While the macro boys at GMM are off hunting Black Swans, I am making money to keep the lights on. – Carol K., GMM, August 11th

Yes, Carol K is correct, and we thank her for keeping the lights on at GMM. We do like hunting Black Swans though if purely defined we wouldn’t know what we are hunting. You know, the unknown unknowns thingy.

By the way, the three ETFs that Carol K. fancied in her August 11th post, Investing In The Economy Of The Future, are up 9.30 percent, 6.41 percent, and 11.95 percent vs. the S&P’s 1.90 percent. Thanks, CK, for subsidizing our trophy hunting.

Low Probability/High Impact Events

Living in the tails and being on the lookout for high sigma events, if you don’t already know by now, is our schtick. We are always searching for low probability/high impact events, which seem to be much more commonplace than statistics would suggest these days.

Treasury Rollover Risk Rising

Here’s a macro swan we recently discovered that really worries us and may help explain the spike in gold prices as Treasury rollover risk has increased markedly because of it.

Just so we don’t set the MMT crowd’s hair on fire, we will define rollover risk as the market becoming hesitant to refinance the $5 trillion of T-bills maturing in the next year, which will force the Fed to step up to monetize the maturing bills to prevent short-term yields from spiking and/or the government from defaulting, which, of course, will send gold to the moon and the dollar to the deepest parts of Hades.

Or, as Russia did in 1998 and Argentina chose to do recently, rather setting off an inflationary spiral — yes, inflation even with an output gap — the U.S. G could choose to default/restructure and reprofile its short-term debt. Highly unlikely but not impossible (if the political calculus favors it) as some suggest.

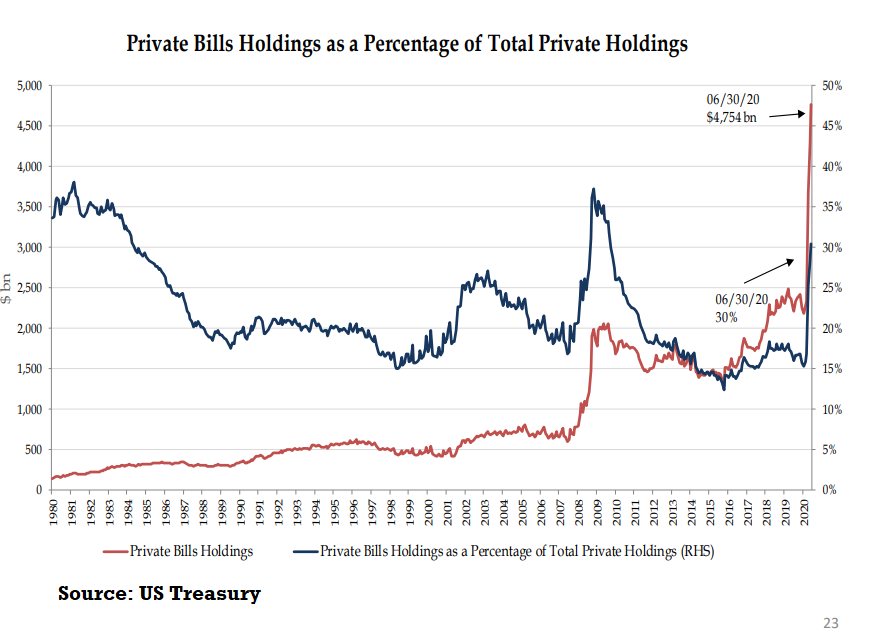

T-Bill Financing Spikes As Percent Of Total Marketable Debt

Take a look at the chart of the Treasury’s marketable debt profile held by the private sector (x/ Fed). Anyone who has worked in the emerging markets understands how dangerous it is for a sovereign to depend on short-term financing to fund a swelling budget deficit and a rapidly growing debt stock.

The current stock of T-bills outstanding is now around 26 percent of GDP compared to 14 percent during the last big spike during Great Financial Crisis (GFC).

Treasury officials do not seem concerned, however,

The recent rise in private sector savings is the largest on record and flows associated with that savings growth should continue to support private sector demand for T-Bills. – Treasury Presentation To TBAC

We are not as sanguine, however, as the spike in personal savings was largely the result of record government transfer payments.

Tepid “Real” Demand For Long Bonds

We understand the COVID crisis has put extraordinary stress on the U.S. budget, much of it will be temporary (fingers crossed), and at zero interest rates is essentially free financing for the taxpayer.

Moreover, yield curve management attempts to prevent interest rate spikes on the long end, which would result if the Treasury listened to the idjits who advocate a trillion-dollar issuance of 30-year bonds to finance, whatever.

