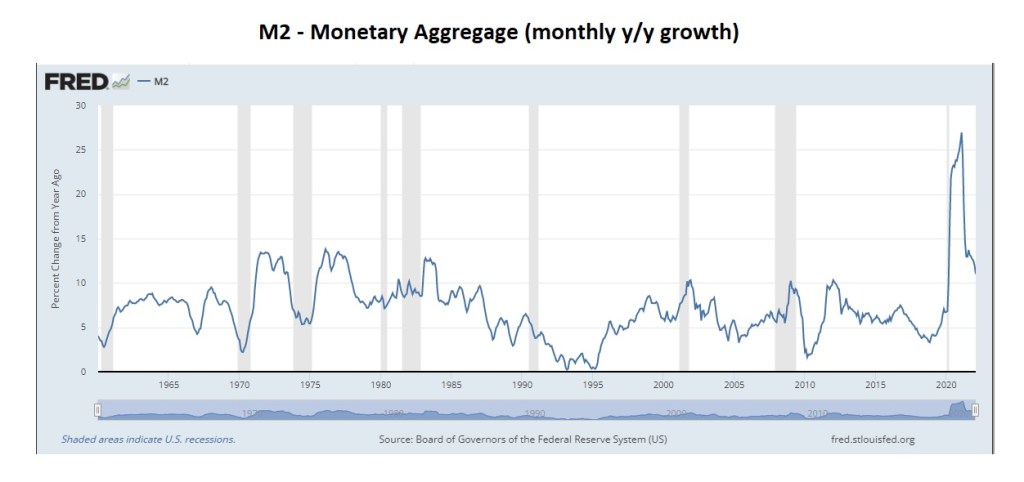

Money is an elusive concept and difficult to define, even more so as technology progresses. Still, many dismissed the link between the monetary aggregates and inflation as nominal GDP began to diverge from the official money figures in the mid-1980s.

We define money as base money, deposits, cash, credit, global wealth, crypto, and among other things, which allow economic agents to purchase goods, services, and assets. M2 — demand deposits, cash, and near money — doesn’t do service to the concept of money but is one of the best official approximations we have.

What about my securities margin account that I can write checks on?

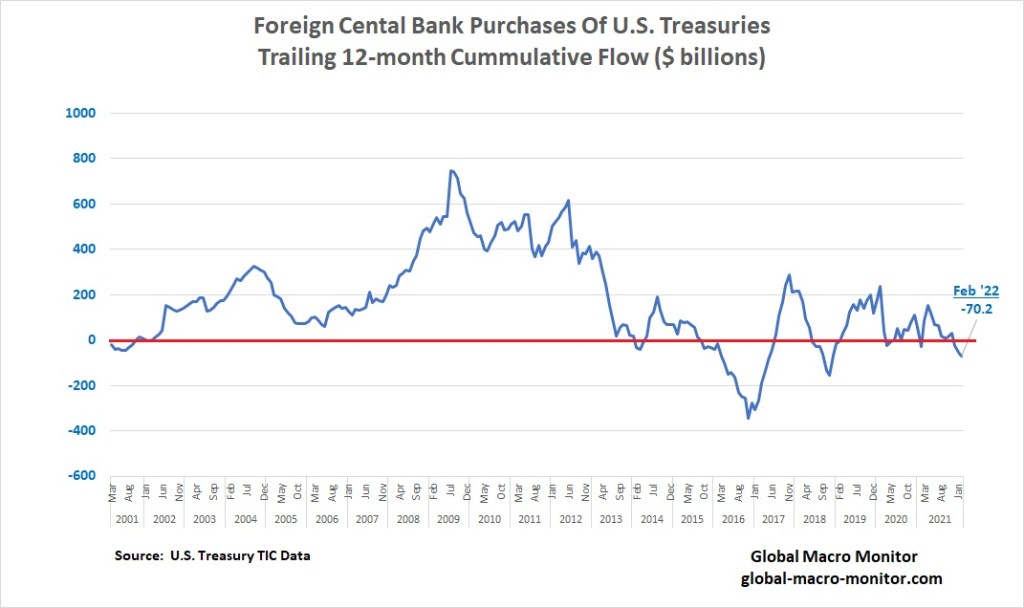

Yields are set to move higher in search of their actual market value as the nonmarket buyers have exited stage left and become net sellers.

We could be wrong if asset markets collapse (doubtful in the short-term given the vast amounts of money in the system) or another economic shock hits the global economy, bringing the duration jockeys, safe haven buyers, and hedge funds, who use the long Treasury market as a safer proxy to stock shorts, back into the Treasury market.

Beware of recency and complexity bias, folks. Globalization, which is about to accelerate and we rid ourselves of denial, and the inflationary forces are real and hazardous to the global economy and valuations. We are in a new era.

