Just our quick take on today’s Fed.

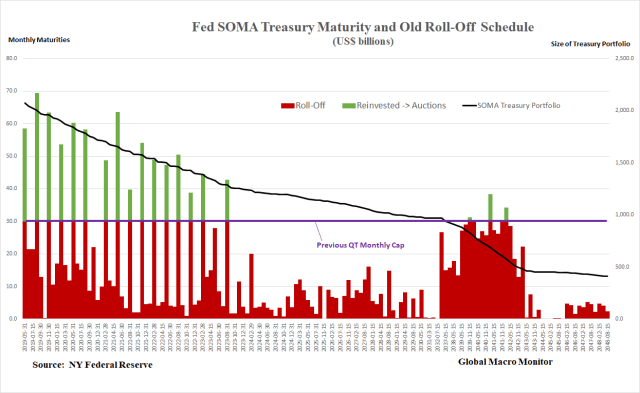

The major takeaway from today’s FOMC announcement is the end of QT in September with the cap moving down to $15 billion in the SOMA Treasury portfolio in May.

- The Committee intends to slow the reduction of its holdings of Treasury securities by reducing the cap on monthly redemptions from the current level of $30 billion to $15 billion beginning in May 2019.

- The Committee intends to conclude the reduction of its aggregate securities holdings in the System Open Market Account (SOMA) at the end of September 2019. – FOMC, March 20th

The end of QT will have little impact on liquidity in a monetary sense — that is credit creation — in our opinion but will reduce significantly the “crowding out” effect as the Treasury will have to issue a substantially lower amount of new securities at the monthly auctions to maintain its balances at the Fed.

It is also quite possible the Fed was also worried about complicating the coming battle over raising the debt ceiling as the Treasury usually runs down its Fed account to fund itself when restricted from issuing new debt. QT would have made funding the U.S. government exponentially more treacherous during a debt ceiling battle.

Our quick analysis:

Reduction in Treasury New Issuance After Today’s FOMC announcement

$137 billion – 2019

$352 billion – 2019-20

We believe the Fed, Treasury officials, and some market participants understood the changing structural dynamics and pressure that QT was putting on the Treasury market, which we pointed out last September, and acted accordingly to circumvent a potential crisis.

The stated reason given for ending its balance sheet reduction is that banks now demand more reserves, which makes no sense to us. Certainly banks demand for cautionary reserves is higher post the financial crisis given their near death experience, but they now are paid 2 plus interest on those reserves, which, we think/but not sure, have no capital requirements. Why wouldn’t they desire a higher level of reserves if they are now being paid 2 percent risk-free to lock them up at the Fed? Free money is always good, no? Also note the excess reserves are most likely highly concentrated in a few large banks.

We think the Fed has got a tiger by its tail and has no idea how to effectively extract itself from QE, and the market has trouble understanding the dynamics of QE/QT, which, in our view, is just fiscal policy on steroids.

Today’s announcement of the end of QT is probably also a major factor (lower expected supply) why the 10-year yield broke to a 2019 low at 2.52 percent, which will further panic yield chasers and add fuel to the Power of Zero, which is now driving the risk markets. Reducing the potential supply of more than $350 billion of new Treasury issuance through 2020 is not small change, folks.

Absurd? Yes, the Market Socialists once again have beat the Fed into submission but that is the reality we all are dealt, so let’s go out and make some money. Emerging markets are the place to be and probably another 10 percent in the S&P500 coming during the rest of the year.

The piper will have to wait for payment until a later date.

Back to you when we have more time to think and do further analysis.

Help keep the lights on at the Global Macro Monitor. Donate by clicking widget on the right side of our website.

You have it! Why would banks want more reserves? Because the Fed is paying them. Back of envelope calculation suggests that 25% of JPM’s profit in 4Q18 cam from Fed

Pingback: Quarter In Review – March 28 | Global Macro Monitor

Pingback: Beware Of Retrofitting Fundamentals To Price Action | Global Macro Monitor