My god, who is going to buy $1 trillion or even $100 billion of 30-year bonds at a 1.35 percent nominal yield or a negative real yield of around 50 bps? Expected inflation and breakeven rates are even distorted as the FED now owns over 18 percent of TIPs.

Benchmark U.S. Treasury yields surged to seven-week highs on Thursday after the Treasury sold a record amount of 30-year bonds to weak demand, the final sale of $112 billion in new coupon-bearing supply this week.

The Treasury sold $26 billion in bonds, up from $22 billion at its last quarterly refunding in May.

The debt sold at a high yield of 1.406%, around three basis points higher than where the debt traded before the sale. Primary dealers took a larger than average share of 28% of the bonds, indicating tepid demand from investors. The bid-to-cover ratio of 2.14 times was the lowest since July 2019. – Reuters, August 13th

Treasury Curve Distortion

Ground control to Investor Tom, take your reality pills, and put your thinking caps on. Current interest rates are relatively meaningless in terms of resembling anything close to fundamental reality or an economic signal.

There are few real money buyers of Treasury coupons at current rates.

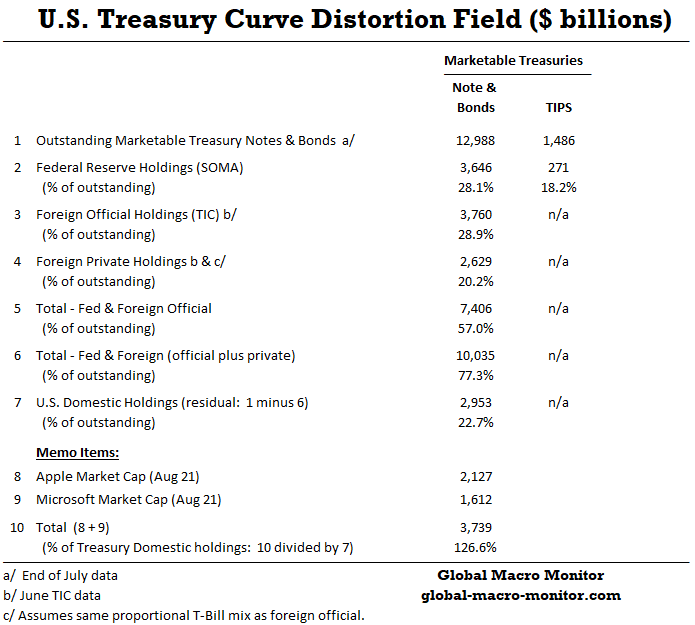

77 percent of Treasury Curve Held By Fed And Foreigners

The following table illustrates that both the Fed and foreign central banks hold 57 percent of the current stock of outstanding Treasury coupon securities, who have no sensitivity to market prices, are not directed by market forces except to keep asset prices elevated. Private foreign investors hold about 20 percent of the $13 trillion of marketable notes and bonds held by the public.

Together, the Fed and foreigners control over 77 percent of the Treasury curve, leaving a residual of only about $3 trillion held by domestic U.S. investors.

Apple & Microsoft’s Market Cap > Treasuries Held By U.S. Domestics

To further illustrate how distorted financial markets are Apple and Microsoft’s combined market cap, alone, at Friday’s close was 126 percent of the total stock of Treasury notes and bonds held by U.S. private domestic investors.

Now, what is the bond market telling us?

Still wondering why the financial markets are behaving like a whacko from Waco?

Hidden Faultline In Bills & May Show Up In Repo Market Again

Nonetheless, short-term T-bills will have to be paid off or rolled over. There is no free lunch and we suspect this is where a big potential problem hides.

As the above chart shows, T-Bills have gone from about 15 percent of a much smaller stock of total marketable debt at the end of January to 30 percent of outstanding Treasury securities privately held at the end of June, while the total stock of marketable debt has increased by 19 percent in just five months.

