From the great Jason Zweig

January 15:

1987: The New York Stock Exchange racks up daily volume of over a quarter-of-a-billion shares for the first time, as a total of 253.1 million shares are traded.

From the great Jason Zweig

1987: The New York Stock Exchange racks up daily volume of over a quarter-of-a-billion shares for the first time, as a total of 253.1 million shares are traded.

Oops, we made a mistake! Impossible Burgers are plant-based, not a lab-grown meat. Read more: https://www.engadget.com/2019/01/10/b…

Break out the Lavender crayons. Again.

Hat Tip: @RedwoodGirl

Help keep the lights on at the Global Macro Monitor. Contribute any amount based on your perception of our value added by clicking the PayPal donate widget at the right side of the screen. Thank you!

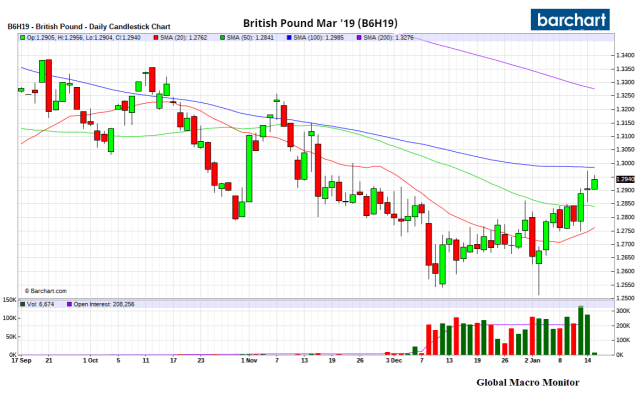

We have over $8k unrealized profit in our cable trade and expect some two-way volatility around the BREXIT vote today.

We are thus putting in an OCO (One-Cancels-The-Other) order on 5 contracts of B6H19 with a limit at 1.3050 and stop at 1.2830, just below the 50-day. If we get taken out, don’t mind buying higher.

Conversely, don’t want to turn a winner into a loser in the event traders get spooked. Not sure the market would be comfortable contemplating a potential Jeremy Corbyn government over the next few weeks.

If you missed it, we sold five S&P500 e-minis at 2582 into the close. The Doji like daily candlesticks over the past few trading sessions was our sell signal. Note Doji’s have been the closest to ringing a bell at the short-term top in this correction. It’s worth a bet, in our book.

Moving Up Stop

They are ramping ’em in the overnight session and our position is now 13 points underwater. In haste, we put in a stop in at 2602 but now moving it up to 2604. Not a good habit to move stops when a position is moving against you but we will take a waiver on this one.

Note also the stop is pretty tight (less than 1 percent) for a 19 VIX.

Retail Traders And SPY

For those who don’t trade futures or have no account, a short can be executed in the S&P ETF, SPY.

Many like to play in the inverse S&P ETFs, and some even provide double and triple leverage – such as SDS, and SPXU. Only for professionals looking for a quick levered cash trade, in our opinion, and then tread carefully as these beasts behave squirrelly and should be used only for day trades.

If you didn’t get your short off at today’s close and the overnight gains hold, consider yourself lucky for a higher entry in the morning.

Stop on the SPY short is 260.25

With just one vote left on Theresa May’s EU divorce deal, Euronews’ Raw Politics team takes at a few Brexit numbers.…

READ MORE : http://www.euronews.com/2019/01/14/br…

Our daily Doji candlestick, though not perfect but close enough for government work, was triggered at the close. The S&P rally has stalled and is having trouble cracking through 2600.

Squeezey in the overnight session with futures up 16 handles, probably, in part, due to strength in Asia stocks, especially the Hang Seng.

Though it is not wise to move stops when the market is moving against your position, we are moving our stop on the S&P e-minis up 3 points to 2604, which corresponds to a 2601-ish cash price. That is where we want to be. We stuck the 2601 stop in at the close in haste to get the trade off and the info out to you.

