-

In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.

-

Join 1,203 other subscribers

Contribute To GMM

Categories

- 3D Printing

- Agriculture

- AI

- Algos

- Apple

- Automation

- Banking

- BFTP

- Bitcoin

- Black Swan Watch

- Bonds

- Brazil

- Brexit

- BRICs

- Budget Deficit

- Capital Flows

- Cartoon of the Day

- Cashless Society

- Chart of the Day

- Charts

- China

- Clean Tech

- Climate Change

- Coach C

- Commodities

- Coronavirus

- COVID

- Credit

- Crude Oil

- Currency

- Cyprus

- Daily Risk Monitor

- Day In History

- Debt

- Demographics

- Disinflaton

- Dollar

- Earnings

- ECB

- Economics

- Economist

- Egypt

- Electric Vehicles

- Emerging Markets

- Employment

- Energy

- Environment

- Equities

- Equity

- Euro

- Eurozone Sovereign Spreads

- Exchange Rates

- Fed

- Finance and the Good Society

- FinTech

- Fiscal Cliff Monitor

- Fiscal Policy

- Food Prices

- France

- Futurist

- Game Theory

- General Interest

- Geopolitical

- Geopolitics

- German Bund

- Germany

- Global Macro Watch

- Global Reset

- Global Risk Monitor

- Global Stock Performance

- Global Trend Indicators

- Gold

- Greece

- Healthcare

- Heat Map

- Hedge Funds

- Housing

- Human Interest

- Immigration

- Impeachment

- India

- Inequality

- Inflation/Deflation

- Infographics

- Innovation

- Institutional Investors

- Interest Rate Monitor

- Interest Rates

- Interviews

- Italian Yields

- Italy

- Japan

- Jobs

- Lectures

- Macro Notes from Conference Calls

- Manufacturing

- Masters

- Mexico

- Monetary Policy

- Movies

- Muni Bonds

- Muni Market

- Natural Gas

- News

- Nonlinear Thinking

- North Korea

- Overbought Markets

- Picture of the Day

- PIIGS

- PMIs

- Policy

- Politics

- Population

- Populism

- Poverty

- President Trump

- Qunat Strategies

- Quote of the Day

- Quotes

- Rare Earth Elements

- Readership

- Reads

- Real Estate

- Relative Strength Index

- Robert Shiller

- RSIs

- S&P500

- Sector ETF Peformance

- Semiconductor prices

- Semiconductors

- Social Media

- Socialism

- Song for the Week

- Sovereign Debt

- Sovereign Risk

- Spain

- Sports

- State and Local Government

- Tail Risk

- Technical Analysis

- Technology

- The Big Reset

- The Weekend Read

- This Day In Financial History

- Trade War

- Trades

- Tweet of the Day

- Ugly Chart Contest

- Uncategorized

- US Releases

- Video

- Volatility

- Wages

- Week Ahead

- Week in Review

- Weekend Reads

- Weekly Eurozone Watch

- Whales

-

Recent Posts

Meta

Masters Week: Jack and German POWs (BFTP)

BFTP: Blast From The Past

Answer to yesterday’s Masters quiz question:

Anthony Kim posted 11 birdies in the second round of the 2009 Masters.

German WWII POWs

Here’s some more 19th hole fodder to impress your buddies and something I bet you didn’t know about Augusta:

German POWs from nearby Camp Gordon built the bridge over Rae’s Creek next to the 13th tee box during WWII. They were part of Rommel’s Panzer division in North Africa responsible for building bridges to enable tanks to cross rivers.

While Augusta National is famed for its almost unnaturally beautiful flora, as it turns out some rather interesting fauna once called the course home as well: 200 heads of cattle and more than 1,400 turkeys. From 1943 until late 1944, Augusta National was closed for play and transformed into a farm of sorts to help support the war effort. Some of the turkeys were given to club members during Christmas (meat rations were in effect) while the rest were sold to local residents to help fund the club. And the cows? Well, they acted as natural lawnmowers but also inflicted quite a bit of damage to Augusta National, devouring many of the course’s famed plants and shrubs.

To help repair cattle-related damage and revive Augusta National for its reopening, 42 German prisoners of war from nearby Camp Gordon were shuttled back and forth to work on the course.

Writes John Strege in “When War Played Through: Golf During World War II:”

“The POWs had been with the engineering crew serving Rommel, the Desert Fox, in North Africa, part of the Panzer division responsible for building bridges that enabled German tanks to cross rivers. It was a useful skill for the renovation work to be done at Augusta National. The Germans were asked to erect a bridge over Rae’s Creek adjacent to the tee box at the thirteenth hole.”

The Masters resumed at Augusta National — now free of German prisoners and barnyard animals — in 1946. And interestingly enough, the Supreme Commander of the Allied Forces in Europe during World War II, Dwight D. Eisenhower, later became a member of Augusta National. Two Augusta National landmarks bearing Eisenhower’s name still stand today: the Eisenhower Tree (a loblolly pine at the 17th hole that the former president and avid golfer repeatedly struck with golf balls and requested be cut down; photo above) and the Eisenhower Cabin (built in the 1950s according to Secret Service security guidelines by the club for the former president’s visits).