Declining Trend In Bid-to-Cover Ratios

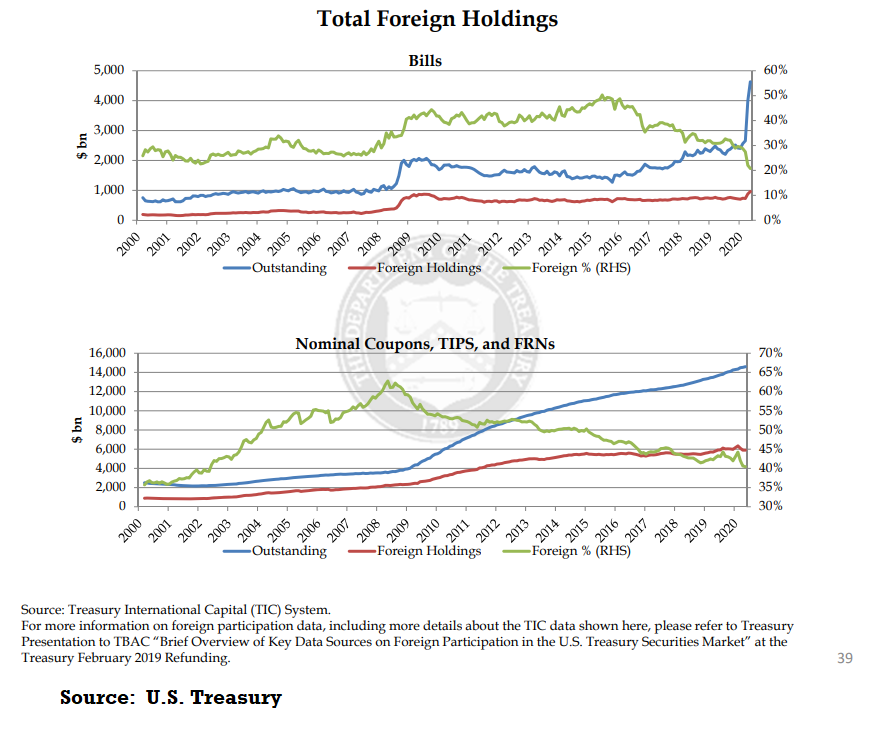

The Bid-to-Cover ratio for bills has been in a declining trend over the past decade.

Could it because they now yield zero percent? However, T-Bills yielded zero percent during the first ZIRP road trip, which lastest for almost five years after the Great Financial Crisis (GFC) so something else must be going on. We are open to suggestions.

Contrary to conventional wisdom the relative demand for Treasury securities by foreigners has been waning. Foreign holdings of U.S. T-bills has declined from over 50 percent of the total stock to around 20 percent over the past five years. Moreover, the percentage of foreign holdings of Treasury coupon securities, TIPs, and FRNs have fallen from as high as 60 percent of the total stock to 40 percent, levels not seen since the early aughts.

Though foreign central banks still hold about 28 percent of the stock of coupons, the Fed has really stepped up as the marginal buyer during the COVID crisis, increasing its holdings of notes and bonds from $2.384 trillion at the end of January to $4.177 trillion by end-June. During the same period, foreign central banks have reduced their holdings from $3.875 trillion to $3.760 trillion.

Upshot

The global financial markets are extremely distorted primarily due to how central banks have manipulated their government bond markets. Because the U.S. remains the world’s dominant reserve currency, foreign central bank recycling of their foreign exchange reserves back into the U.S. Treasury market has, for many years, further distorted U.S. interest rates.

The COVID crisis and the subsequent huge financing requirements of the U.S. Treasury have created anomalies in how the government finances itself, including an over, and what we deem a potentially dangerous, dependence on short-term debt. This is a faultline on nobody’s radar.

There you have it, folks, now you’re in the know. It’s no longer a Black Swan.

Gold, baby!

Thanks for the post and great analysis as always.

I understand the current macro setup favors gold as an good investment choice, especially the exposure of the institutional and generalists to gold/ miners is still low.

however, what always puzzle is the valuation of gold..i understand different investors use different metric to value, like Tudor Jones used the ratio of gold above ground to global M1 as a reference.

do you have a valuation framework of gold? and I understand gold has upside, do you also look for gold miner opportunity? although some recent news flow of miners (buffett purchased stakes of Barrick) and gold ETF (GDX and GDXJ) has recorded good return YTD, the cumulative fund flow from Jan 19 to now, of Gold miners still negative (-1.9 billion USD) while paper gold +40.1 billion inflow..

thanks as always

Thanks for the comments, brother. I don’t really have a gold valuation metric and trade it mostly as a debasement trade. Have used the growth of the global monetary base in the past, however.

If the Fed is or expected to debase the currency by printing digital money it’s the season to be long. If that changes or expectations change, get the heck out of Dodge. Only look the metal and don’t trade miners, though more leverage there is more basis risk. Gold always date and never a marriage. This date looks like it may last a while. Also note gold is a Tower of Terror trade. See my post below. Cheers, bro.

How do you think about timing for this event? I don’t know the credit markets too well but is this a 12/31/2020 refi risk event? Q2 of 2021?

Pingback: This Week’s Best Investing Articles, Research, Podcasts 8/28/2020 - Stock Screener - The Acquirer's Multiple®