Markets wrapped up the week with a paradoxical sense of calm, even as trade tensions re-escalated on multiple fronts. At the center of the uncertainty is President Donald Trump’s hardline tariff rhetoric, including threats of sweeping new levies on the United States’ major trading partners. While markets continue to discount his threats as political theater, the cumulative weight of uncertainty is beginning to test investor patience, especially during the traditionally sluggish “Dog Days of Summer.” Artificial intelligence (AI) trends remain a bright spot for sentiment, but beneath the surface, warning signs are emerging.

Trump’s Renewed Tariff Push: Big Talk, Real Risks

In a sharp escalation, Trump announced unilateral tariff hikes—30% on the EU and Mexico, 50% on Brazil and copper products, and threats of a 200% pharmaceutical levy. The stated justification ranges from narcotics enforcement to trade imbalances, with timing set for August 1. According to Bloomberg, Trump’s “maximalist stance” has left U.S. trading partners scrambling, with some countries (like India) racing to finalize partial deals to avoid being swept up in the tariffs.

Despite the aggressive tone, markets appear to view the latest salvo as another bluff. Traders point to a pattern of bluster followed by walk-backs. Nonetheless, the barrage of tariff letters and the rapidly approaching deadline have rekindled fears of a disrupted global trade regime. As one European official stated, the administration’s “fits-and-starts” approach undermines predictability and stability, the two pillars essential for cross-border investment and supply chain resilience.

Muted Market Reaction: Complacency or Confidence?

While geopolitical rhetoric intensified, market volatility remained surprisingly subdued. Fidelity, Manulife, and Schwab all reported relative calm in U.S. equity indexes. The VIX actually backed up for the week. The S&P 500 and Nasdaq continued to trade near record highs, buoyed by robust AI demand and resilient tech earnings. Yet the calm may be deceptive.

Charles Schwab’s weekly outlook noted that equity valuations remain historically elevated, and market breadth is narrowing again, another potential red flag. The latest leg of the rally has been disproportionately driven by a handful of tech giants, even as cyclical and value sectors lag. The fear is that a deterioration in macro fundamentals, such as renewed supply chain stress from tariffs, could derail the rally just as seasonal volume declines.

Trade Tensions Not Fully Priced In

Although U.S. growth remains supported by fiscal tailwinds, tariff uncertainty is starting to bite. EM Asia policymakers, in particular, are losing faith that trade deals will provide lasting clarity, and sentiment in Europe is dampened by intra-bloc political gridlock. Moreover, supply bottlenecks in global logistics remain unresolved, a risk exacerbated by tariff-driven inventory hoarding or re-routing.

While inflation in Latin America and Japan appears contained, China’s deflationary trends are complicating trade negotiations, especially as Trump’s protectionist pivot collides with Asia’s need for export recovery.

The AI Effect: Cushioning Sentiment for Now

Despite the macro clouds, the AI narrative continues to support risk appetite as investor positioning remains heavily skewed toward AI-linked assets. This thematic allocation may be shielding markets from near-term shocks, creating a perception of resilience that may not be sustainable if tariffs begin to impact input prices or corporate margins.

Conclusion

As markets wade deeper into summer, the surface calm belies an undercurrent of growing tension. Trump’s tariff revival is unlikely to deliver an immediate economic shock, but the cumulative uncertainty may begin to seep into corporate planning, consumer sentiment, and investor allocation. With AI momentum still masking fragility in other sectors, the coming weeks will test whether markets can continue to brush off policy volatility or whether the dog days will give way to a stormier season ahead. Portfolio managers would be wise to remain nimble, hedge trade-sensitive exposures, and monitor developments with vigilance as August 1 approaches.