So, 2797.92, Thursday and the January high, on the cash is the marker to the upside. The key downside level to watch is 2573.61, the .382 Fibo retracement of the current correction is the downside support level.

Looks like we are going to get the Doji candlestick, or close to it, today, which is our sell signal and entry point. Selling 5 e-mini futures right in here at 2582. Stop at 2601. Target 2400. May add if 2573 breaks.

Retail traders should look at the S&P500 ETF, SPY. Back to you on those data points.

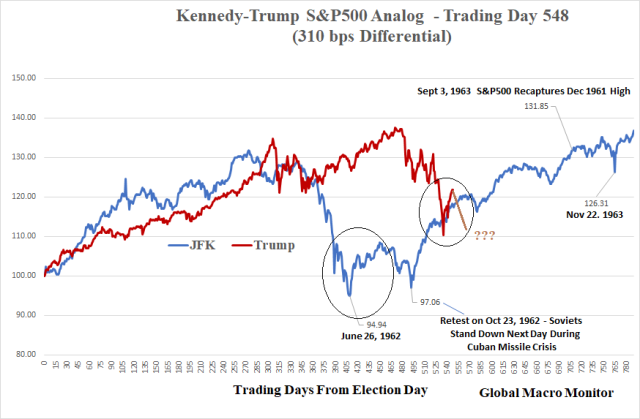

MarketWatch giving us some nice props in their excellent piece today on the back of the Zero Hedge post about our JFK-Trump S&P analog, which convinced us last February that global stocks had entered in a bear market and would soon “roll-over hard.”

Back in April, the Global Macro Monitor blog, which was the first to draw the comparison, warned in an update that, if the trend in the chart below were to continue, the S&P 500 SPX, -0.34% would soon take a big hit.

It may have taken a bit longer than expected, but the selling sure came, and the charts are now in lockstep. In fact, Wall Street has taken notice.

In a note shared on the Zero Hedge blog over the weekend, Goldman GS, +1.38% strategist David Kostin chimed in about how the current retreat, driven by policy concerns, mirrors the “Kennedy Slide” of 1962, which came against the backdrop of the Cuban Missile Crisis, when Kennedy demanded Soviet-leader Nikita Khrushchev remove nuclear-missile installations in Cuba…

Global Macro Monitor gave several reasons why the analog works, including geopolitical jitters, extreme valuations, inflation woes, etc. But the blogger pointed to one compelling stat, in particular: The S&P’s big move in a short period of time after each election: JFK — 30.1%, 285 days; Trump — 34.8%, 306 days.”

“Bear markets always follow bull markets and the bigger the prior move in a compressed time frame, the harder the fall,” he said. “Bear markets look for catalysts to sell, but the underlying vulnerability remains — valuation and longer-term overbought conditions.” — MarketWach, January 14

We iced the analog after a ten percent divergence between the two S&Ps.

We updated it today for your review.

The JFK S&P bottomed in June of 1962, rallied and then retested the low in October as bear markets often do, putting in the final bottom the day after the Russians stood down during the Cuban missile crisis.

Analogs are just another tool in the quiver to guide us through the foggy and uncertain future, just as technical analysis, market gurus, fundamental reports, and preachers, who speak with conviction, do.

Don’t bet the ranch or your life on any of the above.

Eerily, in our post, 2019’s Most Mispriced Tail Events, we list as number one: Trump won’t finish his third year in office.

1. Trump Leaves Office By Year-End

There is only one thing Trump likes more than power – money. As his legal troubles grow exponentially in 2019, the president has an epiphany that he could lose all his wealth. He cuts a Spiro Agnew-like deal and resigns from office in return for leniency. The markets rally into the announcement but Trump doesn’t go easy and dog whistles to his base as he hits the exit. The U.S. experiences a period of political and social instability. Stocks sell-off hard. – Global Macro Monitor, January 6

Stay tuned.

The real lesson is starker. It is that no business, no matter how historically innovative or powerful, is guaranteed immortality. – Robert Samuelson

QOTD = Quote of the Day