Looks like our priors were correct. The tax cut is morphing into nothing more than a financial engineering game. The economics of corporations or the macro have not changed.

Random thought: We hear much about how the corporate tax cut has changed the game for profits. Isn’t this just the government jumping into the financial engineering game? Did the underlying economics of Apple really change?

That is will it increase a companies revenues? Generate new products? Will economic profits change, not just accounting profits? – GMM, March 23

After their earnings release this morning, Citibank closed 3.2 percent off its intraday high and JP Morgan was down over 4 percent from today’s high.

The tax cut has provided no big stimulus, no boost in aggregate demand. Just moving deck chairs around to increase accounting profits and make room for more stock buybacks.

Economic growth in Q1 expected to come in around Q1 around 2 percent. Punk at best.

A bigger concern for bank earnings is slow loan growth. At JPMorgan, total loans were up 4% from a year earlier but flat from the prior quarter. At Citigroup, they rose 7% from a year earlier but were up just 1% from the prior quarter.

Bank executives have generally been bullish on the recent tax reform, expecting it to boost corporate demand for loans. The chief financial officers of JPMorgan and Citigroup said Friday they haven’t yet seen much impact, but they both expect companies’ loan demand to pick up later this year. – WSJ

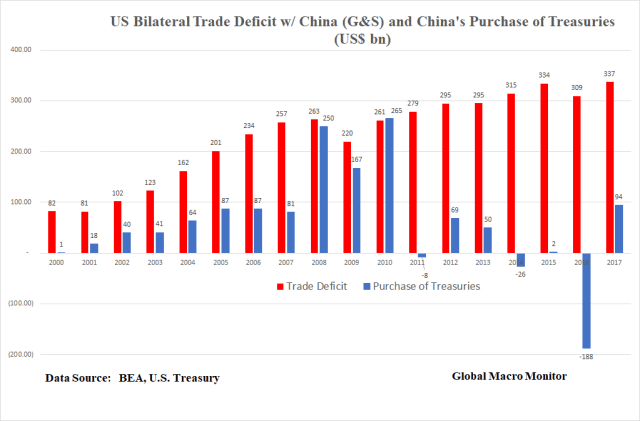

Time for a nice data dump on the U.S. bilateral trade deficit with China, its purchase of U.S. Treasury securities, China’s broad balance of payments, and the U.S. current account balance. There has been much bloviating as to what China might, will, and can’t do with its Treasury holdings so we thought its time for just the facts, ma’am.

US Bilateral Trade Deficit With China

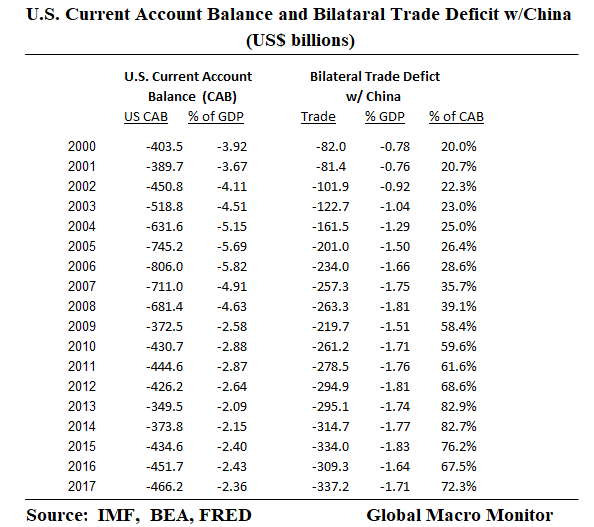

The U.S. has been running a trade deficit in goods and services with China in the amount of 1.5-1.7 percent of GDP for the past several years. Last year’s deficit totaled $337 billion.

China’s Purchase of U.S. Treasuries

China’s purchase of U.S. Treasury securities has declined significantly since the financial crisis. The country has had a problem with capital flight over the past three years, which it appears it has now arrested. During the height of capital flight in 2016, which saw the country’s international reserves fall by $1 trillion, China sold almost $200 billion in Treasuries. The alternative was to allow a significant devaluation in the renminbi, which would have been a major shock to the risk markets.

Nevertheless, China’s has recycled, on average, 30 percent of its trade balance with U.S. back into the U.S. Treasury market since 2000.

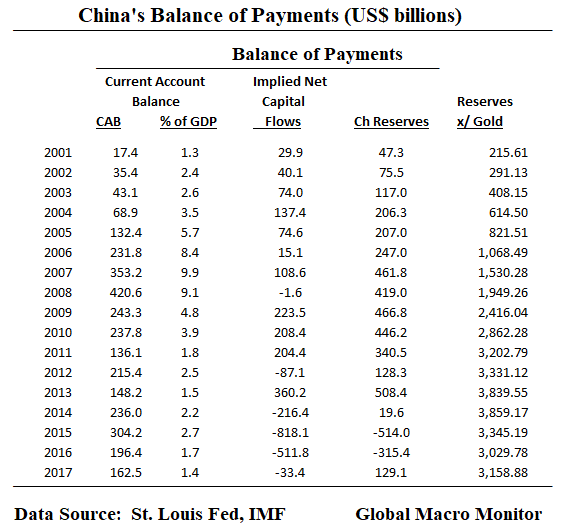

China’s Balance of Payments

Unlike Germany, China has significantly reduced its current account surplus from almost 10 percent of GDP before the financial crisis to around 1.4 percent in 2017. This is a huge external adjustment.

After running large capital account surpluses up until 2014, capital flight accelerated sharply in 2015-2016, resulting in a 25 percent decline in the country’s stock of international reserves. Though the capital account was in a small deficit in 2017, it appears the monetary authorities have arrested the decline in reserves, largely by the implementation of capital controls.

U.S. Current Account Balance

The U.S. has also experienced a significant rebalancing of its current account since the great recession. The deficit fell from -5.82 percent of GDP in 2006 to -2.36 percent last year. The adjustment has not been mirrored in the bilateral trade deficit with China.

Upshot

The data illustrates that China is not locked in to buying Treasuries with its surplus. The country can do what ever it wishes with the surplus, which includes selling down its stock of notes and bonds to defend the currency.

The Chinese monetary authorities may wish to diversify out of dollars, buy real assets, investment in the Venezuela oil sector, among many of its options rather purchasing Treasury bonds.

Most important, foreigners, probably including China, seem to be AWOL from the recent Treasury auctions, which could lead to a big problem for the risk markets down the road.

We continue to expect real yields to rise given the toxic combination of a large increase in new supply as a result of rising U.S. budget deficits, the Fed moving from largest buyer to a significant net seller, and, what appears to be, a strike by foreign buyers.

And we haven’t even discussed China’s nuclear option in the trade dispute with the U.S..

We asked foreign policy experts around the world whether we are heading for a third world war. Producer Tobias Chapple

Please subscribe HERE http://bit.ly/1rbfUog

The world’s hottest investment.

Thank you, Japan. The land of the rising Ohtani-San!

To: Larry Kudlow

From: Investor Class

Date: April 11

Re: U.S.-China Trade Dispute

_______________________________________________________________

We appreciate your positive disposition but time to get real with the markets. Don’t

lose your credibility.

Also, the Administration’s fear of losing the stock market puts the U.S. at a negotiating disadvantage. China is playing an uncooperative game with asymmetric information.

Sounds like the issue is to overcome what appears to be irreconcilable expectations.

Former CIA analyst Sue Mi Terry says the biggest risk of the upcoming summit between US President Donald Trump and North Korean leader Kim Jong Un are the ‘wildly different expectations’ from the two sides

► Subscribe to FT.com here:http://bit.ly/2GakujT