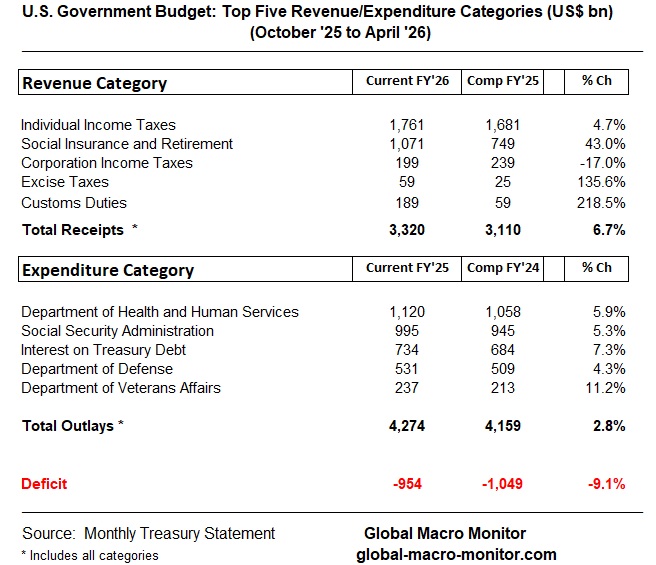

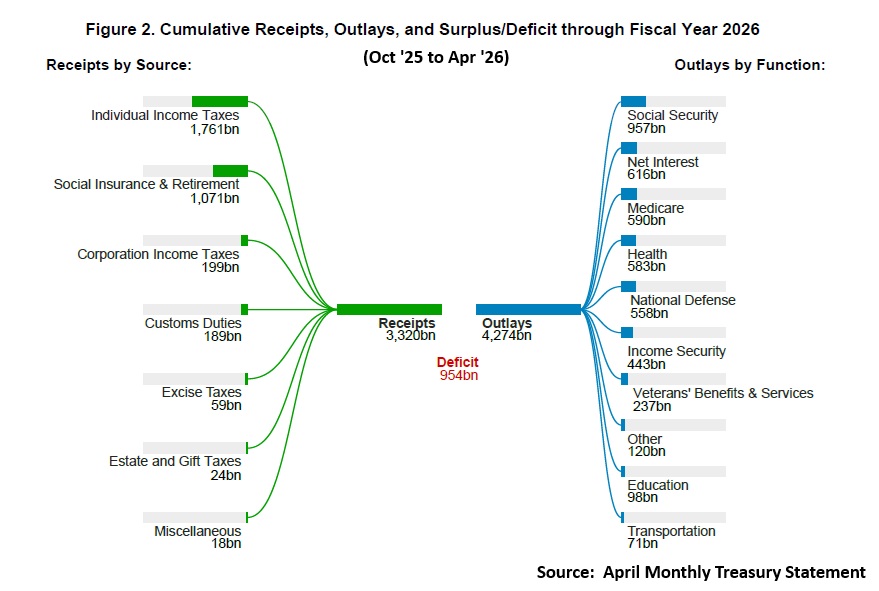

The headlines look almost encouraging. The U.S. federal deficit for the first seven months of fiscal year 2026 came in at $955 billion — $94 billion better than the same period a year earlier. Revenues rose 7%, outlays only 3%. So is Washington finally getting its fiscal house in order?

Not quite. Dig one layer deeper and the picture is less a turnaround than a temporary optical illusion.

