And the new market narrative by Tom Petty,

Summary

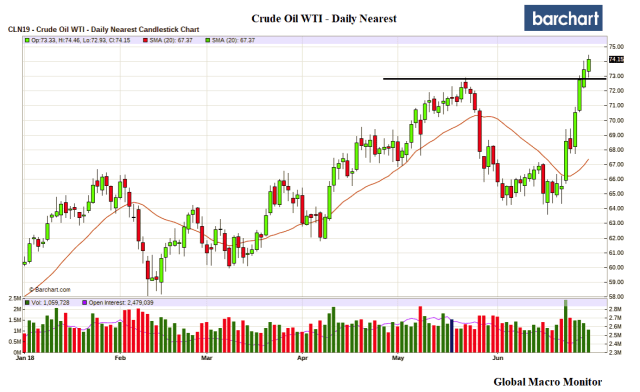

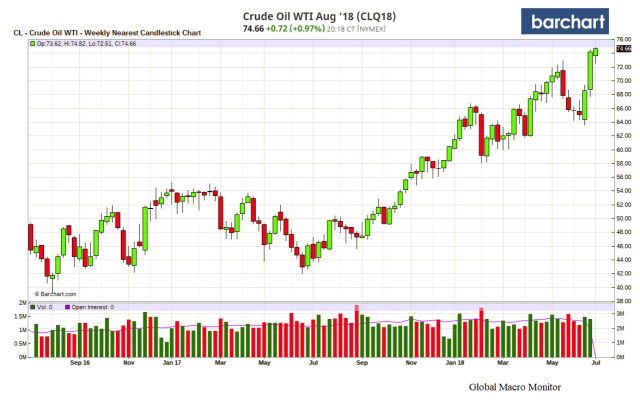

As the price of crude marches toward $80 per bbl, and drags up gas prices, the pols are starting to panic. Midterm elections and high gas prices are a toxic mix.

Surging gas prices could fuel backlash against Trump

The increase in gas prices is felt most heavily by lower-income Americans — especially in the South where people drive the most — who received the smallest share of the tax-cut benefits. So the increase could hit Trump’s blue-collar Southern base the hardest while potentially eroding confidence in the economy and tamping down consumer spending, which accounts for 70 percent of economic output. – Politico, May 25

Witness President Trump’s tweet over the weekend (completely exaggerated., in our opinion, as it would be the end of OPEC) and talk of releasing crude from the Strategic Petroleum Reserve (SPR), which would have almost zero medium-term impact on prices. Note crude oil prices rose today.

Comparative Analysis

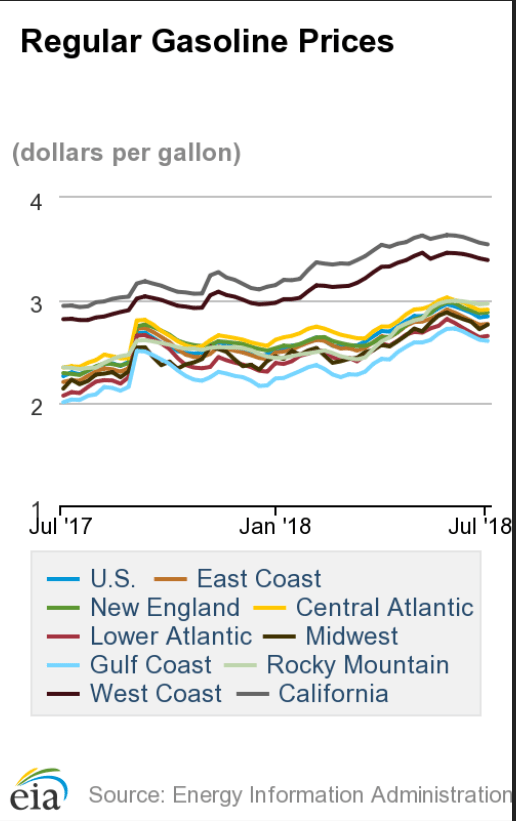

We thought it is time to roll out our comparative analytics to illustrate how the $.60 increase in gas prices over the past year will affect the average driver if prices are sustained or move higher from here.

First, a little primer on what drives gas prices.

