October Datafest

October is always a month of feasting for us macro data junkies as the IMF releases several of their annual reports and databases, such as the World Economic Outlook (WEO) and the Global Financial Stability Report (GFSR). We have a preference for the IMF economists as they don’t have a pom-pom/cheerleading bias in their analysis with a BTFD or “the market is cheap” tint to their narratives as do many sell-side and buy-side analysts, who almost always seem to be talking their books. Not all, but several.

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” — ― I, Candidate for Governor: And How I Got Licked

We know first hand as we’ve worked on all sides. At several Wall Street investment banks, hedge funds, and began our career at one the Bretton Woods institutions.

Academic Versus Market

The IMF and World Bank analysts have an academic bent, however, which also needs to be discounted. After working on Wall Street for a few years, I went back to Washington to speak with one of my professor friends about finding an arbitrage opportunity in a Korean mutual fund. He responded, “That is not supposed to happen, markets are too efficient” Yeah, right, I thought. Go talk with the Efficient Market Hypothesis (EMH) geniuses who blew up Long Term Capital Management (LTCM).

The moral of the story is, in general, don’t look to academics to help you understand real-world market dynamics to make money trading. They are very useful on the theory, however. But you can’t bend theory to fit market price action. Or, can you?

Finally, nobody knows the future so we are the first to admit and warn to heavily discount our opinions and market views. Take them into account with other counter-narratives and you use them to stress test your own views and portfolios.

Overvalued Markets

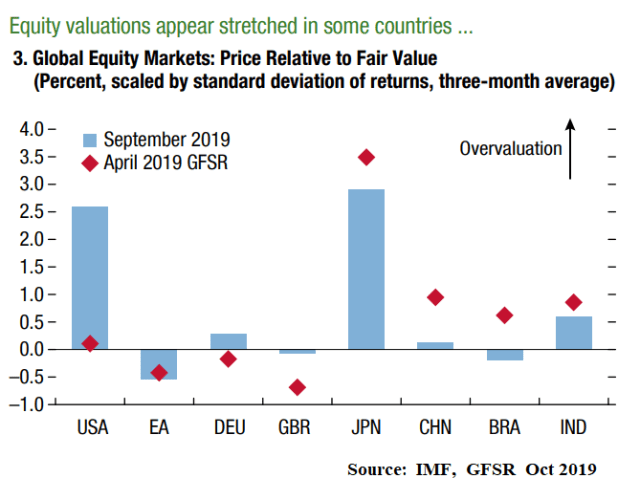

Here is the nice chart and a short excerpt from the recently released Global Financial Stability Report,

Other risk assets are also showing signs of stretched valuations. Equity markets appear to be overvalued in Japan and the United States (Figure 1.2, panel 3, shows misalignments scaled by monthly price volatility). Since April, US equity prices have increased whereas fundamentals-based valuations have declined as higher uncertainty about future earnings outweighed the boost from an expected rebound in earnings and lower interest rates. Equity valuations in major emerging markets, however, are closer to fair value, as investors’ risk appetite may have been tempered by concerns about trade tensions and the economic growth outlook (see Chapter 4)

The equity valuation models presented in this report are based on the dividend discount model(DDM), which explains equity prices as a function of expected corporate earnings, the compensation required to take on equity risk (the equity risk premium), and interest rates. – IMF, Anex 1.1. Technical Note

We’re not looking for confirmation bias but the above does confirm our bias that U.S. stocks don’t have much room to run to the upside. See our recent post, How Far Can The Stock Market Run?

Just because we and the IMF think the U.S. stock market is overvalued — using totally different metrics, by the way — it doesn’t rule out that stocks can’t break to new highs. Markets always do what they are going to do regardless of whatever the consensus or contrarians believe.

To buy higher, however, would be tantamount to picking up nickels in front of a steam roller and dangerous to your financial health, in our opinion.

Whither Japan

It is also stunning to see that Japan’s stock market is so overvalued.

The NIKKEI stock index is still 42 percent below its high 30-years after the December 29, 1989 peak of 38,957, even after 20 years of zero and negative interest rates (ZIRP & NIRP) and a massive quantitative easing (QE) program, which includes the central bank’s outright purchases of stocks (BoJ is on pace to become the largest shareholder of stocks) and the ballooning of the Bank of Japan’s balance sheet to where its size now exceeds the country’a GDP. Isn’t it obvious, QE forever is not going to save U.S. stocks in the long-run?

Imagine the politics and turmoil in the U.S. if the S&P500 is trading at the NIKKEI equivalent of 1745 in 2049? How would pensioners be living then? We can get a glimpse of how some of the Japanese elderly are surviving during their stock market’s long secular bear market and zero income on savings.

At a halfway house in Hiroshima – for criminals who are being released from jail back into the community – 69-year-old Toshio Takata tells me he broke the law because he was poor. He wanted somewhere to live free of charge, even if it was behind bars.

“I reached pension age and then I ran out of money. So it occurred to me – perhaps I could live for free if I lived in jail,” he says.

“So I took a bicycle and rode it to the police station and told the guy there: ‘Look, I took this.'”

…Toshio represents a striking trend in Japanese crime. In a remarkably law-abiding society, a rapidly growing proportion of crimes is carried about by over-65s. In 1997 this age group accounted for about one in 20 convictions but 20 years later the figure had grown to more than one in five – a rate that far outstrips the growth of the over-65s as a proportion of the population (though they now make up more than a quarter of the total). — BBC

That is fracking sad and one helluva social security program. You go, central bankers.

Though we are not expecting the U.S. markets and economy to follow the same path as Japan but the above does illustrate how difficult it is to predict the future. Ex-ante we tend to believe history progresses in a linear fashion. Ex-post we see it takes a non-linear path.

The Pacific Century

At peak Japan in 1989, for example, the shelves of bookstores were stocked with titles and themes similar to something to the effect, “The 21st Century Will Be The Pacific Century.” Open any one of them back then, read the cover and every author was certainly not focused on a Pacific dominated by China but one controlled by Japan.

Docile Population

Moreover, do you really think the U.S. population would be as docile as the Japanese if the S&P500 is trading at 1745 in 2049? We don’t.

Upshot

Question everything, including our analysis, take nothing for granted, don’t be complacent and stay alert, folks.

Running Out Of Free Lunches

We are almost out of free lunches, folks, and will be posting only sporadically unless your support increases. Donate whatever you think is fair by clicking on the PayPal button just below the Twitter and search icons on the upper right-hand side of the blog. You do not need a PayPal account and can use almost any credit card.

Don’t be a free rider. Thanks, so much.

BTFD…really? You think that is funny? Appropriate? Grow up.