Posted in Masters

Tagged Anthony Kim, art, books, Food, German POWs, Jack Nicklaus, Masters, News, Sports

Leave a comment

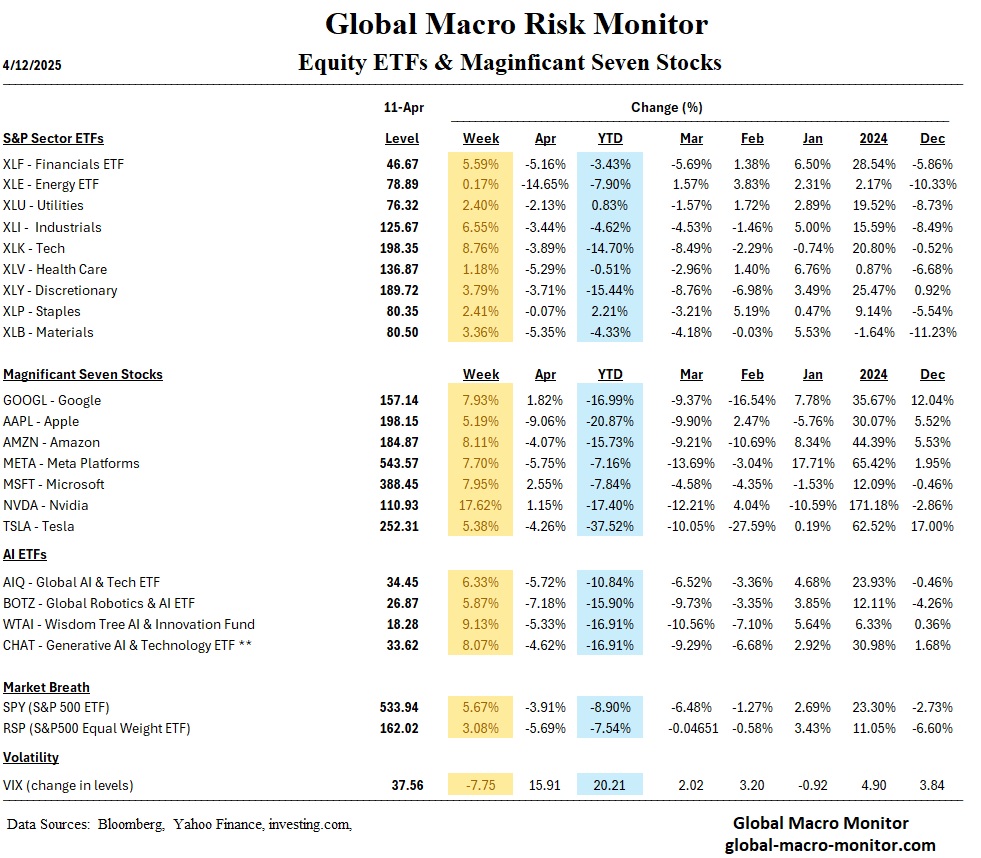

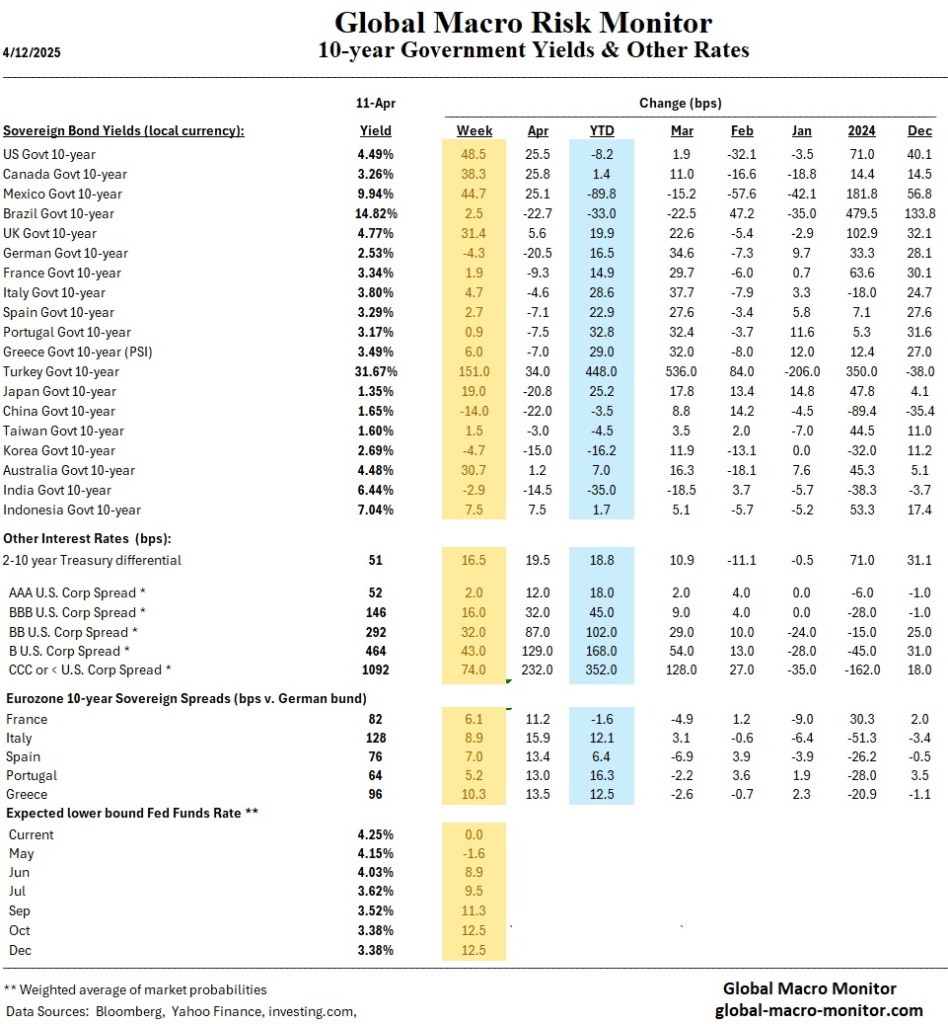

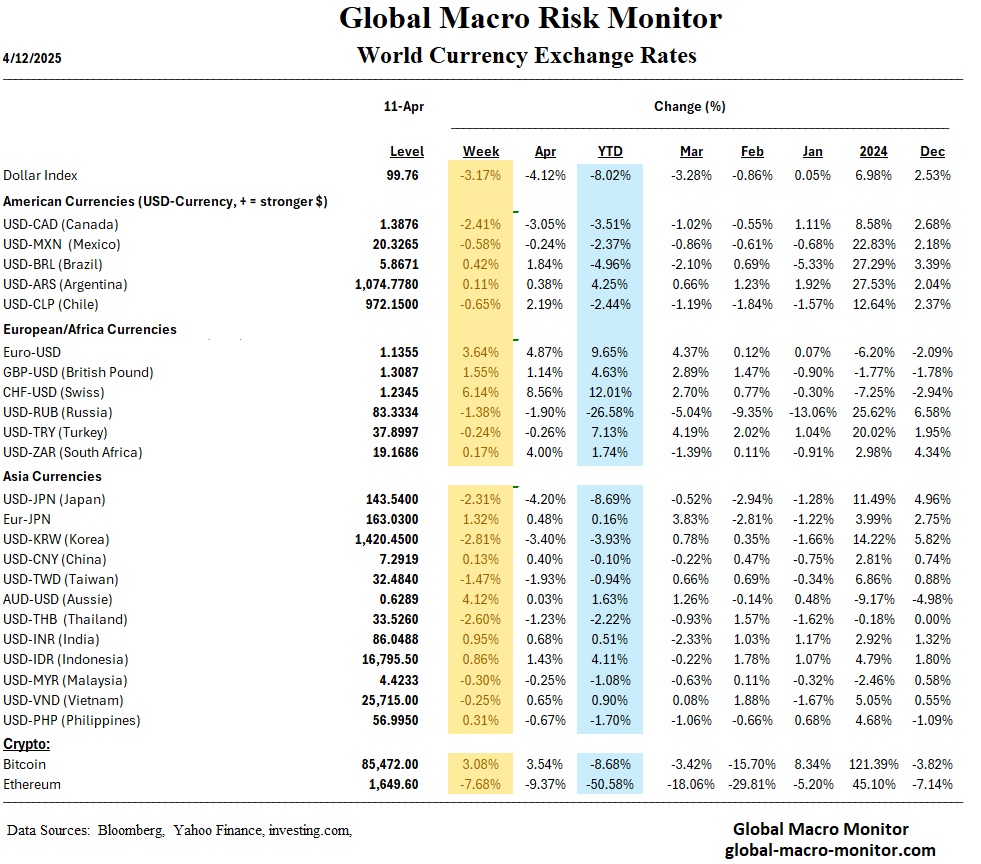

Global Risk Monitor: Weekly Update – April 11

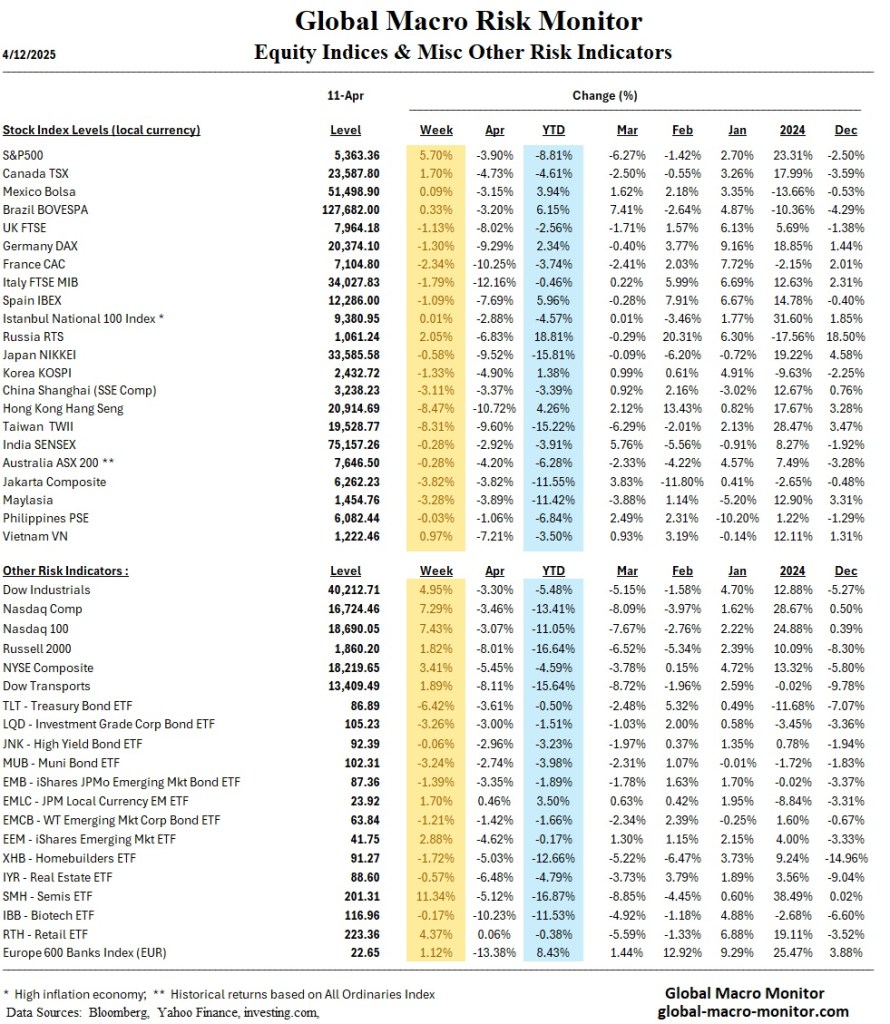

The United States’ current tariff regime reveals not a strategic plan but an erratic response to market volatility, suggesting a governing philosophy resembling reactive day trading more closely than structured economic policymaking. As the week’s developments show, the absence of a coherent framework has amplified financial instability and is now beginning to erode the traditional safe-haven status of U.S. assets. The dramatic 50 basis point surge in U.S. Treasury yields—contrasting with a 4 basis point decline in German bunds and a 6.1% appreciation of the Swiss