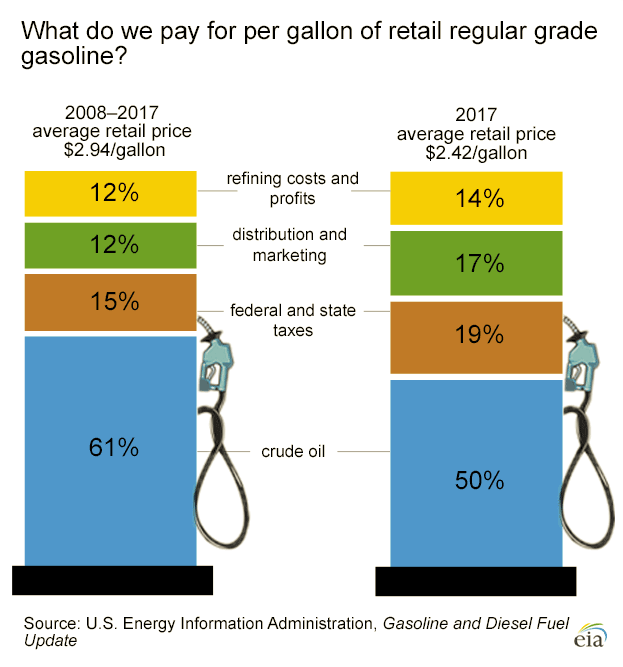

The retail price of gasoline includes four main components:

- The cost of crude oil

- Refining costs and profits

- Distribution and marketing costs and profits

- Taxes

Retail pump prices reflect these components and the profits (and sometimes losses) of refiners, marketers, distributors, and retail station owners – EIA

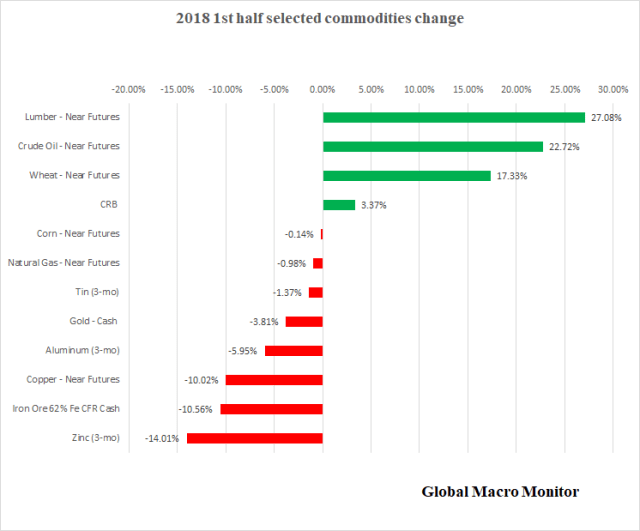

Notice in the graphic about 50 percent of the price of a gallon of gas in 2017 was derived from crude oil. Given the 23 percent rise in the price of crude since the beginning of the year, we suspect the percentage is now between 60-70 percent.

Average American Driver

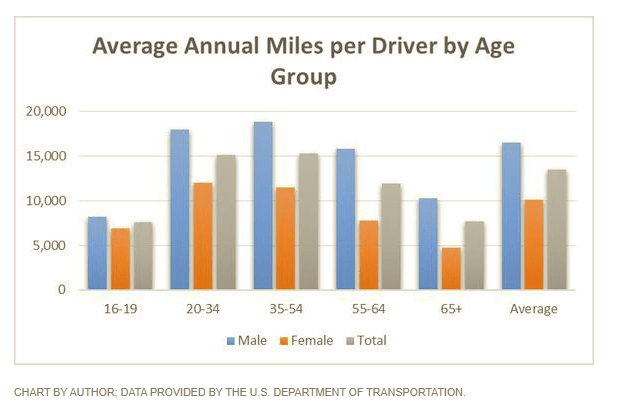

The Department of Transportation estimates the average American drives 13,474 miles per year, or about 37 miles per day. The average fuel economy for cars and light trucks now stands at about 22 mpg.

Cost Matrix

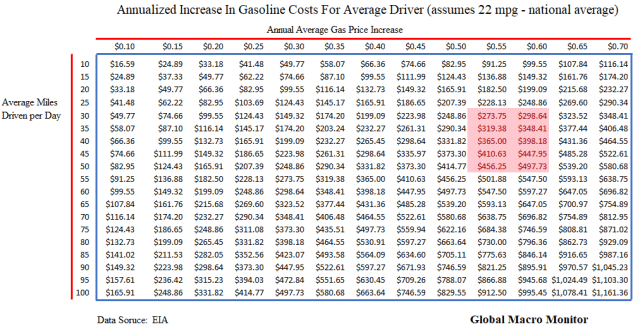

We constructed the matrix below, which calculates the average annual cost increase of various gas price changes and daily miles driven assuming the national average fuel economy of 22 mpg.

