Global Stock Indices

Relatively quiet week in global equity markets given the FOMC’s historic decision to start reducing the Federal Reserve balance sheet, to which we called the market action a big double cheese non-burger.

Argentina continues rockin’ the free world, up almost over 5 percent this week and closing in on the 50 percent mark for the year. Argentina’s competitiveness is getting a double boost with a weaker currency, down 9 percent against the dollar this year and the dollar index is down 10 percent. That’s about 20-25 percent boost in euro terms.

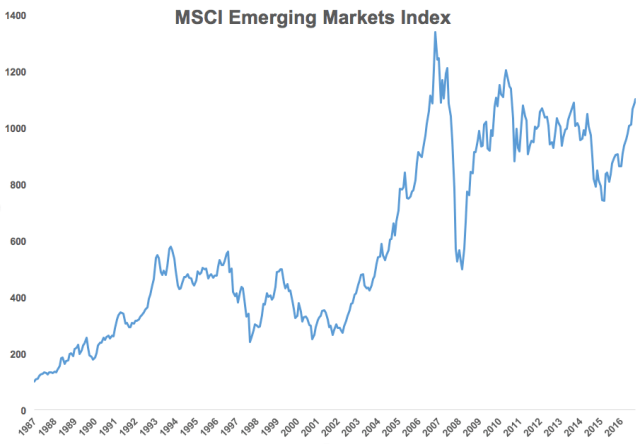

Emerging market equities have been stellar this year.

“After lagging for many years, there has been a significant breakout to two-year highs in the MSCI Emerging Markets Index relative to the S&P 500,” he wrote in a note, calling this “another indicator that the EM strength could be legitimate and should continue to be a place to find potential alpha in well-diversified portfolios.” – Ryan Detrick via MarketWatch

Turkey down on “dodgy” politics and as global markets begin to fret over carry trade countries with high-interest rates to attract hot money capital flows to cover current account deficits. Turkish 10-year yield up 27 bps on the week.

Global 10-year Bond Yields

Big move down in Portugal 10-year yields as the sovereign recaptured its investment grade rating from S&P. Brazil continues to come in as markets are true believers in potential economic reforms of a government under political fire. Brazil and Indonesia bonds rates are honey to yield seeking capital in a NIRP and ZIRP world.

Turkey hit with what was noted in stock section above.

The UK and China sovereign ratings were downgraded this week. Ratings agencies always the last to turn out the lights and markets are way ahead of the them.

The “head for spread” continues. Junk in 12 bps.

Global Currencies

Dollar relatively stable and strong against EM. The Dixie holding above the 91-92 level on the FOMC action. Euro/$ having a tough time cracking and holding the 1.20 level. Shorts may get nervous.

Select Commodities

Nothing big except iron ore continues to flop. Not that bad of a week for the complex given the Fed action.

Other Risk Indicators

Energy stocks, this year’s big laggard, bought up as expectation crude in a new higher range of $50-55. Euro banks up on stronger PMIs throughout Europe. Russell looks like it is ready to take out new high. Stress index and VIX lower. Markets believe all is well.

On Our Radar Next Week

- We are watching North Korea as tensions ratchet up. The debacle now has morphed into what looks like a cage fight between “Twitter Man” vs. “Rocket Man”. Markets are not going to like this.

- Fallout of Saturday’s New Zealand election, which returned a hung parliament. Not expecting much impact.

- The results of Germany’s election will be more interesting

- Watching Spain for potential instability leading up to Catalonia’s independence vote on October 1.

- Watching fallout from Kurdish independennce vote from Iraq set for Monday. Turkey not happy.

- Will Aaron Rodgers, QB of the Green Bay Packers, take a knee in today’s game? President Trump’s tirade against the NFL in his speech in Alabama on Friday night is blowing up in his face and has transformed a racial issue into an assault on the First Amendment. Caesar should not pick on the circuses and the gladiators. Always a losing proposition to awaken the masses.

- Lots of Fed doves speak next week. Janet Yellen at 11:50 eastern on Tuesday.

- Economic data: Wednesday – Durable goods; Thursday – GDP, and Friday – Personal Income.

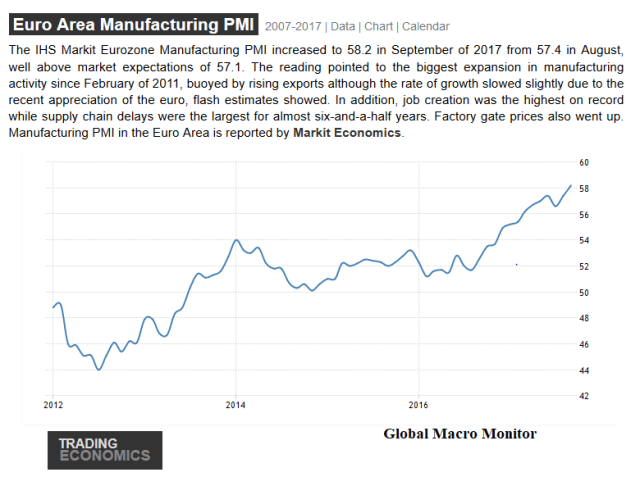

- Most important, European bond markets as ECB is way behind the curve, especially given last week’s strong PMIs (see the chart below)

Notice a prevailing narrative from the above?

The whole world, even now the west, is slouching toward tribalism.

Most important, we are preparing for the coming October correction we have been looking for.

Stay thirsty, my friends.

Key Charts

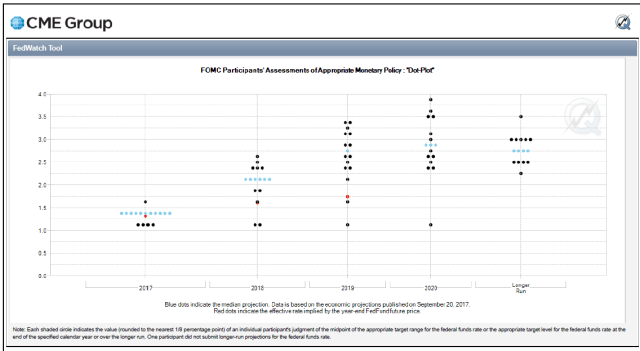

The red dot represents the markets’ expectation versus FOMC dots. Market expecting much lower policy rates than Fed officials. See here.