Franc—signifies an unsettling reality: capital is fleeing the U.S. in patterns more commonly associated with emerging markets in crisis.

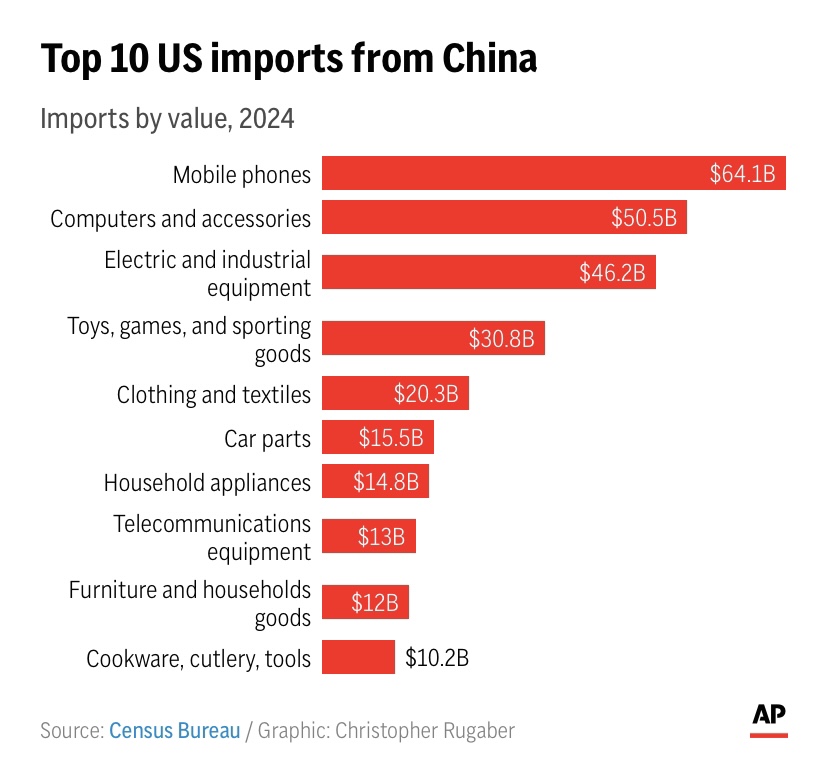

This capital flight reflects growing investor anxiety over both the economic impact and political incoherence of U.S. trade policy. In particular, the decision to impose sweeping and massive tariffs on China —then abruptly exempting $390 billion in consumer electronics, including smartphones and chips —undermines confidence in policy predictability. As revealed in the Friday night tariff exemption announcements, the White House walked back its own levies under intense market pressure, with Apple, Nvidia, and Microsoft among the major beneficiaries. While this move will spark another positive market response early next week, it also reinforces the perception that policy is being dictated by equity indices, not long-term economic goals.

Meanwhile, U.S. credit spreads widened significantly, Treasury market volatility surged, and equities remain fragile despite a mid-week bounce. The broader implication is troubling: without a principled policy reversal, not merely ad hoc relief, U.S. markets may remain hostage to political instability and stagflationary risk. If change comes, it will be driven not by strategy, but by necessity.

Markets

U.S. Market Analysis

- Wild Rebound, but Breadth Collapses: U.S. indices bounced midweek (S&P 500 +5.7%, Nasdaq +7.3%), but participation was narrow—SPX breadth fell to 26.4% from 37.4%.

- Volatility High: The CBOE Volatility Index surged early in the week, peaking at 5-year highs before subsiding.

- Yields Spike: 10-year yields jumped from 3.99% to 4.51%. The yield curve steepened sharply.

- Credit Spreads Widen: IG spreads +8 bps to 102 bps; HY spreads +50 bps to 387 bps.