The Tariff Mirage

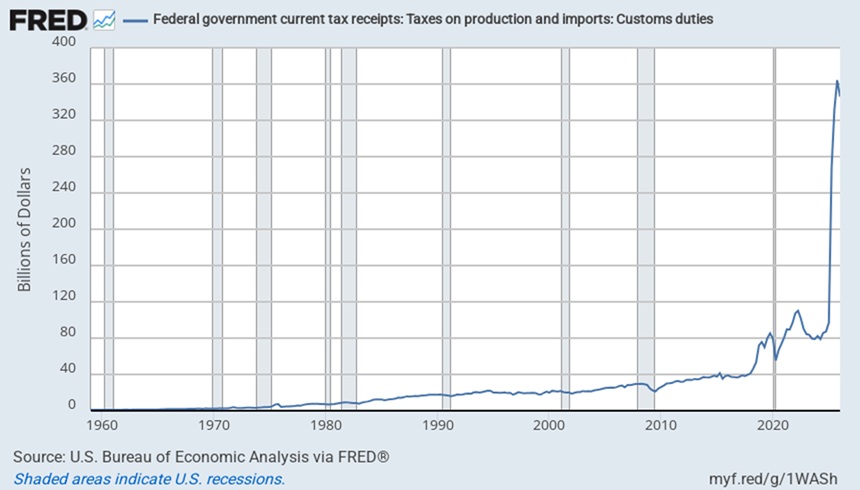

Nearly all of the year-to-date improvement traces back to a single source: customs duties. Tariff revenues surged by $130 billion over the period — roughly three-fifths of total revenue gains, and larger than the entire $94 billion deficit improvement. Strip out tariffs, and the budget actually deteriorated. Corporate tax receipts fell $58 billion, and non-tariff revenue growth of $79 billion was simply no match for $116 billion in new outlays.

This is fiscal improvement by executive fiat, not structural reform. And it’s already fraying. A February 2026 Supreme Court ruling struck down IEEPA-authority tariffs — the source of roughly half of all customs duties collected since January 2025. CBO estimates that ruling alone will add $2 trillion to projected deficits over the next decade compared to the February baseline. Penn Wharton pegs the average effective tariff rate at just 7.1% after the court-ordered regime change. The windfall is leaking.

The Structural Problem Hasn’t Moved

Beneath the tariff noise, the fiscal math remains deeply uncomfortable. CBO’s full-year deficit projection sits at $1.9 trillion, or 5.8% of GDP — well above the 50-year average of 3.8%. Federal debt held by the public hits 101% of GDP this year, reaching 120% by 2036, and a staggering 175% by mid-century.

The composition is the real story. Mandatory spending — Social Security, Medicare, Medicaid — now runs at 14.2% of GDP and is essentially on autopilot. Social Security and Medicare alone will account for 81% of mandatory spending growth through 2036. Discretionary spending, meanwhile, is at its lowest share of GDP since 1962. There is no fat left to cut there. And then there’s interest: net interest costs of $1 trillion this year (3.3% of GDP) will nearly equal all discretionary spending by 2036. The fiscal problem is increasingly an interest-burden loop on top of pre-existing primary deficits, not a conventional spending blowout.

G7 in Context: America Is Not Alone, But It Is Unique

Japan retains the dubious crown of most-indebted G7 sovereign, with gross debt at 204% of GDP against a 2% deficit. The BOJ’s yield curve control legacy has provided remarkable insulation — effective interest costs still run below nominal GDP growth — but IMF projections suggest interest payments could double between 2025 and 2031 as JGBs roll into higher yields. A shrinking BOJ balance sheet and rising foreign investor participation will make that market progressively more sensitive to fiscal news and global risk-off episodes.

Elsewhere in the G7: France runs a 4.9% deficit with debt at 118% of GDP; Italy posts 138% debt; the UK sits at 104%. All three face credibility and repricing risk if growth disappoints. Germany, the outlier, carries just 64.6% debt — but is now choosing to use that fiscal space, with defense and investment commitments pushing debt toward 74% by 2031.

The U.S. sits in a category of its own: very large deficits combined with ownership of the world’s benchmark reserve asset. That combination preserves market access but also means fiscal slippage transmits through term premia, Treasury auction absorption, and global duration markets — not just domestic credit spreads.

What This Means for Portfolios

The risk here isn’t imminent sovereign default — it never was. It’s subtler and more tradeable: rising term premia on long-duration Treasuries, rollover sensitivity ($9.7 trillion in Treasury debt matures in FY2026 alone), and the increasing linkage between sovereign funding markets and leveraged nonbank intermediaries. IMF and GAO both flag that fiscal stress is more likely to surface through auction tails, repo strains, or basis-trade deleveraging than through macro data or ratings actions.

