BFTP: Blast From The Past

We posted the following last May when earnings and the market were all lathered up and on a sugar high induced by the corporate tax cut and weaker dollar in 2017. Our lack of confidence in earnings growth has been confirmed by the following chart.

We are expecting the S&P to make a nominal new high at around 3025 before the big dipper correction or a bear market. We posted a plethora of our concerns, including valuations, peak margins, too much public and corporate debt, demographics, tectonic shifts in geopolitics, and domestic politics. Add to that a bout of political instability coming this summer, the Summer of Discontent, as the Democrats move to impeach Trump after the revelations of the Mueller Report. Stay tuned.

How Sustainable Is Earnings Growth?

Not very.

We will leave the calculation for the entire stock market to the stock analysts.

Here’s why:

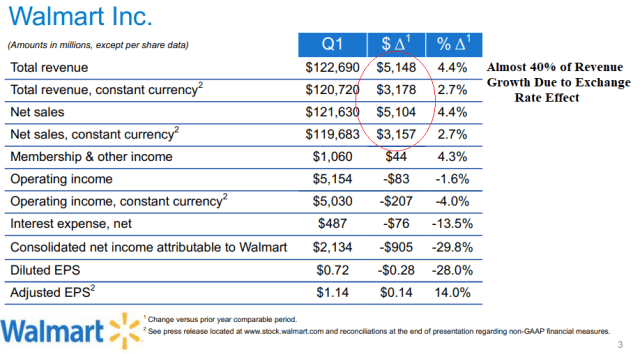

Just glancing over WalMart’s latest earnings release from the week, we see two one-off macro factors that helped WalMart’s earnings in Q1, and likely are the same for most companies:

- Foreign exchange rate effect

- The tax cut

Note that almost 40 percent of WalMart’s y/y revenue growth in Q1 was due to the exchange effect, and over 1300 bps of tax cut relief. That is one-offs.

Though the dollar was weaker in Q1, it has rebounded sharply in Q2. Thus a deleterious exchange rate effect is coming to Q2 earnings. Not to mention higher gas prices and interest rates, which will negatively impact the non-energy and non—financial sectors.

Pingback: Did Mueller Buy Or Sell Trump? | Global Macro Monitor