Excellent interview. Upshot? Inflation cometh.

Apr.18 — Former Chairman of the Federal Reserve Alan Greenspan joined Bloomberg Television for a wide-ranging discussion about U.S. debt, the current rate hike path, Europe’s new direction and his reading assignment for the Republicans. Dr. Greenspan joined Tom Keene on “Bloomberg Markets.”

– Bloomberg TV

Not that we discovered the similarities between the recent volatility shock and 1962 we certainly were the first to cite it and write it up. Goldie cribbed our research.

Only three times since 1950 has intraday volatility jumped so high as measured by a modified version of the Average True Range: 1) September 1955 after an extraordinarily period of calm the S&P500 tanked on September 26th when markets opened after President Eisenhower’s heart attack on the 8th hole of Cherry Hills Country Club over the weekend. The market quickly recovered; 2) January 1962 when the “Kennedy slide” began to accelerate; and 3) the October 1987 stock market crash.

Kennedy-Trump S&P500 Analog

This market is starting to look very similar to the JFK post-election rally, top, and bear market, which eventually bottomed when Khrushchev backed down during the Cuban Missile Crisis. We will post more on the JFK-Trump S&P500 analog later in the week. — GMM, February 11, 2018

Here is Zero Hedge citing the Goldie piece:

…we refer readers to an overnight report from Goldman’s new derivatives strategist Rocky Fishman (whose year-end bonus prospects now look much better), who points out that while implied vol, i.e., VIX, briefly went bananas, it was the surge in realized vol that was the real shock, at least when it comes to P&Ls.

According to Fishman, while Q1 realized volatility was not extreme in absolute terms, it was a sharp reversal from 2017 that stood out. In fact, according to Goldman’s calculations the magnitude of the surge in realized vol from Q4 2017 to Q1 2018 – which rose 3.5 times – has been observed just twice in history: “only in the Cuban Missile Crisis and the 1987 crash had quarter-over-quarter SPX realized vol tripled over the past 70 years.” – Zero Hedge, April 17, 2018

Bollocks! A citation would have been nice.

Nothing new and not out of character from the Vampire Squid.

After 363 trading days since election day, the JFK and Trump S&P500 are only 1.52 percent apart regarding price performance.

The Kennedy bull run peaked 274 trading days after the November 7, 1960, election rising 31.81 percent and topping on December 12, 1961. The Trump Bump rose 34.77 percent in 306 trading days, peaking on January 26, 2018.

The major factor why, other than the symmetric political cycle, that both markets have tracked so well is because of the similar large runs in such a short period. Speculative behavior repeats itself as human nature has not changed, even if it is machine programmed by algos that search reams of time series financial data to search for similar patterns that mimic that behavior.

As the analog illustrates it is now time for the S&P to break lower. Today (April 19), Trading Day 363, marked the swing high in 1962 and the start of the subsequent precipitous drop that took the S&P500 down 23.72 percent before bottoming on June 26, 1962.

If the analog is a true tracker — that is not daily correlated, but both move together on a relative basis in the same time and direction space — the market should break in the next few days or week.

The catalyst? Maybe higher interest rates and inflation fears.

