Hong Kong’s floor traders will vacate the city’s trading hall for the final time on Friday after the exchange operator shuts the premises permanently. Don Weinland reports.

► Subscribe to FT.com here: http://bit.ly/2r8RJzM

Picture of our old street after firestorm. Every house on street wiped out. Fate of our new home dependent on direction of wind and how hard it blows over next few days.

Caught up in NorCal fires and had to evacuate home.

Looks like war zone. Several neighborhoods burnt to ground with gas flaring off like the Kuwaiti desert in Gulf War I.

Back to you soon as we can.

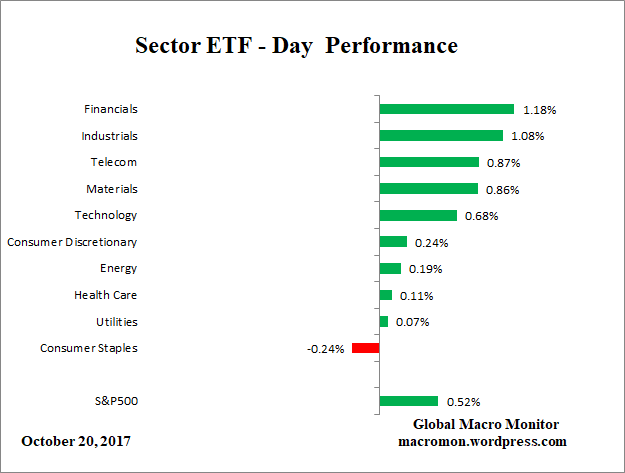

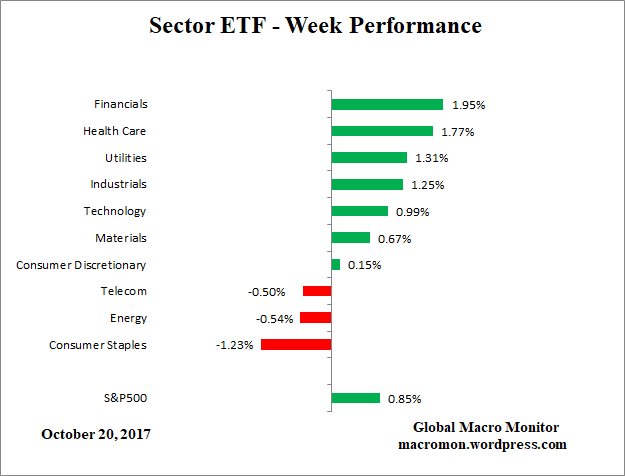

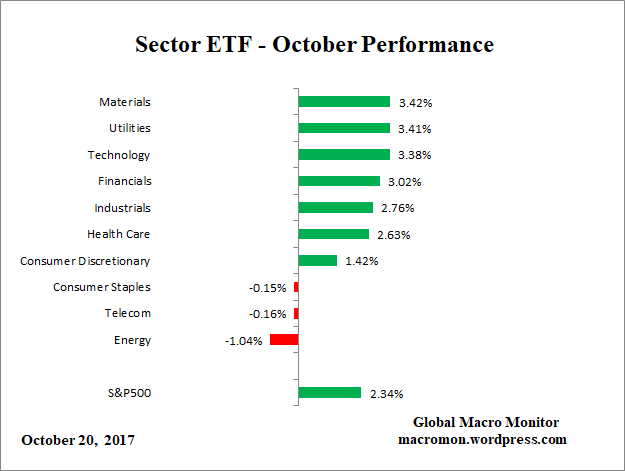

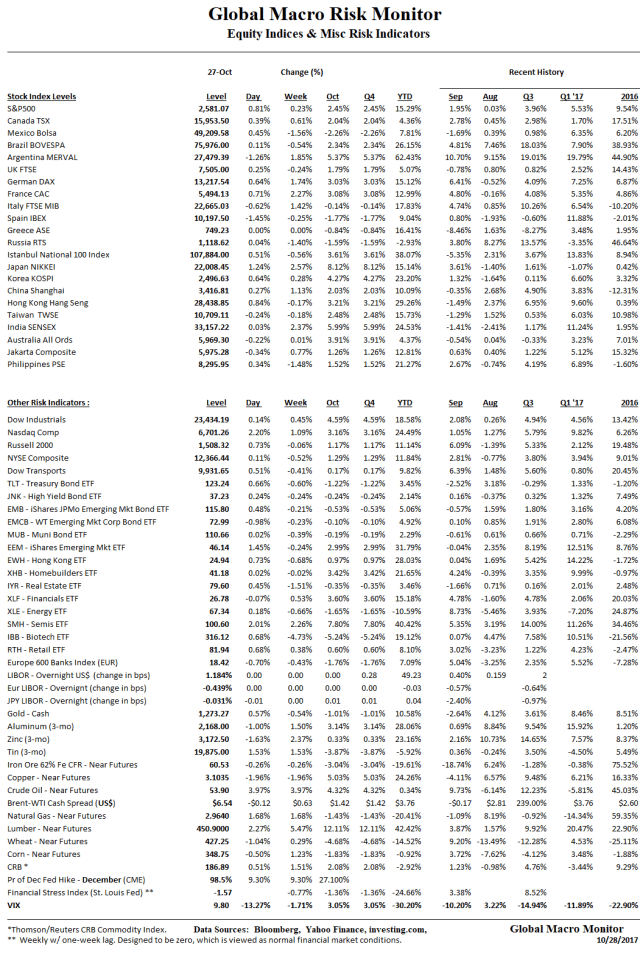

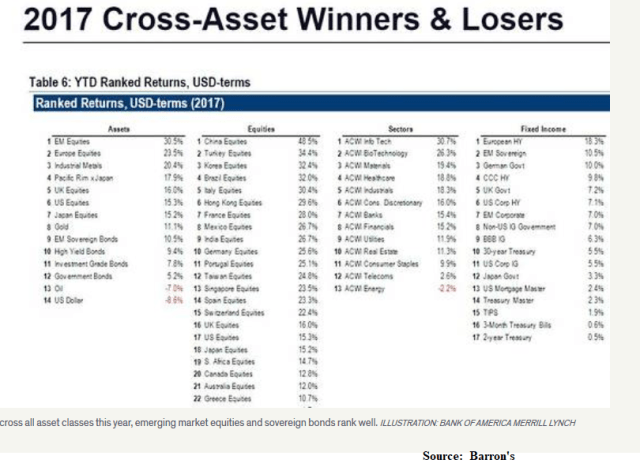

The global stock bull market continues like a full force gale with the emerging markets leading the way. The grand narrative of the market is the synchronized global recovery and the hope for U.S. tax cuts.

The counter-narrative? Valuations and, now, rising bond yields.

Relatively quiet week in fixed income.

U.S. 10-year yield is having trouble breaking 2.40 percent with 2.45 percent, a key level of resistance. German bund yields are meeting stiff resistance at 0.50 percent. Watch 0.62 percent on the Bund.

Mexico yields up on budgetary concerns – more spending due to the earthquake. Spain higher on Catalonia concerns and Turkey rates up on inflationary pressures and geopolitical spat with U.S..

Ireland was paid to borrow money with a new issue this week. Un-freaking-believable:

Ireland has sold its first ever bond with a coupon of zero per cent, with the country effectively being paid to borrow €4bn over five years. The country brought in more than €10bn of orders for the debt, which matures in 2022. The bond, which is priced slightly above par, came at a yield of minus 0.008 per cent. The absence of the coupon means Ireland will not have to make any interest payments on the bond, which will mature at a slightly lower value than that at which it was sold. Investors who hold the debt to maturity are guaranteed to lose money. – FT