Stay tuned.

#CKStrong

Lack of spine drove inflation to nine.

#CKStrong

BFTP: Blast From The Past

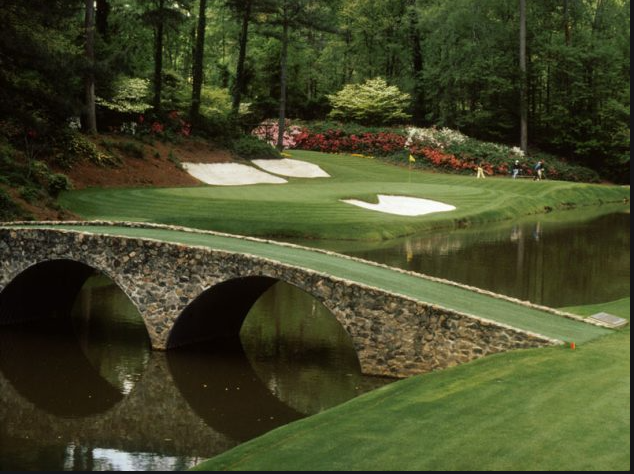

Go Tiger! What a story!

Answer to yesterday’s Masters quiz question:

Anthony Kim posted 11 birdies in the second round of the 2009 Masters.

German WWII POWs

Here’s some more 19th hole fodder to impress your buddies and something I bet you didn’t know about Augusta:

German POWs from nearby Camp Gordon built the bridge over Rae’s Creek next to the 13th tee box during WWII. They were part of Rommel’s Panzer division in North Africa responsible for building bridges to enable tanks to cross rivers.

While Augusta National is famed for its almost unnaturally beautiful flora, as it turns out some rather interesting fauna once called the course home as well: 200 heads of cattle and more than 1,400 turkeys. From 1943 until late 1944, Augusta National was closed for play and transformed into a farm of sorts to help support the war effort. Some of the turkeys were given to club members during Christmas (meat rations were in effect) while the rest were sold to local residents to help fund the club. And the cows? Well, they acted as natural lawnmowers but also inflicted quite a bit of damage to Augusta National, devouring many of the course’s famed plants and shrubs.

To help repair cattle-related damage and revive Augusta National for its reopening, 42 German prisoners of war from nearby Camp Gordon were shuttled back and forth to work on the course.

Writes John Strege in “When War Played Through: Golf During World War II:”

“The POWs had been with the engineering crew serving Rommel, the Desert Fox, in North Africa, part of the Panzer division responsible for building bridges that enabled German tanks to cross rivers. It was a useful skill for the renovation work to be done at Augusta National. The Germans were asked to erect a bridge over Rae’s Creek adjacent to the tee box at the thirteenth hole.”

The Masters resumed at Augusta National — now free of German prisoners and barnyard animals — in 1946. And interestingly enough, the Supreme Commander of the Allied Forces in Europe during World War II, Dwight D. Eisenhower, later became a member of Augusta National. Two Augusta National landmarks bearing Eisenhower’s name still stand today: the Eisenhower Tree (a loblolly pine at the 17th hole that the former president and avid golfer repeatedly struck with golf balls and requested be cut down; photo above) and the Eisenhower Cabin (built in the 1950s according to Secret Service security guidelines by the club for the former president’s visits).

#CKStrong

Money illusion is an economic theory positing that people have a tendency to view their wealth and income in nominal dollar terms, rather than in real terms. In other words, it is assumed that people do not take into account the level of inflation in an economy, wrongly believing that a dollar is worth the same as it was the prior year. – Investopedia

#CKStrong

Try discussing these ideas with someone who thinks the earth is only 6,000 years old.

Four in 10 Americans believe God created the Earth and anatomically modern humans, less than 10,000 years ago, according to a new Gallup poll.

About half of Americans believe humans evolved over millions of years, with most of those people saying that God guided the process. Religious, less educated, and older respondents were likelier to espouse a young Earth creationist view — that life was created some 6,000 to 10,000 years ago — according to the poll. – LiveScience

Whatever happened to the commandment,

Love the Lord your God with… all your all your mind

#CKStrong

Britain’s statistics office rejigged the basket of goods that make up its consumer-price index. Out go men’s suits (because of remote working), single doughnuts (people now scoff them in packs, presumably because of remote working and probably why men cannot fit into suits) and coal (no one likes it). In come sports bras (covid’s effect on fashion) and antibacterial wipes (because of sticky fingers after all those doughnuts). – Economist