Moody’s and Fitch have both flagged the trend. The message is consistent: U.S. fiscal exceptionalism is eroding faster than Aaa-peer norms. That’s not a crisis call — it’s a duration and liquidity-risk repricing call.

Though it is not easy deconstruct with certainty the reasons for 60 bps pop in 10-year Treasury yields since the end of February, there is no doubt much of the above is playing a role along with the increase in expected inflation.

Position accordingly and stay frosty folks.

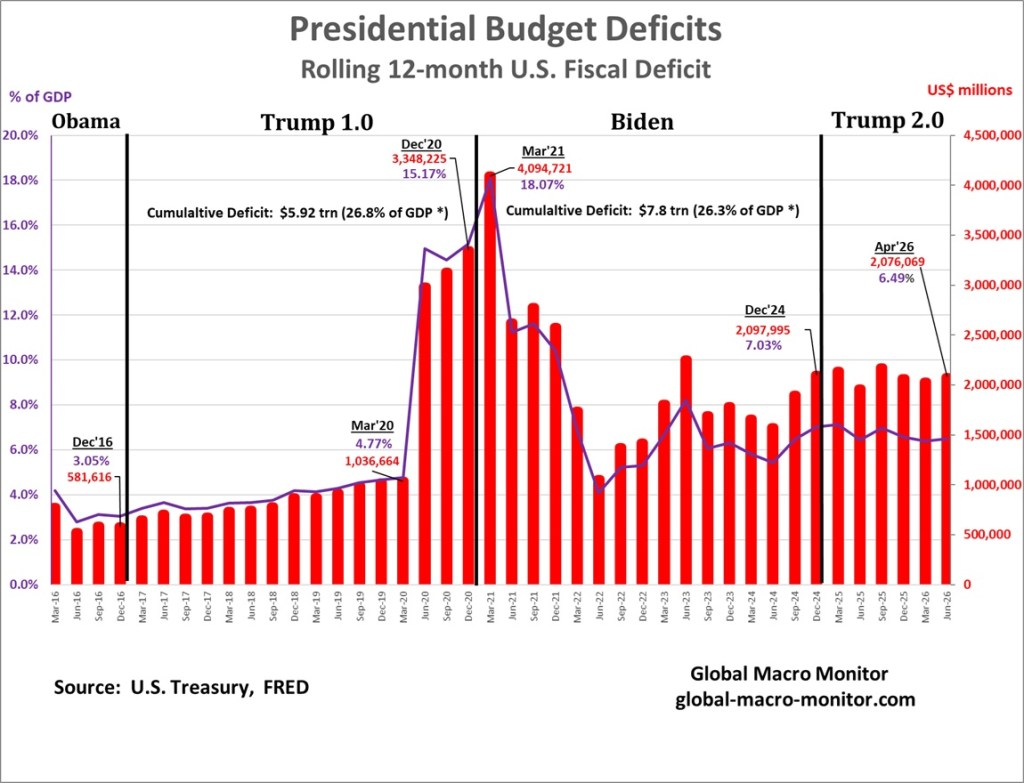

Appendix: Presidential Budget Deficits

The conventional political narrative holds that Biden blew up the federal deficit. The data tell a more complicated story, and one that will surprise many.