JFK Presidential Papers of the 1962 Bear Market

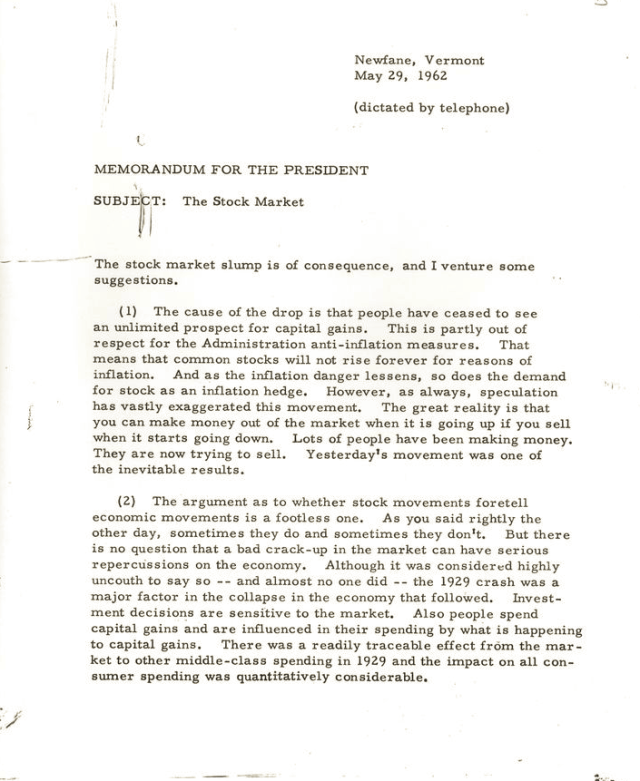

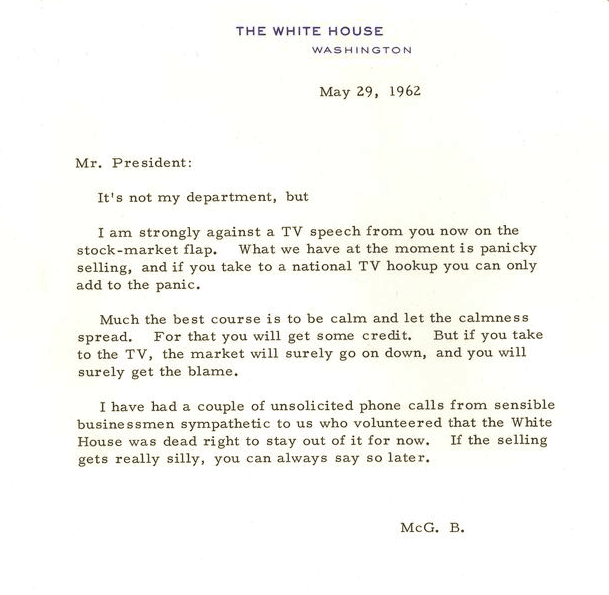

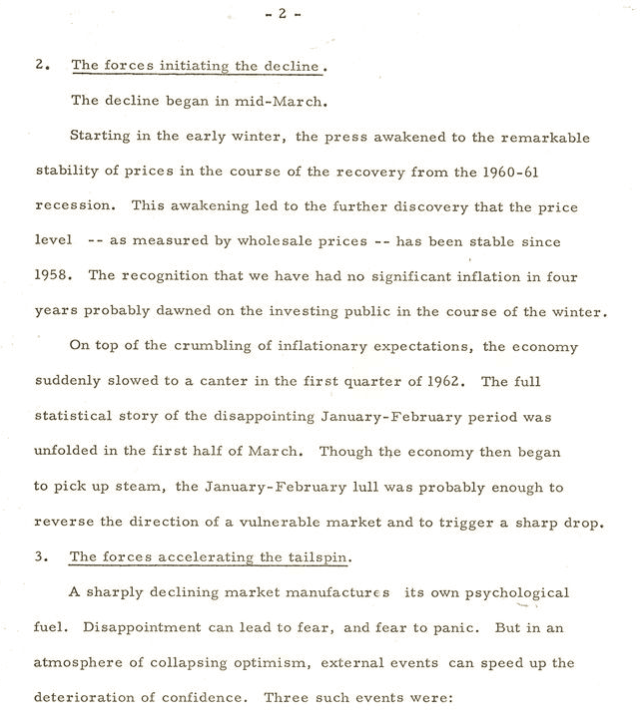

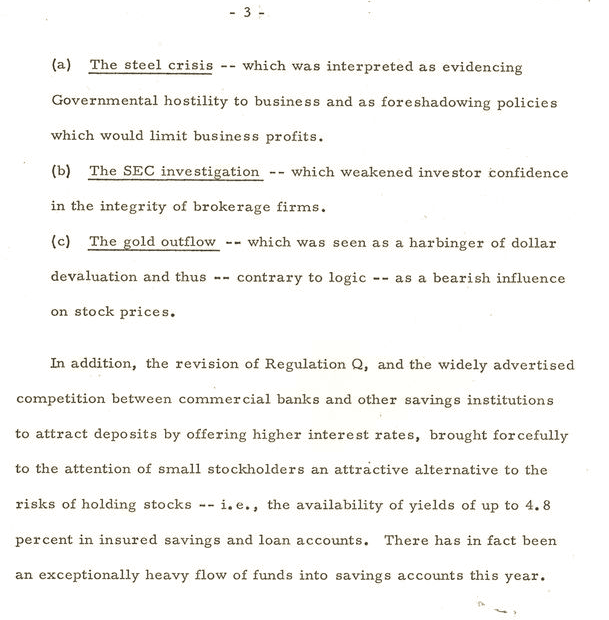

We sifted through some of President Kennedy’s briefing memos concerning the 1962 bear market, which is available online (see here). We thought you would find the following three interesting and very relevant.