- U.S. Dollar Weakens: DXY briefly broke below 100, compounding uncertainty.

Global Market Analysis

- Europe: STOXX 600 –1.9%. Germany’s DAX –1.3%, Italy’s FTSE MIB –1.8%. Bunds rally. ECB signals concern over global trade risks.

- Asia:

- Japan: Nikkei and TOPIX each down ~0.6%. Tariffs spook exporters; BoJ may delay rate hikes.

- China: Shanghai Composite –3.1%. China raised retaliatory tariffs to 125%. GDP growth forecast cut to 4.1%.

- Emerging Markets:

- Latin America: Mixed impact—some relief from tariff exemptions (e.g., metals), but vulnerable to commodity weakness.

- EEMEA: Less exposed directly, but capital flow and FX volatility remain elevated.

Economics

U.S. Economic Overview

- Consumer Sentiment Collapses: University of Michigan’s Index fell to 50.8, lowest since 2022. Inflation expectations jumped to 6.7%—highest since 1981.

- CPI & PPI Soft, but Misleading: March CPI flat m/m, Core CPI +0.1%. PPI also declined, but these reflect pre-tariff conditions.

- Fed Outlook Muddled: Rate cut odds for June remain high, but hawkish commentary persists amid inflation uncertainty.

- Yield Moves Defy Inflation Prints: Bond yields rose despite soft data, suggesting market concern over structural risks—not cyclical weakness.

Global Economic Overview

- Eurozone: March CPI eases to 2.2%. ECB expected to cut rates Thursday. Recession risk rising.

- China: Tariff impacts to trim 1–3 pp off GDP. Beijing expected to roll out new fiscal stimulus.

- Japan: Tankan survey firm; BoJ cautious. Yen appreciated on global risk aversion.

- India: RBI cuts rates 25 bps. More easing likely as GDP downgraded.

- Mexico & Brazil: CPI supports further easing; Banxico likely to cut in May.

Week Ahead (April 14–18, 2025)

Key U.S. Events:

- Economic Data:

- Tue (Apr 15): Empire State Manufacturing, Import/Export Prices

- Wed (Apr 16): Retail Sales, Industrial Production, Housing Market Index

- Thu (Apr 17): Housing Starts, Jobless Claims, Philly Fed Index

- Earnings:

- Mon: Goldman Sachs, M&T Bank

- Tue–Fri: J&J, BAC, Citi, UNH, Schwab, AXP, DHI, Comerica, and more

Key Global Events:

- China GDP: Wednesday—expected slowdown from late-2024 strength.

- ECB & BoC Rate Decisions: Thursday (ECB cut expected); Wednesday (BoC to hold).

- Tariff Watch: Any update on China-U.S. trade dynamics will drive markets.