As illustrated the $.60 increase in gas prices since last year, if sustained, will cost the average driver around $400, which wipes out the tax cut for most middle class families with two drivers per household.

Play around with the matrix to calculate the increase in your annual gas bill given your miles driven. You can also make the linear transformation if your mpg differs from 22 mpg with the following:

22/(your average mpg) x Cost

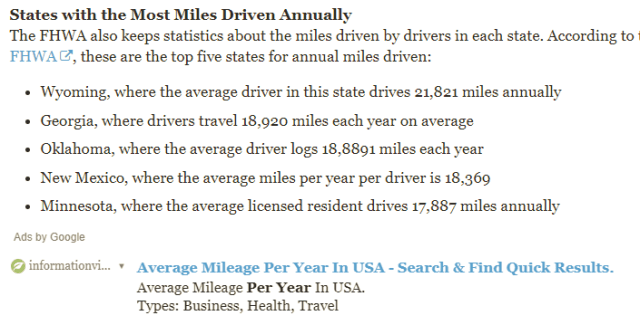

Red States Hit Hardest

We also looked at the states with the highest miles driven per year. Three out five are Red states.

The average driver in Wyoming, for example, is hit with an almost $700 increase in gas bills. We also suspect the state’s fuel economy is less than the national average of 22 mpg. That is real money for the middle class.

Expect America’s withdrawal from the Iran deal, which many believe is driving up prices, to become a major lightening rod and political liability as gas prices move higher into the November midterms.

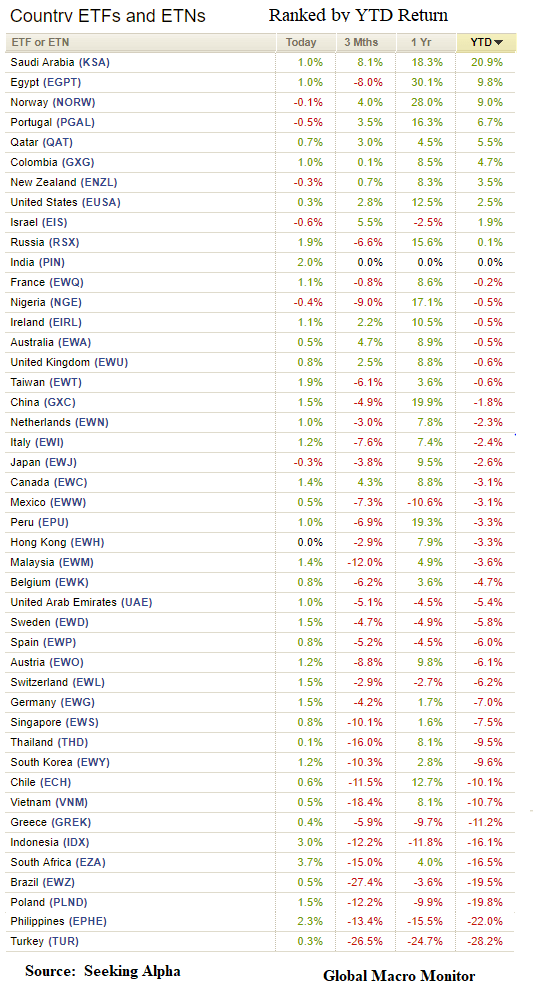

Stunning we were just talking about a Mexican presidential candidate winning a plurality of less than 30 percent just a few months ago. AMLO will enter office with a powerful mandate. If only we knew for what?

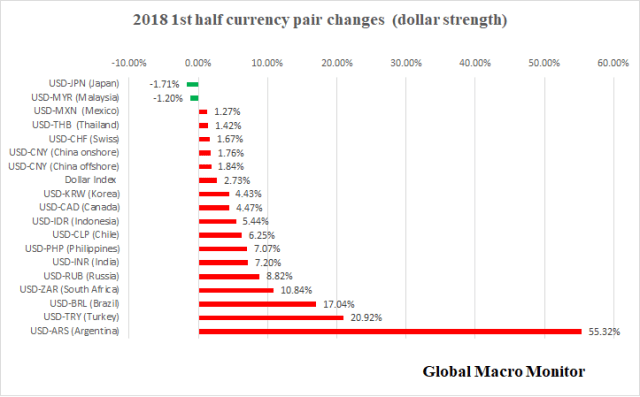

Swans relatively quiet. Mexico and Brazil currencies weaker. RMB still sliding.