The first is from JFK’s economic adviser, John Kenneth Galbraith (JKG) who lists several reasons for the bear market, mainly market psychology and the government’s anti-inflationary policies. Recall Galbraith wrote a seminal book on the 1929 market crash.

The second from McGeorge Bundy, Special Assistant to the President for National Security, urging the President not to panic after the 6.68 percent flash crash on May 28, 1962. The market decline did not warrant the White House’s attention until the May flash crash.

Finally, the third memo is the last three pages of a briefing to the President from Walter Heller‘s Council of Economic Advisers (CEA) listing several macro reasons for the market slump, including steel prices, balance of payments deficit ergo tighter money, and competition from rising short-term rates. All seem similar to the current macro issues affecting the market.

Time to buckle up.

Thought tax cuts were going to lead us to the new economic Shangri-La?

Random thought: We hear much about how the corporate tax cut has changed the game for profits. Isn’t this just the government jumping into the financial engineering game? Did the underlying economics of Apple really change?

…Apple needs more than just a tax cut and financial engineering. Maybe a new product, or two? – GMM

Financial engineering is nearing its end-game.

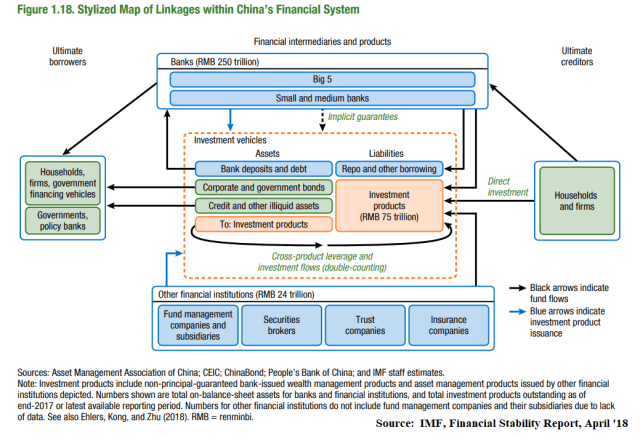

Awesome chart on the opaque China’s Financial System from the IMF’s latest Global Financial Stability Report. China has been a hedge fund graveyard as short positions on the country have moved sideways if not against the perps. .

The country spent over $1 trillion in reserves defending its currency over the past few years and now seems to have arrested capital flight. Pressure is building on the Hong Kong dollar, but we would not bet against it. At least not until it or if it breaks.

China is, after fall, still a command economy. The government can intervene whenever and with whatever policy it desires to protect and further the Party’s economic and political goals. Market discipline is not an issue in China if it threatens the government and political stability.

The U.S. Savings and Loans Crisis

For example, think of how bank deposit insurance subverts market discipline in the U.S. financial system. Though necessary to avert bank runs, financial institutions can remain in business with government deposit guarantees even with Frankensteinesque balance sheets.

GAO Report

As a graduate student, I worked at the General Accounting Office (GAO), the research arm of the U.S. Congress. I spent most of my time doing econometrics for a piece commissioned by a congressman who wanted to know what it would cost the government to resolve the 1980’s Savings and Loans crisis.

We estimated the cost of an immediate resolution of around $22 billion to close all the bankrupt S&Ls that were still able to operate due to the deposit guarantee (FSLIC). These thrifts were highly unprofitable as they paid higher deposit rates to attract funds and made riskier loans trying to hit the home runs or bet the ranch to “get them back to even.”

If they were allowed to continue in business – that is, if the government chose forebearence – we concluded it would eventually cost the taxpayer over $200 billion.

Because President Reagan wanted to avoid a further increase in record budget deficits, the Administration chose forbearance. At the end of the day more than half of the S&Ls failed costing Poppy Bush and the taxpayer more $200 billion. Some reports put the final cost closer to $500 billion.

Our report is still widely cited today.

Moral Hazard

The moral hazard of government guarantees can avert bank runs and market discipline but with a cost. A balance must be struck.