#CKStrong

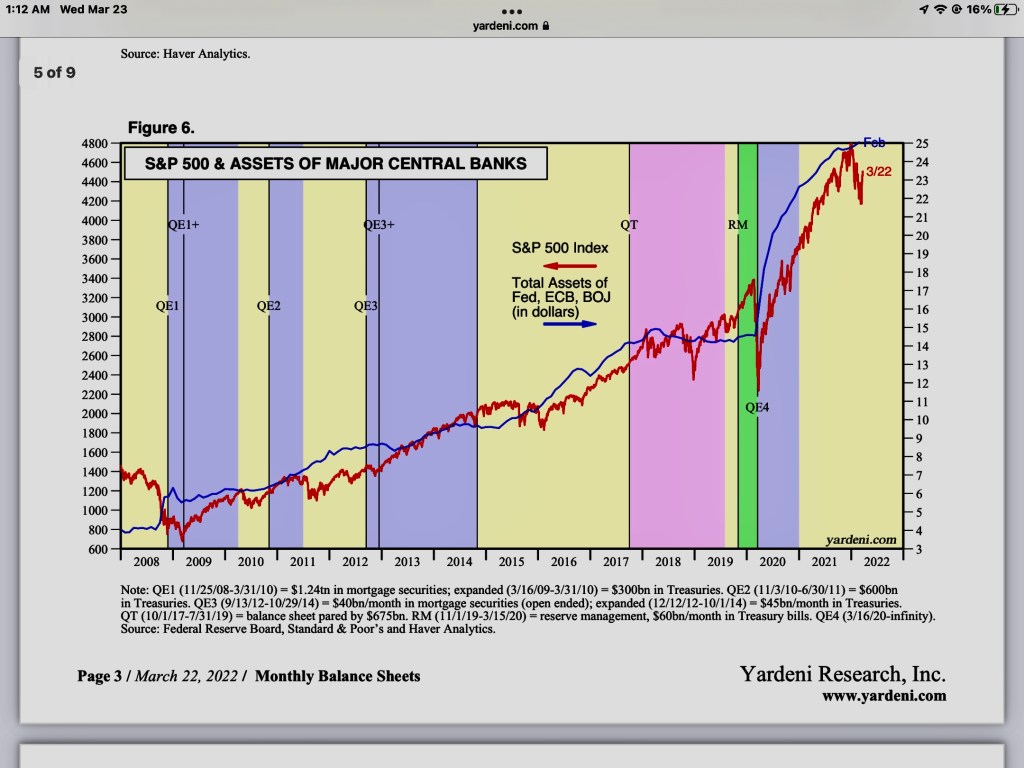

Have Central Banks Reached The Debasement Tipping Point?

It’s almost impossible to see how the central banks will climb down from the extraordinary heights they have taken their balance sheets over the past 15 years. The trillions of base money pumped into the global financial system from the central banks coupled with the money and faux wealth created by the private sector, has inflated the global money supply, wealth, liquidity, or however defined, to such extraordinary levels, and with combined with the forces of deglobalization that are fast at work will likely create a future of perpetual shortages in almost all things but fiat money.

Sorry to drive the final stake into the myth that inflation is transitory or temporary. No surprise there, however.

Seriously, folks, how Kafkaesque is it to be talking about 2.0 percent plus 10-year year yields when inflation is heading north of 10 percent on it’s way to 20 percent; or debating what the yield curve is signaling when it is has been managed by the Fed for over a decade? Strange days indeed.

What kind of Kool-Aid is everyone drinking? I want some.

The Federal Reserve has shredded it’s credibility keeping the monetary spigot turned on for too long and repressing so-called market interest rates, especially given that there was no credit crisis. My 19-year old daughter is being offered lines of credit greater than Ty Cobb’s top salary.