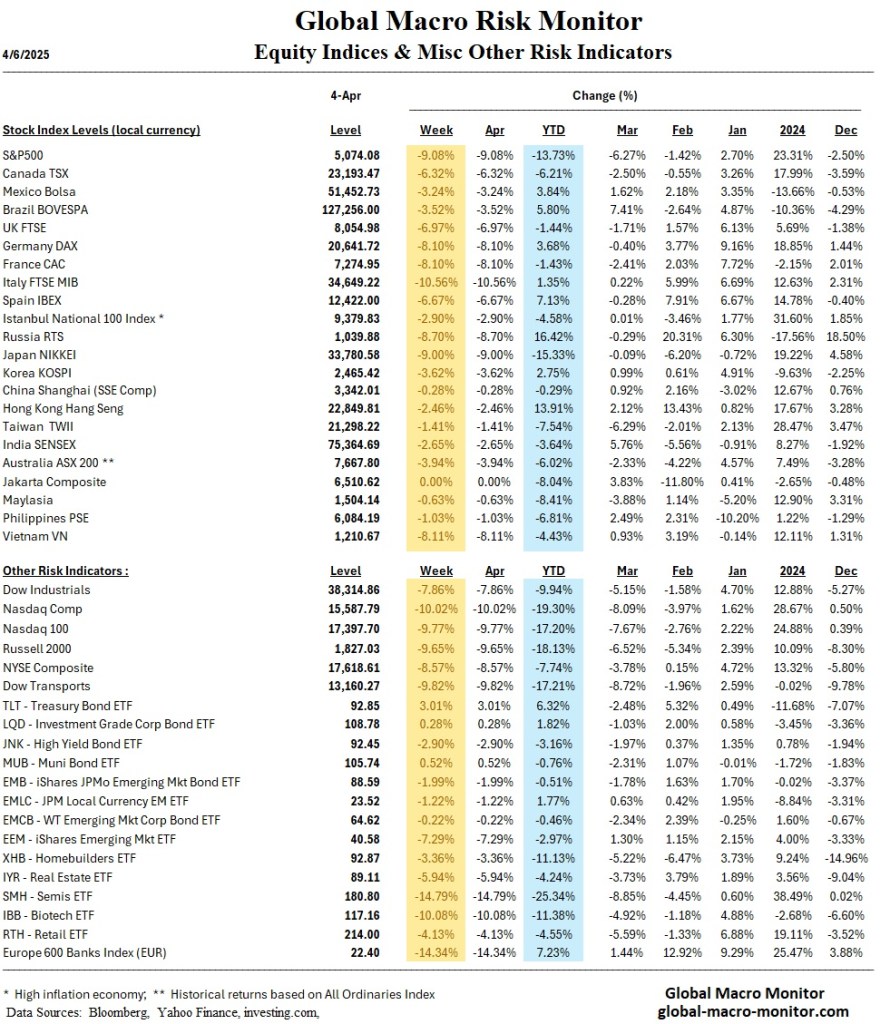

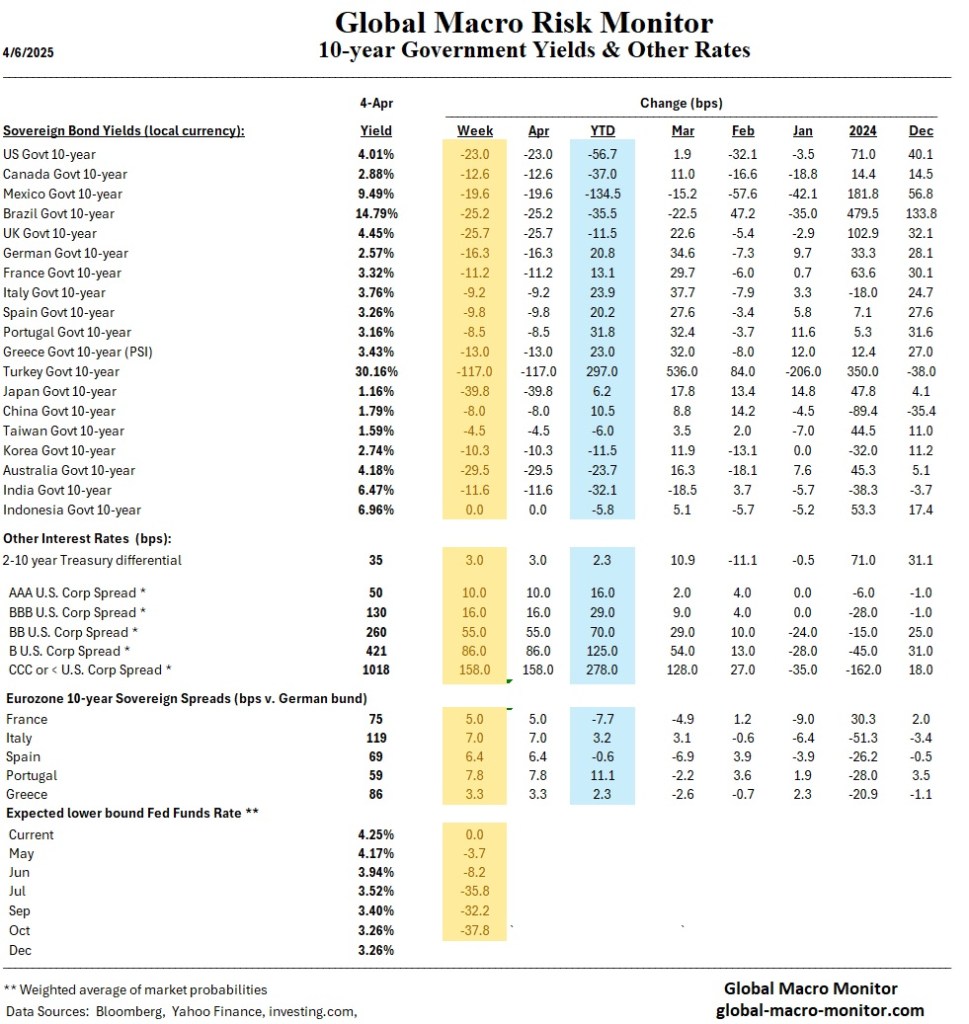

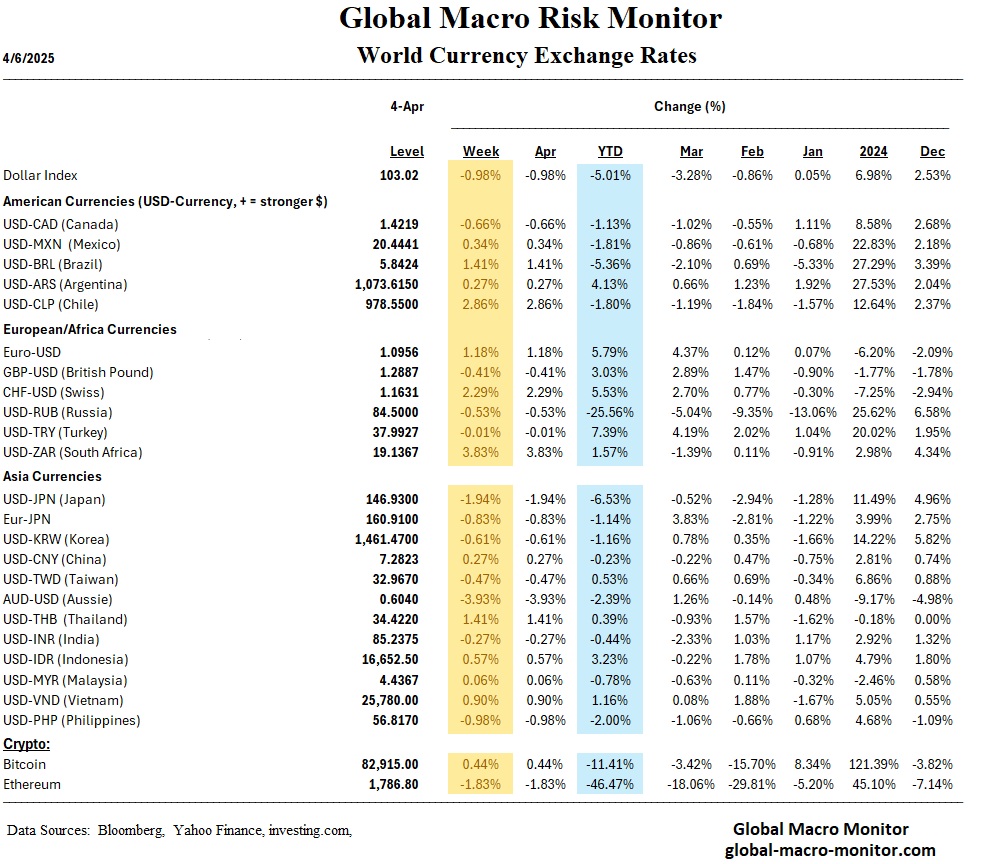

Global Risk Monitor 2.0: Week In Review – April 4

Our earlier GRM post mistakenly included data tables from the week of March 28th. Here are the up-to-date April 4th tables.

The U.S. Administration’s tariff policy represents a critical policy error that has upended financial markets and raised the specter of a severe recession and a prolonged bear market, with no clear bottom in sight. The imposition of sweeping, unilateral tariffs under the guise of reciprocity has rattled global trade systems and injected significant uncertainty into economic forecasting. Unless swiftly reversed, these actions risk anchoring inflation while simultaneously constricting growth—a classic stagflation trap that could force the Federal Reserve into an unenviable position and prevent equity markets from stabilizing in the near term.

At the heart of this miscalculation lies a series of incompatible objectives. The Administration claims the tariffs are designed to ensure fair trade, revive domestic manufacturing, and raise Treasury revenues. However, these aims are mutually exclusive in practice. Fair trade typically implies mutual reductions in barriers, not escalations. Promoting domestic manufacturing by taxing intermediate inputs only raises costs for U.S. producers, undermining competitiveness. Furthermore, the notion that tariffs will substantially boost Treasury receipts is flawed, as reduced trade volumes and retaliatory actions abroad are likely to erode revenue gains.

The strategy’s incoherence is evident in absurd measures such as, for example, a tariff on coffee, an import for which the U.S. lacks viable domestic production except de minimis production in Hawaii and Puerto Rico. These policies reflect a reactive, politically charged agenda rather than a cohesive economic strategy. Ultimately, market forces are likely to compel a reversal. Only sustained capital flight and a prolonged earnings recession may bring the necessary pressure to correct course and restore stability.

Doesn’t the Administration understand the most basic concept of international trade and economics – Comparative Advantage?

Markets

U.S. Market Analysis