The one thing that is still etched in my mind after running thousands of statistical iterations during that paper are the many S&Ls that had a negative net worth or equity of more than 60 percent of total assets.

Can you imagine having your savings in such a deeply bankrupt institution? It did not matter with deposit guarantees, however. Moreover, you were earning 25-100 bps higher interest on what was effeectively U.S. Treasury risk. Not one penny of guaranteed deposits was lost.

China

China is moral hazard times a million. The system can remain afloat much longer than expected. China will do whatever it takes to survive.

We have been intermittent China macro bears over the past several years but, thank goodness, we never had the ‘nads to bet against the country.

Upshot

At the end of the day, it is clear to us governments will do whatever it takes to keep a sinking ship afloat. If it means printing $15 trillion in fiat currency, so be it. I never thought we would see this day, but it is what it is.

Our conclusion is the endgame will be inflation but probably not before several major deflation scares.

Argentina nationalized and directly monetized public pension short falls and debt payments. Don’t you think the U.S. and other governments will do the same or will politicians have the courage to restructure the promises they have made? Easy answer given recent history.

We bet Argentina over 1930’s America. Sorry defaltionistas.

The large-scale and opaque interconnections of the Chinese financial system continue to pose stability risks (Figure 1.18). China’s RMB 250 trillion (300 percent of GDP) banking system is tightly linked to the shadow banking sector through its exposure to off-balance-sheet investment vehicles. These vehicles are largely funded through the issuance of investment products (RMB 75 trillion), with roughly half sold to multiple investors as high-yielding alternatives to bank deposits and half held by single investors, including banks.47 They invest in various assets, such as bonds, bank deposits, and nonstandard credit assets, as well as in other investment products. Insurance companies also have considerable exposure to these vehicles because they invest in their products and use them as a source of funding. These little-regulated vehicles have played a critical role in facilitating China’s historic credit boom and have helped create a complex web of exposure between financial institutions.

Banks are exposed to investment vehicles along many dimensions—as investors, creditors, borrowers, guarantors, and managers. These vehicles rely on banks’ short-term financing to use leverage and manage their maturity mismatches. Banks, in turn, receive significant flows from these vehicles in the form of deposits and bond investments. Banks and other financial institutions are also direct investors in investment products. Small and medium-sized banking institutions and insurance companies are particularly exposed, with investment products accounting for one-fifth and one-third of their assets, respectively. About one-quarter of investment vehicle assets, in turn, are invested in other vehicles, leading to opaque cross-holding and leverage structures that are difficult for regulators and investors to monitor. Banks in particular are seen as implicitly guaranteeing the RMB 25 trillion in investment products they manage, which allows them to package high-risk credit investments as low-risk retail savings products. Investment vehicles managed by nonbank financial institutions are perceived to be higher risk, but in most cases banks still bear some risk as creditor, end investor, or guarantor.

The authorities have substantially tightened the regulatory framework to reduce risks related to investment vehicles and other borrowing between financial institutions. Since the summer of 2016, regulators have incorporated bank-sponsored investment vehicles in the macroprudential framework and have taken other steps to curb financial sector leverage and interconnectedness.48 Proposed asset management rules would also overhaul the investment product market beginning in 2018. In addition to limits on investment vehicle leverage and complexity, banks would be gradually restricted from investing in these vehicles or providing them with financial support. This restriction would limit their ability to implicitly guarantee investment products’ fixed-yield returns, effectively converting roughly half of the market from deposit-like products into mutual funds. In addition, the insurance regulator has clamped down on the sale of short-term investment products by life insurers. – IMF, Financial Stability Report