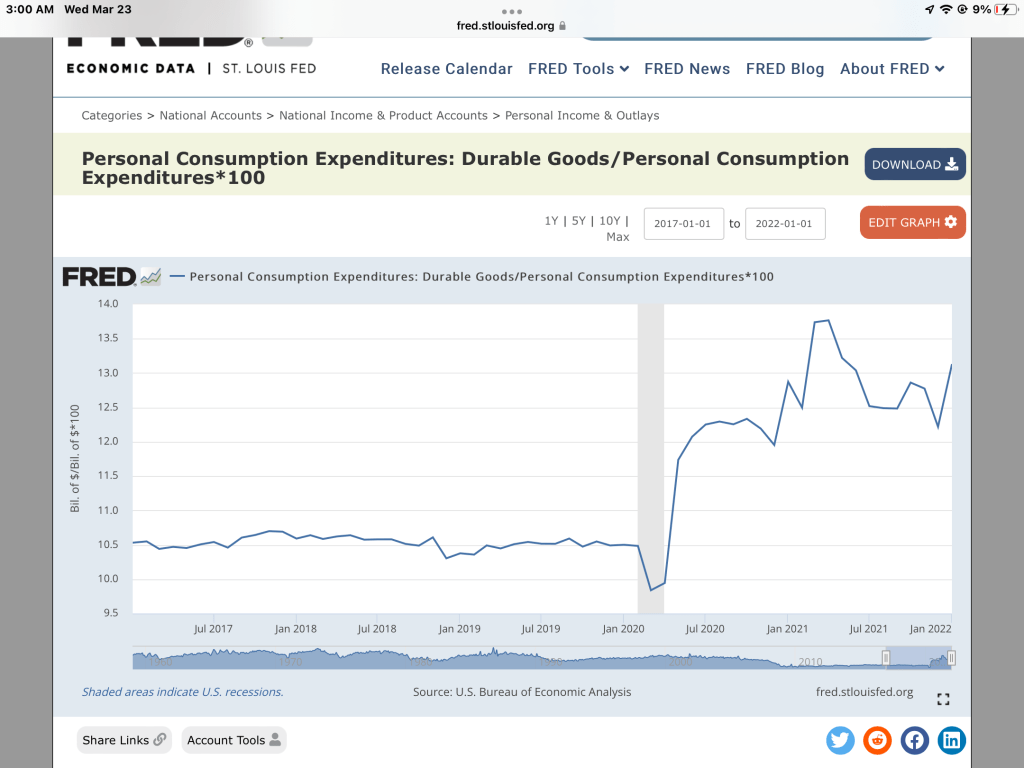

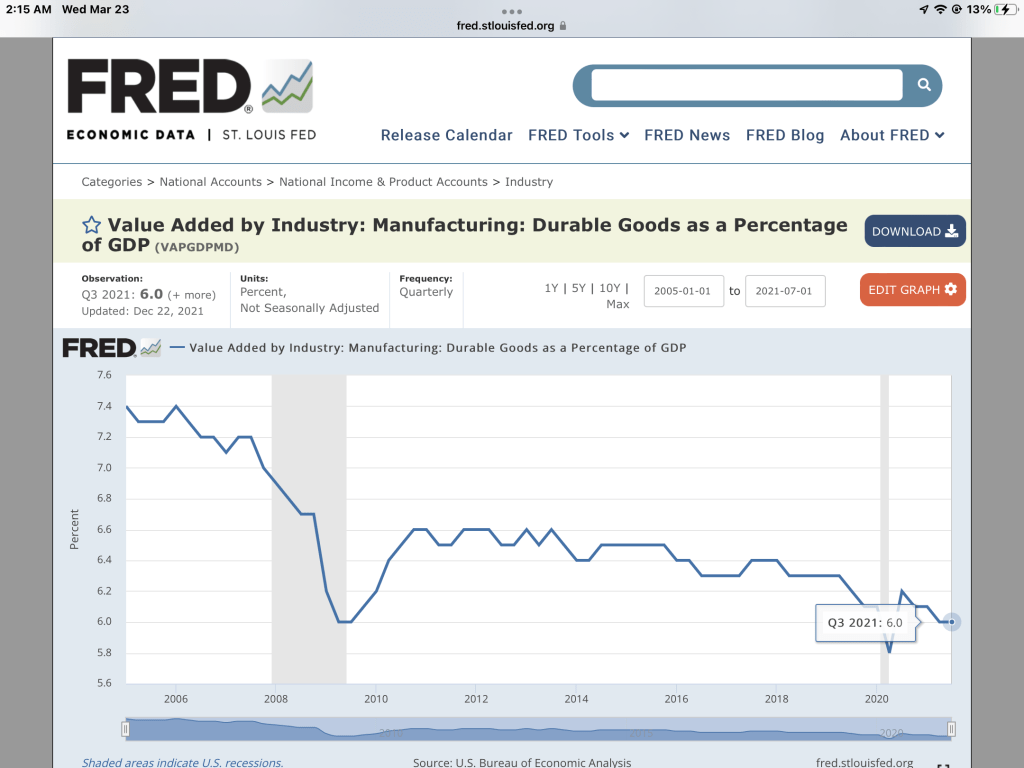

Blame It On The Supply Chain?

Nah, maybe in part, we concede, but personal consumption expenditures on durables make up only 13 percent of total personal consumption, although durable consumption skyrocketed during the pandemic, swamping supply chains. Morevever, the value-added of durable goods to U.S. GDP is only 6 percent of GDP.

Got that, folks? The U.S. only produces 6 percent of it’s GDP that hurts if you drop it on your foot. If, perhaps, you dropped a stale cupcake on your foot it may sting a bit, but it would be classified as a manufactured nondurable good, which make up about 5 percent of GDP.

Furthermore, can anyone explain the supply chain issues driving skyrocketing rents?

Too Much Money Chasing Too Few Goods

Too much money chasing too few goods…and wait for it…the velocity of money, again, however defined, will increase with inflation. And, yet, the Fed talks big but slow walks.