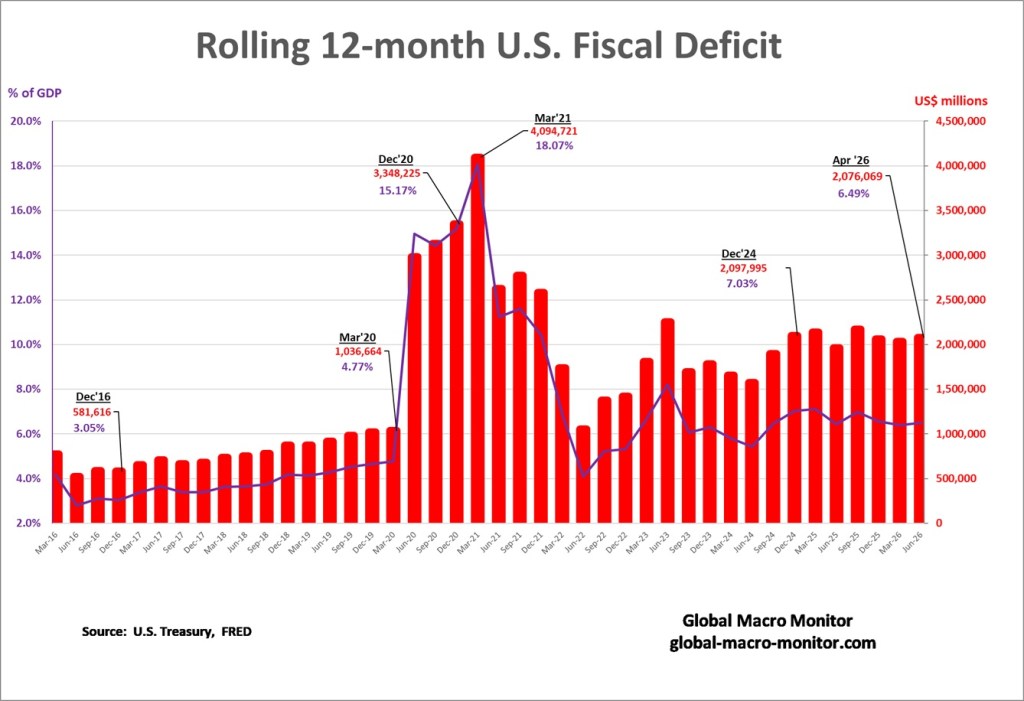

Presdient Obama left office with the rolling 12-month deficit at a relatively disciplined 3% of GDP. Trump 1.0 then widened the structural deficit to nearly 5% of GDP by March 2020, before the COVID pandemic began to spread in the United States. The pandemic did the rest: emergency spending exploded the deficit to 15.2% of GDP by December 2020. What is rarely acknowledged is that Trump handed Biden a deficit already running at 15% of GDP — among the largest in U.S. peacetime history. Biden’s early months pushed it marginally higher to a peak of 18.1% by March 2021, but the trajectory was largely baked in before the inauguration.

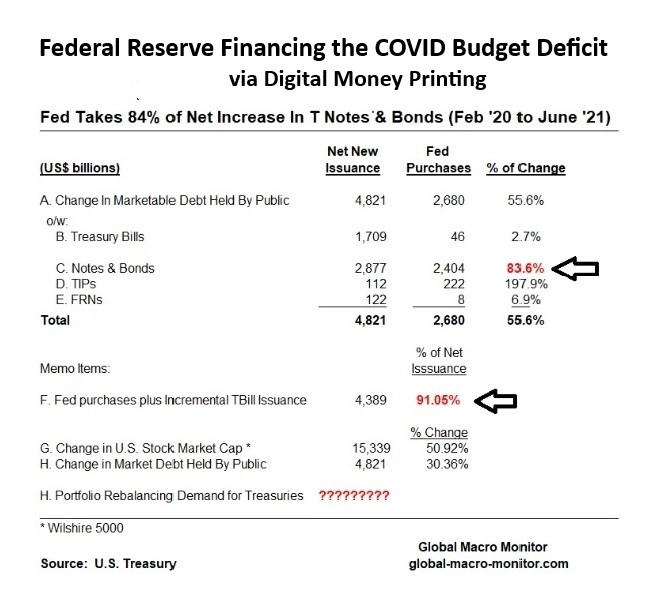

The fiscal shock was too large for private bond markets to absorb. The Fed stepped in as the bond and U.S. Treasury debt buyer of last resort, purchasing 83.6% of all net new Treasury notes and bonds issued between February 2020 and June 2021 — funding 91% of net issuance when incremental T-bills are included. That is digital money-printing at scale, and it is the true origin story of post-COVID inflation in both financial assets and goods and services.

Pingback: Presidential Budget Deficits | Global Macro Monitor

Pingback: Presidential Budget Deficits | Global Macro Monitor

Pingback: The Medicaid Surge: Economic Drivers, the Unwinding, and the OBBBA Retrenchment | Global Macro Monitor