Nothing happening, all glued to 2-0 Brazil v Mexico World Cup victory.

Machines push it down and buy it back. Go to the beach, read a book, get refreshed for next week.

Guess where I am going to lunch this week? I will give you the full review.

Also going to try and speak with management about capital and the marginal costs to produce a burger versus using labor. Big implications for the tipping point wage rates of burger flippers.

DEFINITELY NOT PRICED!

Horst Seehofer, the German interior minister, has set Angela Merkel an ultimatum, saying he would resign unless the chancellor acceded to his demands for tougher controls on the German border.

…That could lead to the collapse of Ms Merkel’s coalition government just three months after it came into office and throw the future of the EU’s longest-serving leader into doubt. – FT

Good luck sneaking one by that goalie!

NIZHNY NOVGOROD, Russia — Danijel Subasic saved three penalties, and Croatia’s World Cup hopes.

…Subasic is only the second goalkeeper to save three penalties in a shootout at the World Cup. The only other man to do it was Portugal keeper Ricardo against England in 2006. – Fox61

Summary

Commentary: Big events this week, though we expect quiet trading with the July 4th holiday and tomorrow’s World Cup match between Brazil and Mexico.

Our focus: 1) let’s see how crude responds to the Trump tweet; 2) how EM reacts to the election of the lefty president, AMLO in Mexico; 3) U.S. tariffs and retaliatory tariffs take effect on July 6th, and 4) most important, the Fed steps up it Quantitative Tightening cap to $40 billion per month,

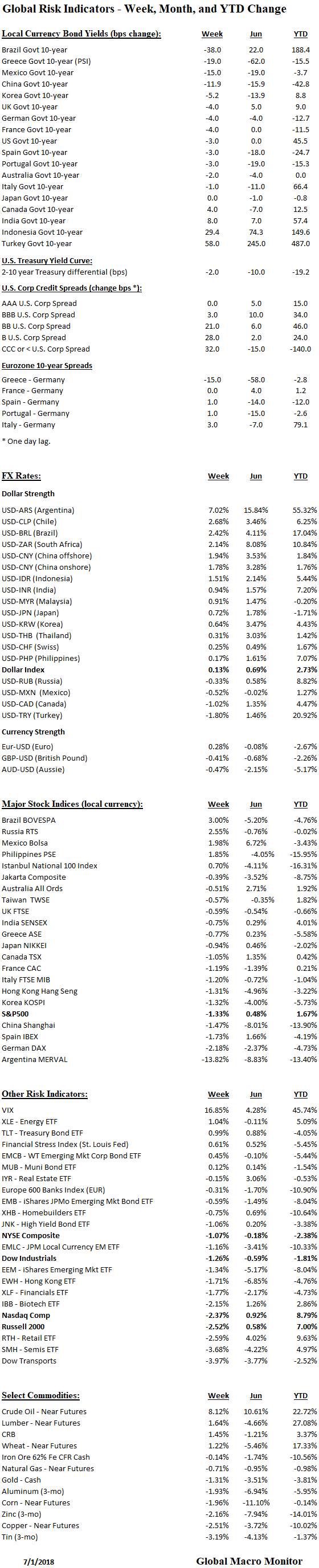

We estimate the Fed will reduce its SOMA Treasury portfolio by $24 billion and the MBS book by $11.2 billion in July. It is more challenging to estimate MBS redemptions due to the uncertainty of prepayments. We also expect the SOMA portfolio will have only $6.3 billion available to rollover into Treasury auctions in July, which are increasing in size by 13 percent per month on average y/y in 2018. Thus Fed participation in July’s Treasury auctions will be reduced to 2 percent of total new issuance, compared to 7 percent in June and 15.6 percent in May. On the margin, and all other things being equal (they never are), this should put upward pressure on interest rates, especially if traders realize and internalize the data.

Since QT began in October 2017, we estimate the Fed has reduced its holding of T-notes and bonds by $98.3 billion and the MBS book by $46.9 billion, for a total of $141 billion. The balance sheet reduction is not insignificant and equivalent to around 3.7 percent of the U.S. adjusted monetary base. We maintain this is what really matters and should be the focus of investors and not the obsession over interest rates.