Hat Tip: Grace E., The Gorgeous Ginger From Maria Carillo

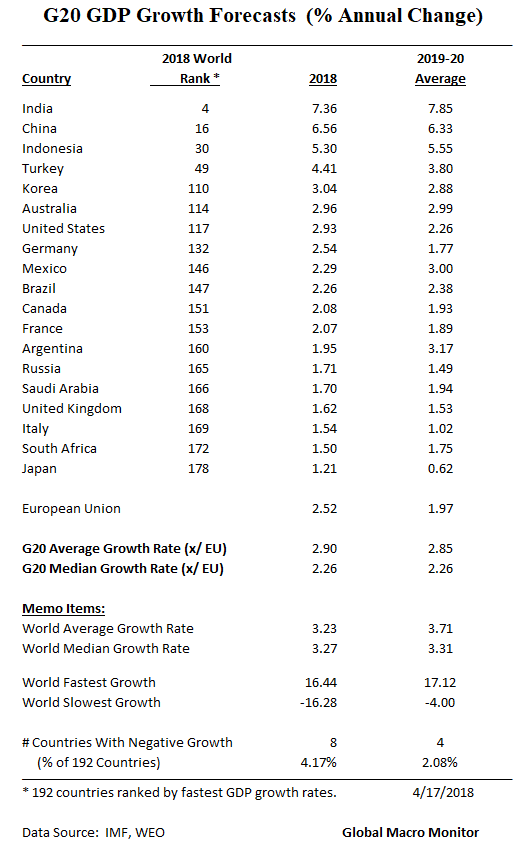

Hot of the press!

We have updated the latest 2018 and 2019-20 average annual forecasts and ranked the world’s country 2018 GDP forecasts in our ginormous table below. The data are from today’s release of the April 2018 IMF’s World Economic Outlook.

Let’s begin by first checking out the G20 data.

President Reagan On The ’87 Stock Market Crash

President Reagan certainly understood the nature of markets.

That is they do whatever they are going to do, sometimes without a fundamental rhyme or reason. Very different from the current occupant of the White House who seems to think every uptick in the S&P is all about him, and he is not afraid to take credit for the upside and tweet about it.

Before going to President Reagan’s comments about the October 19, 1987 stock market crash, we first review some data, which lends light on the 1987 crash.

The S&P500 had just completed a massive run from September 1985 before peaking on August 25, 1987, moving up almost 87 percent in less than two years. That qualifies as a bubble in our view.

Yuuuge Decline In Interest Rates

Much of the move was attributed to a sharp drop in interest rates.

The 10-year Treasury yield fell almost 350 bps in less than a year before making a local bottom in September 1986. Interest rates then began to move sharply higher, utterly roundtripping almost the entire move by the day of the crash.

The 10-year yield had risen 300 bps year-to-date on October 16th, closing back above 10 percent, increasing almost 150 bps just since the S&P peaked on August 25th.

The S&P500 was already down 16.33 percent from its high before crashing on October 19th. Markets rarely fall out of the sky and usually signal something big is coming by a sharp rise in volatility. Think of a Richter scale before a volcano blows.

This is why we take the early February volatility shock seriously and a signal of regime change, and give a much higher probability for a potential major price reversal than most in the market are anticipating.

Finally, the S&P500 fell 23.43 percent from the October 16th Friday close to the intraday low on Tuesday before a mysterious buyer stepped into to the Major Market Index futures contract at 12:38 p.m, setting the stage for one of the most powerful rallies in history.

We believe the 1987 stock market crash was an accident waiting to happen due mainly to a toxic cocktail of a severely overbought market and rising interest rates. All that was needed was a buyers strike coupled with some catalysts or reasons to bail and take profits. The same reasons may or may not have mattered if not for such a toxic cocktail.

Given the nature of the New Economy, we seriously doubt the government will allow such a similar short-term crash, say, 15-25 percent, to occur again. We now have no doubt the Fed will step up and announce they will do whatever it takes and become the buyer of last resort to keep the market from melting down in one or two days.

Why? Because it would be the end of the world and they surely know it.

The thought of the Fed directly purchasing stocks as the Bank of Japan now does contradicts everything Larry Kudlow’s dictum, “free market capitalism is the best path to prosperity” stands for.

Privatizing profits and socializing major Wall Street losses are now forever institutionalized especially given the structure of our asset driven global economy. The “Powell put” may now have a little lower strike price than many traders would like but it is absolutely still in place. No doubt about it.

Oy veh! Sorry deflationistas.

Iran Again

By the way, the U.S. was also in the midst of a conflict with Iran in October 1987.

President Reagan’s Comments

Now to President Reagan.

Asked after the close if the stock market crash was his fault, the President delivers the ultimate money quote, in our book:

Profound. We can learn from the Gipper to refrain from trying to explain or attribute daily stock market moves to certain factors. Any one of the catalysts we deem moved the market in a certain direction on a given day could have moved it 180 degrees the other way with a different set of technical conditions.

Reagan truly understood market noise.

Full Transcript Of October 19, 1987 Informal Exchange With The Press

Here is the full transcript with reporters that day, October 19, 1987.