Markets

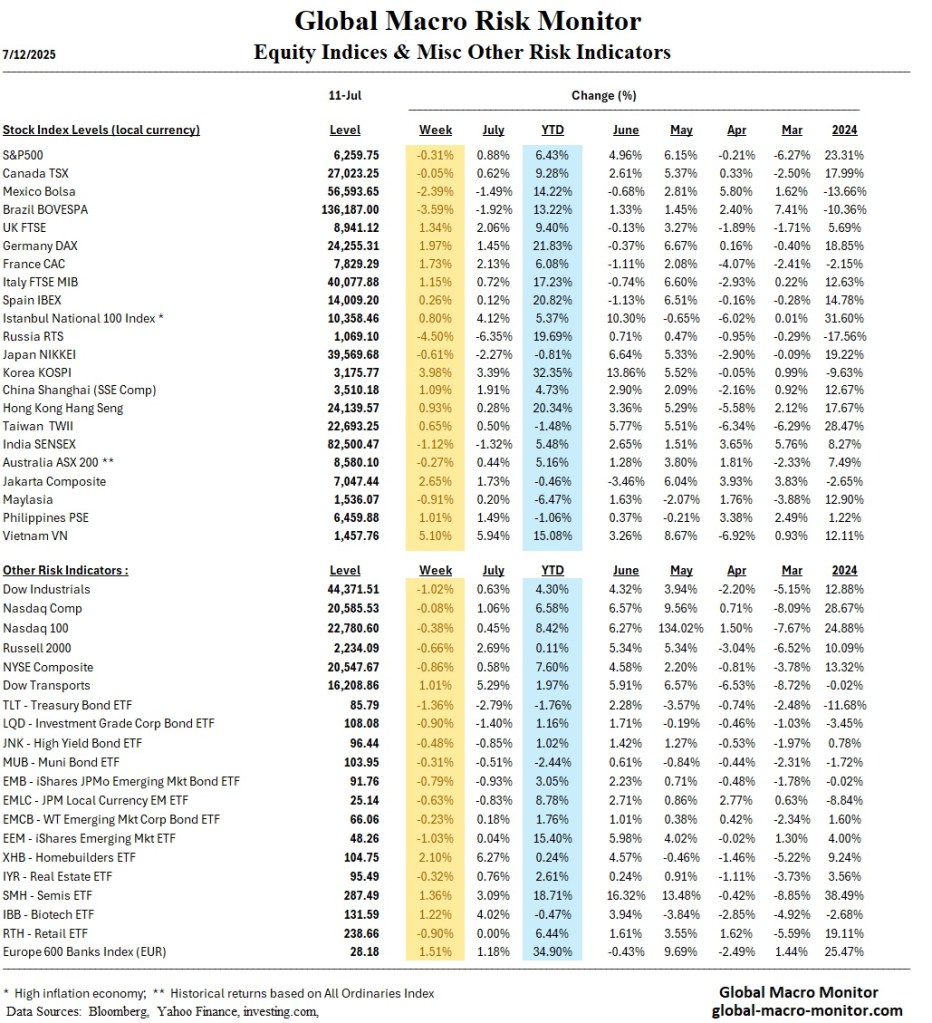

U.S. equities showed mixed performance, with major indexes retreating modestly due to renewed tariff headlines and seasonal trading lulls during the summer.

Nvidia hit a $4 trillion market cap, helping offset declines in broader sectors.

Oil prices rebounded, climbing more than 3% following a sharp drop the previous week, signaling continued volatility in energy markets.

Market breadth remained narrow, as gains were concentrated in mega-cap technology stocks.

U.S. Market Analysis

President Trump’s tariff threats targeted key sectors, including copper (50% increase), soybeans (23%), and autos. The proposed hike on Brazilian tariffs to 50% signals a shift toward broader trade protectionism.