High-grade corporate spreads in on fears of expected lower supply due to the elimination of interest tax deduction and less need for liquidity as corporate capital repatriated from overseas post U.S. tax reform.

We still expect a taper tantrum in Europe this month, which is why 0.62 percent on the Bund, the 52-week high, is important. A breakout above the key level would signal the tantrum is on.

Dollar stronger across the board as expectations of a December Fed hike increased, now close to 90 percent probability. South Africa hit hardest.

The British pound had its worst week in a year. Speculation abounds that the Tory MPs are preparing to dump the prime minister.

The Industrial metals were up on strong global economic growth. Crude tanked on supply fears caused by OPEC backsliding.

Biotechs continue to rip and U.S. financials doing better on prospects for higher interest rates. Euro banks pulled down by Spanish banks and concerns over Catalonia.

Watching bank earnings later in the week to see if loan books are expanding. If the case, inflationary expectations should increase especially after the Republicans have abandoned their budget-cutting ways.

IMF out with World Economic Outlook on Tuesday. Federal Reserve minutes on Wednesday. Eurozone industrial production on Thursday will be crucial to ECB forward guidance. Retail sales and CPI in U.S. on Friday.

Monitoring Catalonia, which is keeping a lid on interest rates in the ‘zone. Still expecting a revolt by bond markets leading to an October correction in risk markets. The fact that a correction seems so improbable only strengthens our conviction it is more likely.

Buy the correction, however, as interest rates are not even close to the level that will send yield chasers into retreat.

Upshot? Higher interest rates and stronger dollar on the way, which should cause a bit of temporary risk aversion.

Active central bank Narrative construction in the service of their policy goals is a permanent change in our market dynamics. – Ben Hunt, Epsilon Theory