Summary

- Bond yields mostly lower on the week as global growth expectations ratchet downward and yield chasing back in vogue, led by Brazil

- Credit spreads tighter led by lower-tier credits

- Major Latin FX rebounds after a few weeks of weakness

- Dixie rejected right at 97.70 resistance. Chart traders and/or ‘bot in total control. We was [sic] wrong but believe dollar moves higher into year-end

- Pound continues to price soft Brexit or new Refie

- Smart week for global equities

- Brazil equities bounce big after their bout of weakness

- S&P closes at its highest level since the bear market began in late September

- VIX at the lowest level since October

- Wheat and corn bounce on short covering due to….of course, what else, trade rumors. The American farmer has been butchered by the trade wars

Commentary: The S&P500 finally managed to crack and close above the great big beautiful wall at 2816, its highest close since last October. The Power of Zero is now driving the risk markets — that is fears that global interest rates are going to zero, some of which are already negative with a line of moving vans backed up ready to move into the less than zero neighborhood.

Oy vey! Equity markets can’t rise with stronger growth because of too much public debt in the world and it’s sensitivity to higher interest rates. Markets are now driven by FOMO and yield panic.

Nevetherless, we don’t know where the market is going tomorrow as it is pretty close to a random 50/50 bet (53/47, in fact, similar to the House odds at the roulette wheel) but as we have stated earlier, history suggests the S&P500 will end March at or around 2850. Important the S&P stays above 2820. Our instincts tell us some profit taking coming early in the week but our instincts are biased by human genes, which have evolved over the past 200,000 years of human existence, of which 95 percent of that time was spent running from wild beasts on the savannah.

Underestimate the Power of Zero, which has firmly taken hold of the markets, at your own peril, at least, until we can see the white of the eyes of a global recession. The market is now pricing a 10 percent chance of a Fed rate cut by June and an almost 30 percent probability by December. Nuttin’ else seems to matter, honey!

We are we looking at this week? Glad you asked:

- Potentially, another Brexit vote in Parliament. The PM may or may not table it depending on if she thinks it can pass. Rumors are that Tory Brexiteers have told her they will vote yes if she stands down as Prime Minister.

- The Fed meets and may lay out their exit plans from their balance sheet reduction.

- Bank of England meeting.

- President Xi’s visit to Italy.

- Brazil’s Bolsonero visit to the White House.

- The election in Thailand. Back to democracy?

- FedEx earnings

- U.S. factory orders and existing home sales

- Japan CPI

- Eurozone PMI

- Argentina Q4 GDP

- Other

- P.S. More “trade deal” tweets

Happy hunting out there this week, folks.

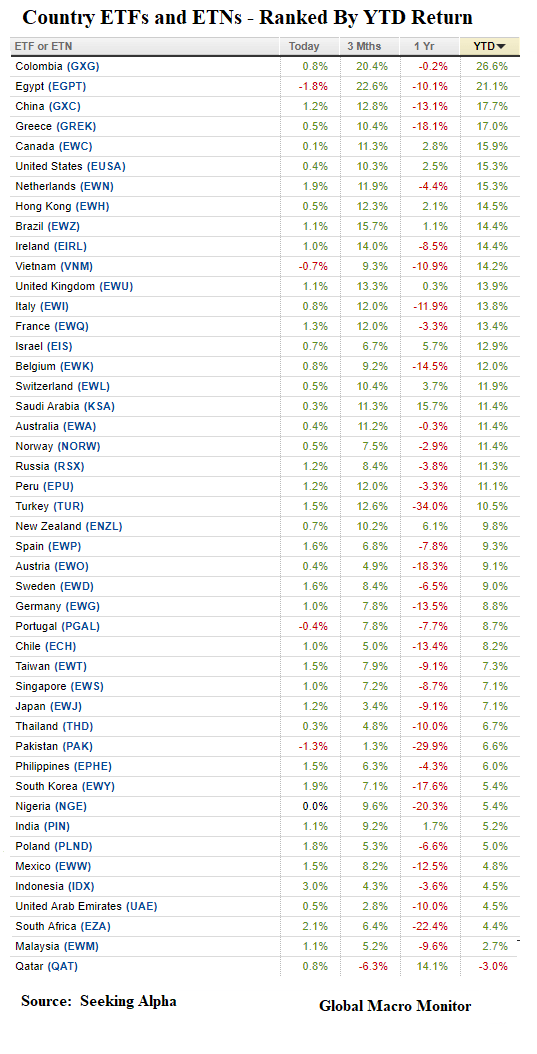

S&P Breaking Out?

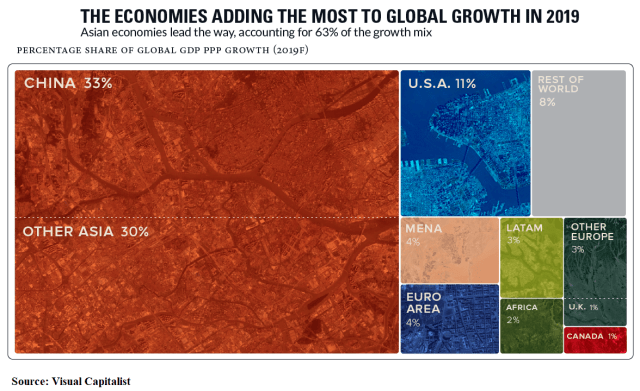

All Asia Global Economy

Hat Tip: @Carol_Kohlberg

Pingback: FOMC: Bid Adieu to QT | Global Macro Monitor

Pingback: Newton’s Q1 Law Of Motion For The S&P500 | Global Macro Monitor