Stocks were hit with a double punch with the Apple warning and this morning’s weak ISM data (see table). The S&P took out all its hard work since the Christmas Eve tank to close at its post-Christmas low.

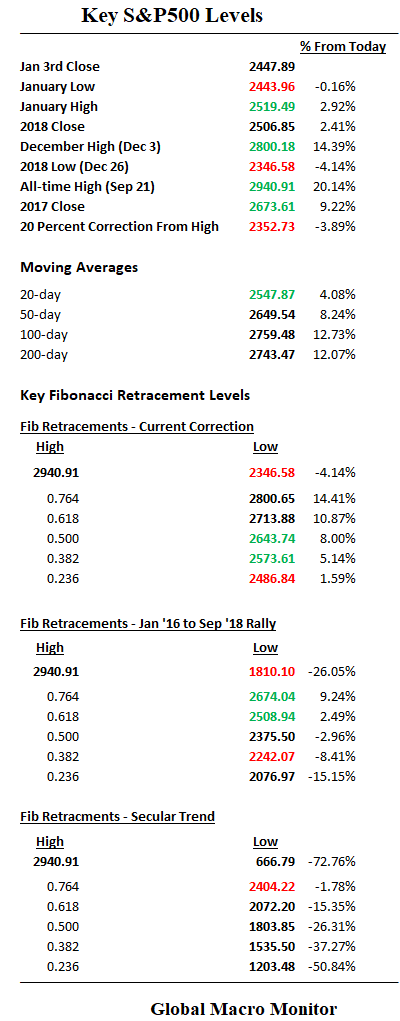

We’re not going to bore you with the key levels as they are evident in the table.

The logical short-term trade here is to bet on a test of the recent low at 2346.58, 4 percent down from today’s close. But as we quoted Stan Druckenmiller in our recent post,

“Logical doesn’t mean profitable.”

Eventually, and relatively soon, we think the test is a no-brainer, however, tomorrow’s employment data and Jerome Powell speech are events that could generate a bounce.

If the employment data comes in soft but not too soft, coupled with today’s weak ISM gives the Fed Chair the cover to strike an exceedingly dovish tone in his speech tomorrow. Ergo rally time and the shorts get their Friday facial and should further boost our gold trade.

Moreover, it’s now or never for a bounce. The chart below shows how rare it is that the S&P500 has closed this far below its 200-day moving average. In fact, only three times since August 2011.

If there is no or just a feeble bounce tomorrow, we get shorty the e-minis for the test of the recent low.

Brazil Equity Trade

How ’bout that Brazil trade, (EWZ), we identified on January 1st? It was up almost one percent in today’s extremely weak tape and now up almost 5 percent from our $39.00 entry point. We are moving the trailing stop up to $38.77. We like the country ETF as it also captures the currency move.

Druckenmiller On Bonds

If you listened to the Druckenmiller interview we posted on New Year’s Day, he thrives in bear markets, not by shorting stocks but being long bonds. Shorting stocks in a bear market, though more profitable, he has learned is riskier due to the higher propensity for nutcracking short squeezes. Druck also worries about the level he is buying at.

Nevertheless, this confirms our suspicion the bond market has been hijacked by stock bears and short sellers. How far they push down yields is anyone’s guess. We just wonder who they are going to sell to when its time to get out. They couldn’t be betting on a central bank takeout in a new round of QE?

Unexpected bond market volatility could be the Black Swan of 2019. We will flesh out our thoughts in a later post.

Source: Institute for Supply Management