- Sharpest Sell-off in Years: U.S. equities suffered their worst weekly decline since 2020 following unexpectedly aggressive tariffs announced by the Trump administration. The S&P 500 dropped over 9%, Russell 2000 entered bear market territory, and the Nasdaq fell 10%.

- Small-Caps Hit Hard: The Russell 2000 dropped over 10% this week and is down more than 30% from its all-time high.

- Investor Sentiment & Breadth Deteriorated: Market breadth collapsed with fewer stocks trading above their 200-day moving averages; SPX breadth fell to 37.4%.

- Bond Yields Plummet: 10-year Treasury yields fell below 4% (from 4.2%) due to flight-to-safety demand, marking the largest weekly gain for bonds in seven months.

- Bitcoin Resilience: In a break from past behavior, Bitcoin held steady (~$83K) despite the broader market’s sell-off.

- Credit Spreads Widen Sharply: Investment grade spreads widened by 8 bps to 102 bps, and high-yield spreads rose 50+ bps to 387 bps—signaling rising recession fears.

Global Market Analysis

- Europe: STOXX Europe 600 fell 8.4%, led by Italy (–10.6%) and Germany (–8.1%). The ECB faces growing pressure to cut rates amid slowing inflation and trade uncertainty.

- Asia:

- Japan: The Nikkei 225 dropped 9% and TOPIX lost 10%. A 24% U.S. tariff on Japanese imports spooked markets, delaying expected BoJ rate hikes.

- China: The Shanghai Composite dipped modestly (–0.3%), while retaliation included 34% tariffs on U.S. goods, rare earth export limits, and trade bans on some U.S. firms.

- Emerging Markets:

- Emerging Asia: GDP forecasts cut due to tariffs; deeper and earlier monetary easing expected.

- Latin America: Spared from direct tariffs but vulnerable to falling global demand and commodity prices.

- EEMEA: Limited direct exposure to U.S. tariffs but still faces slower global trade and capital flow risks.

Economics

U.S. Economic Overview

- Jobs Report Strong, But Overshadowed: March nonfarm payrolls surged by +228K (vs. 130K est.), but the unemployment rate edged up to 4.2%. Strong healthcare and hospitality hiring offset weak federal employment and temporary jobs.

- Inflation Risks from Tariffs: ISM Manufacturing PMI fell back into contraction (49.0), and Services PMI slipped to 50.8. Tariffs have pushed input prices higher.