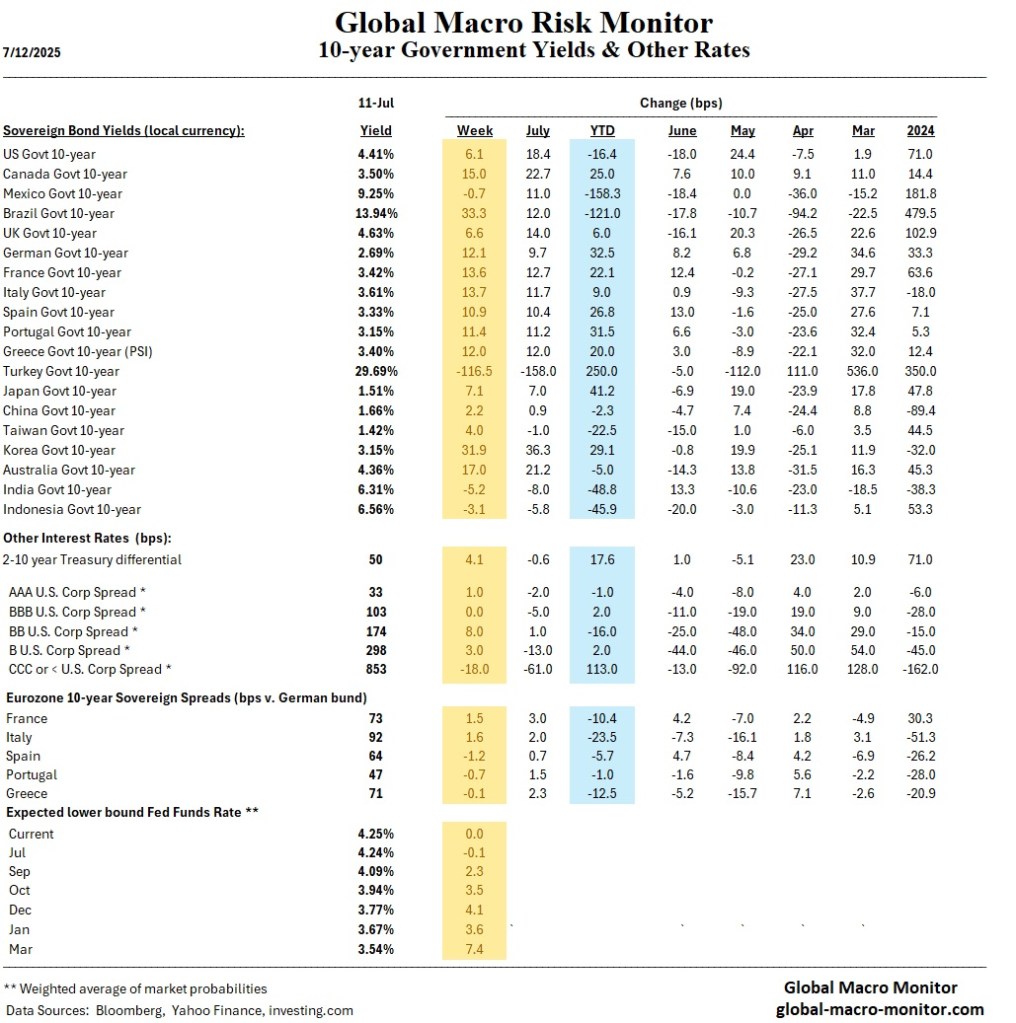

Fed minutes revealed a divergence in outlook, with most members supporting rate cuts, but the timing remains contested.

Treasury yields rose slightly, with strong investor demand for 10-year notes; corporate bonds underperformed Treasuries.

FOMC outlook indicates cautious optimism, tempered by trade and global uncertainty.

Global Market Analysis

Trade policy uncertainty intensified, as reciprocal tariffs and delayed negotiation timelines clouded visibility for multinational supply chains.

EU political tensions escalated, with disagreements over the next Multiannual Financial Framework (MFF) and national budgets, especially in France.

Japan saw positive wage and inflation trends, supported by accommodative monetary policy and resilience despite trade tensions.

China’s economy remains under deflationary pressure, as June PPI declined and CPI stayed low. Consumer confidence remains fragile.

Economics

U.S. data continues to show resilience, but early signs of softening are emerging in housing and employment metrics.

UK GDP contracted in May, yet second-quarter growth projections remain positive. Cooling in labor market conditions has been noted through alternative datasets.

Latin America saw benign inflation readings, especially in Brazil and Mexico, paving the way for continued monetary easing.

Emerging markets are grappling with policy response uncertainty, especially in Asia, where expectations for trade stabilization remain low.

Week Ahead (July 14–19)

Key U.S. Events

Economic Data:

Monday: CPI (Consumer Price Index)

Tuesday: PPI (Producer Price Index, Final Demand)

Wednesday: Industrial Production, Jobless Claims, EIA Petroleum Status Report

Thursday: Housing Starts, Philadelphia Fed Manufacturing Index

Friday: Consumer Sentiment (Preliminary)

Earnings Reports:

JPMorgan Chase, Wells Fargo, BlackRock, Johnson & Johnson, and Bank of America to report earnings.

Key Global Events

Eurozone: Continued debates on fiscal integration and tariff alignment within the bloc.

Japan: Corporate sentiment and trade data will be key, particularly under the yen’s depreciation.

China: Key employment and wage data expected; markets watching for any new stimulus signals.

this market appears to be schizophrenic and on its mood stabilisers.