Summary

- Big bounce in all assets after the Q4/December downdraft

- Global bond yields way down on global deflation panic as $11 trillion in global bonds now have negative yields

- The Power of Zero (yields) has driven stocks up with China leading the way

- Dollar stronger, closing quarter close to the top of its recent range

- Argentina peso hammered in Q1

- Cable stronger in spite of Brexit chaos

- China and Russian currencies stronger

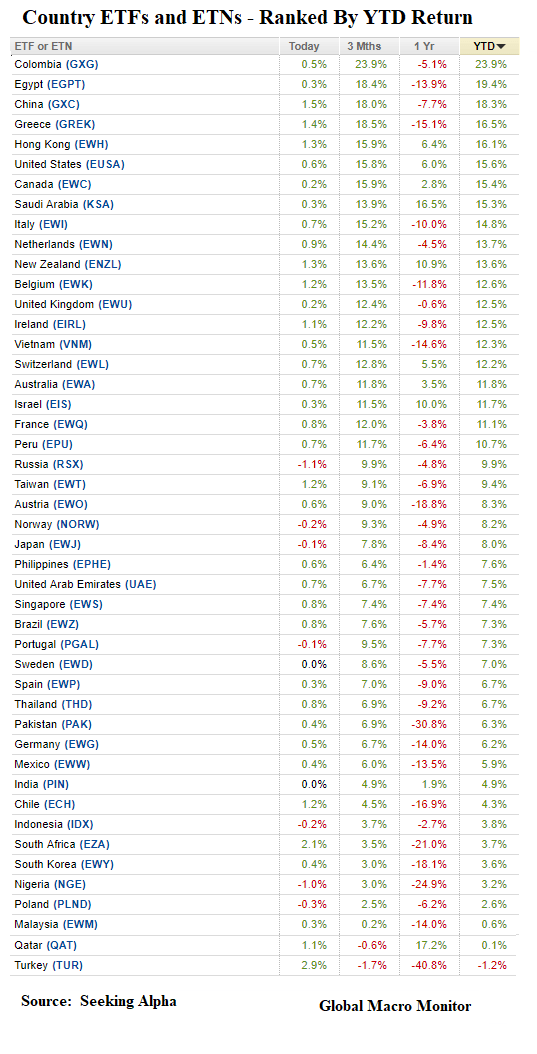

- All major stock markets up for the quarter with Nasdaq leading U.S. indices

- Semis and Homebuilders up 20 percent

- Crude oil up over 30 percent

- CRB up 8 percent. Where is the deflation?

Commentary: The stock market usually bounces after a down year as back-to-back down years are very rare. The Dow’s probability of an up 2019 is close to 90 percent.

Markets are way over their skis on the deflation and growth scare.

The Atlanta Fed’s GDP Now Q1 forecast has skyrocketed over the past few weeks, up from 0.3 percent to 1.7 percent. There is no deflation and it’s entirely possible the Cleveland Fed Median CPI prints 3 percent y/y in March with energy prices now skyrocketing. The daytraders in and out of the administration calling for a 50 bps rate cut are panicked and clueless unless they see something nobody else does. Could they be signaling the China trade deal is in trouble? Just askin’.

Moreover, if Trump closes border with Mexico bad economic news to come.

If the bottom is in with the China growth scare, bonds are in for a big pasting in the next quarter. An uptick in China will also help sentiment in Germany and Europe.

We expect the Q1 momo to continue in stocks, with the S&P making a nominal new high by year-end at around 3025, 2.85 percent above the all-time high, before the continuation of the bear market, which began in Jan 2018, and the next Big Dipper hits. This is based on a simple extrapolation of the momentum that takes place after such a strong first quarter after a down year.

The S&P500 finished March close enough for government work to our February 4th expectation, so we are taking a victory lap.

If history is any guide, given the historical start to the year, the S&P should finish March at or around 2850-ish. – GMM, Feb 4th

Happy hunting next week and the quarter, folks!

Pingback: Beware Of Retrofitting Fundamentals To Price Action | Global Macro Monitor

Pingback: Is “Obama Envy” Driving Trump’s Call For QE4? | Global Macro Monitor