- CPI Outlook: March CPI is expected to show flat m/m inflation, but looming tariffs will likely reignite inflation over the coming months.

- Rate Cut Expectations Rise Sharply: Markets now price in ~113 bps of Fed rate cuts in 2025, with 4 cuts expected and a December Fed Funds rate of 3.26%. A May cut has a 43% probability; June is fully priced.

- Trade Deficit Stubbornly High: February trade deficit remained elevated at $122.7B as firms rushed to import ahead of tariffs.

Global Economic Overview

- Eurozone: Inflation eased to 2.2% with slower services inflation. ECB likely to cut rates in April. Recession forecast for 2025.

- China: GDP forecast cut to 4.0% due to tariffs and slowing external demand. Stimulus is expected, but headwinds remain.

- Japan: Tankan survey showed mixed but positive business sentiment; BoJ may delay rate hikes due to uncertainty.

- Australia & Colombia: Both central banks held rates; RBA likely to cut in May amid tariff-related global risk.

- India: Expected to cut rates by 25 bps as inflation softens and growth eases.

- Mexico & Norway: Inflation data due next week; monetary easing is expected to begin soon in both nations.

Week Ahead (April 7–11, 2025)

Key U.S. Events:

- Economic Data:

- Tue (Apr 8): NFIB Small Business Optimism

- Thu (Apr 10): CPI, Jobless Claims, Treasury Budget

- Fri (Apr 11): PPI, Consumer Sentiment (UMich)

- Earnings:

- Fri (Apr 11): JPMorgan, Wells Fargo, Morgan Stanley, BlackRock

- Others: Levi Strauss, Delta, Constellation Brands, CarMax, WD-40

Key Global Events:

- Mexico CPI: Wednesday (Mar reading)—will shape Banxico’s next move.

- RBI Rate Decision (India): Thursday—25 bps cut expected.

- Norway CPI: Thursday—key to gauging timing of Norges Bank easing.

- Tariff Developments: Any changes or negotiations will dominate headlines and market direction.

Breaking News: Making America Great!

Meanwhile on Saturday — as traders and executives across Wall Street and corporate America were still reeling from the market mayhem — White House aides issued an announcement: Trump had won the second round of the Senior Golf Championship at his Jupiter, Florida club. – Bloomberg

Posted in Uncategorized

4 Comments

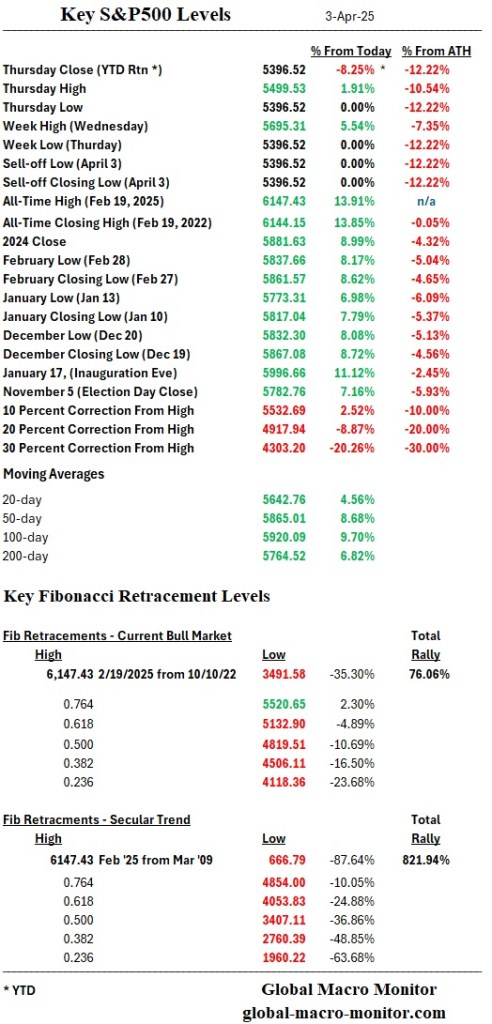

S&P500 Key Levels – April 3

The S&P 500 closed on its 5400 support level, which will not hold. The first key Fibonacci level of the current bull market, which began in October 2022, has been taken out, and the .618 at 5132.90 (4.89 percent lower) is now in play—and, at least to us, is a done deal.

This is not your normal correction, folks. The rules of the game have changed. The Fed put is off the table unless the market suffers a disruptive crash. The post-WWII global economic and political system is no more, and the clowns (except a few) running the show in Washington have zero idea what they’re doing. To paraphrase Will Rogers:

We don’t fear what they don’t know, but what they do know—that just ain’t so.

We are only buying French Dips, and we’re tightening up our seat belts.

Stay frosty, folks.

Posted in Uncategorized

Leave a comment

S&P 500 Key Levels – March 31

After a few days above, the S&P 500 has broken below its 200-day moving average, and a retest of the recent low at 5504 now appears inevitable. We are skeptical that this level will hold, with next critical support near 5400 (see chart below).

Given Friday’s ugly close and current policy overhangs, we anticipate a wave of panic selling at Monday’s open. At this point, a sharp market correction may be the only effective restraint on the Administration’s increasingly disruptive economic policies, which are being wielded like a wrecking ball against global financial and political stability.

Stay frosty, folks. Buckle up.

Posted in Uncategorized

1 Comment