I was just explaining to a close friend earlier today how gold can sometimes be a “Tower of Terror” trade where the bottom falls out of the price for no apparent reason. In addition, the metal is mainly driven by sentiment around a central bank’s long-term resolve and ability to maintain the currency’s purchasing power, which makes gold just a “date” and never a “long-term marriage.”

Gold Is Going Much Higher

Though we do expect this move to be a relatively long and thrilling date, with a not zero probability of morphing into a marriage.

Yikes!

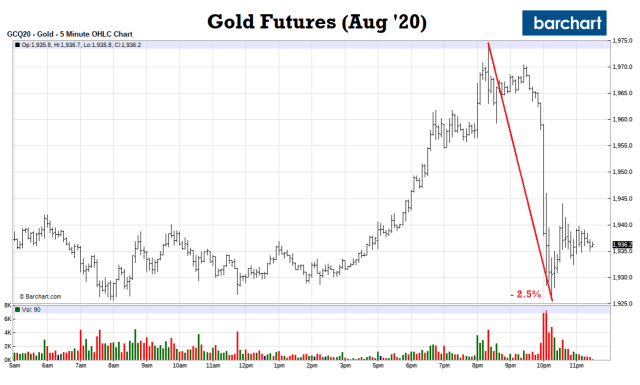

Before leaving for a walk tonight I see gold futures in Asian trading up to 2 percent after the New York close and fast approaching $2k. I come back and the price had fallen almost $50 from its high trade of $1975, or almost 2 1/2 percent in a little less than two hours.

Welcome to the “Tower of Terror,” Robinhooders.

The Tower of Terror

The Tower of Terror

The yellow metal is pretty overbought here and needs some consolidation before making its next move to $3000.

No Inflation?

Not so fast. There is no credit crunch and it feels, at least to us, there is inflation in the economy. Continued accommodation will result in more inflation and central banks really can’t do a damn thing about it.

This inflationary spike is unprecedented across all comparison years and constitutes more inflation than normally occurs in a year. We show that the increase in prices mainly happened in the first week of the UK’s lockdown (which began on 23 March 2020), and that a key driver was a reduction in the fraction of promotional transactions as retailers cut back on both price promotions and quantity discounts. This fall in promotions contrasts with the Great Recession, during which consumers purchased more on sale (see Griffith et al. 2016 for evidence in the UK, and Nevo and Wong 2019 for the US).

Second, we show that declining product variety strengthens inflation. Typically, inflation between two successive periods is computed by comparing the prices of products available during both periods. However, consumers’ effective cost-of-living is also impacted by the removal or entry of new products; all else equal, if less products are available consumers will be worse off. In Figure 2 we show the evolution in the number of unique products purchased per week in 2020 and in preceding years. Prior to the start of lockdown, and similar to previous years, the number of products sold in each week is stable. However, from the beginning of lockdown, there is a fall of around 8% in the number of products we observe purchased. This points towards a reduction in product variety, which erodes consumers’ effective purchasing power

…What lessons about the dynamics of inflation can be drawn from these findings? Lockdown coincided with unusually high inflation, which was experienced by almost all households and in almost all product categories. This finding is noteworthy given financial markets expect the COVID-19 pandemic to be a disinflationary shock (Broeders et al. 2020). The pervasive nature of the inflation, along with the fact that it is observed even in product categories with declines in output, point toward a risk of stagflation.

It is naturally too early to say for sure whether persistent stagflation will materialise. While the higher price level has persisted for several weeks, the inflation spike coincided with a one-time event, the beginning of lockdown; in addition, we do not observe the entirety of households’ consumption baskets (e.g. rents and services are not included). Nonetheless, it is crucial for central banks, fiscal authorities, and statistical agencies to closely monitor inflation risks going forward. Our work highlights the advantages of real-time scanner data for this purpose. One can track changes in spending patterns for disaggregate products in real-time and observe changes in promotion activity and product variety, all of which are important drivers of inflation and are typically overlooked by statistical agencies. – Voxeu

Yes, the study was done in the UK but the laws of economics know no borders and the thesis rings true in America too.