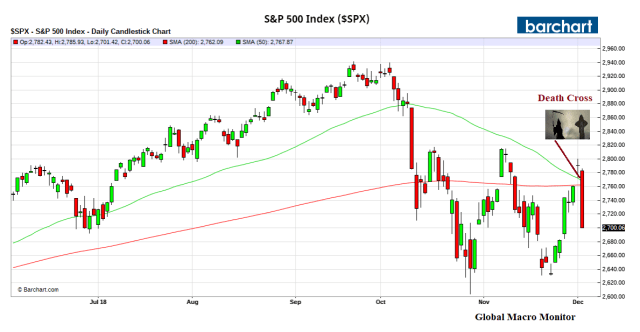

Fugly day in the stock market.

We had to post a response to the market punditry rationalization on why stocks accelerated downward today:

“the S&P500 broke its 200-day moving average.“

Are you fricking kidding me?

The S&P500 has been under its 200-day 87 percent of the past 30 trading days and 14 straight days prior to yesterday’s ramp.

Why then would a break of the 200-day moving average tank stocks?

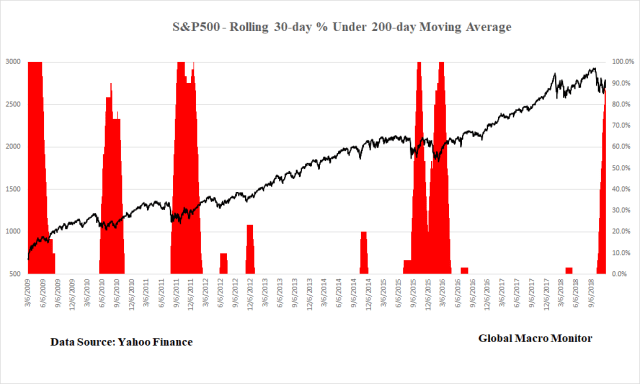

Nice Chart

See the second chart below which illustrates the percentage of days over a 30-day rolling period the cash S&P500 has been below its 200-day moving average.

It is interesting that from March 16, 2016, to March 29, 2018, the S&P500 closed under its 200-day only once. That is 1 out of 514 trading days. Moreover, from June 28, 2016, to March 29, 2018, the S&P500 closed above its 200-day 442 consecutive days.

Didn’t Minsky say, something to the effect, the lack of volatility, leads to complacency, which sows the seeds of higher volatility?

Stop Losses?

We’ll concede it is possible that many, including the trading ‘bots, who got long yesterday’s ramp expecting a Christmas rally may have used the 200-day as their stop-loss. The pundits should have qualified their explanations instead of hanging it out there that today’s break of the 200-day was somehow unique. Come on, man!

Perverted Yield Curve And Self-Fulfilling Recessions

The noise around the “perverted” yield curve is also absurd, at least to us, and a bit dangerous as it could actually be self-fulfilling and cause the recession it is supposedly predicting. The policymakers, who have manipulated the markets for the past decade, just might be seeing the chickens finally coming home to roost.

Nevertheless, as we have said many times, the only way bond yields move lower is due to haven flows. That is other markets need to sell-off bigly.

We are working on a piece, crunching the numbers, on the yield curve. It should be posted in the next few days.

Stay tuned.