Getting back to the pre-COVID unemployment rate of 3.5 percent after the rules of the game and economic incentives have changed is a pipe dream, in our view.

It’s clear the labor supply curve has shifted left.

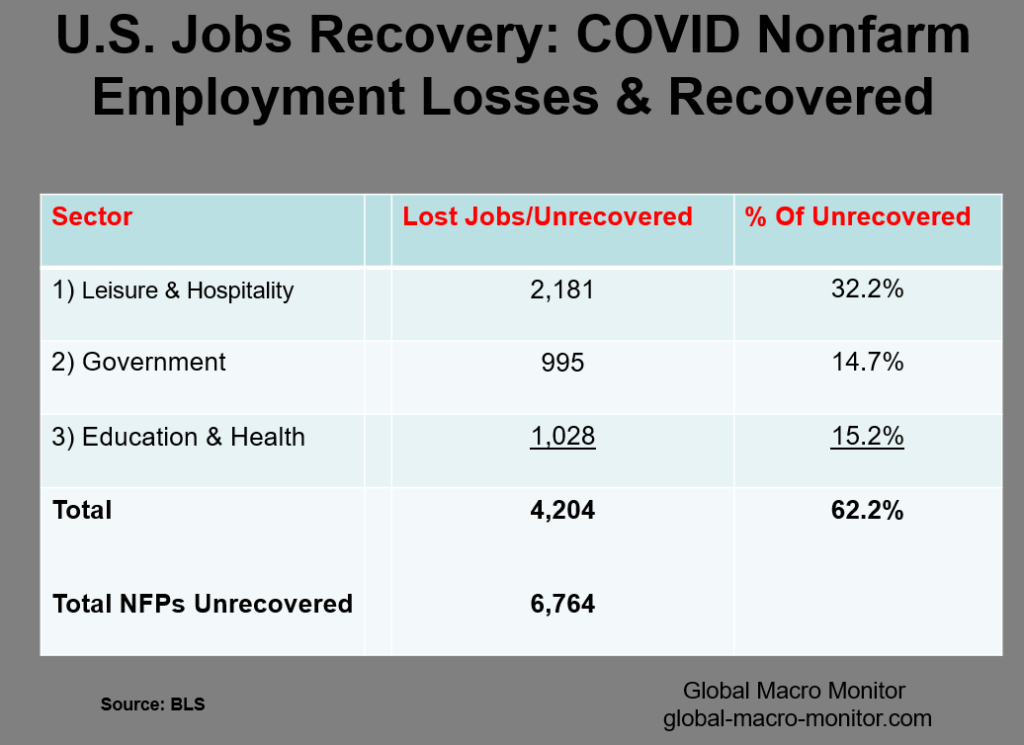

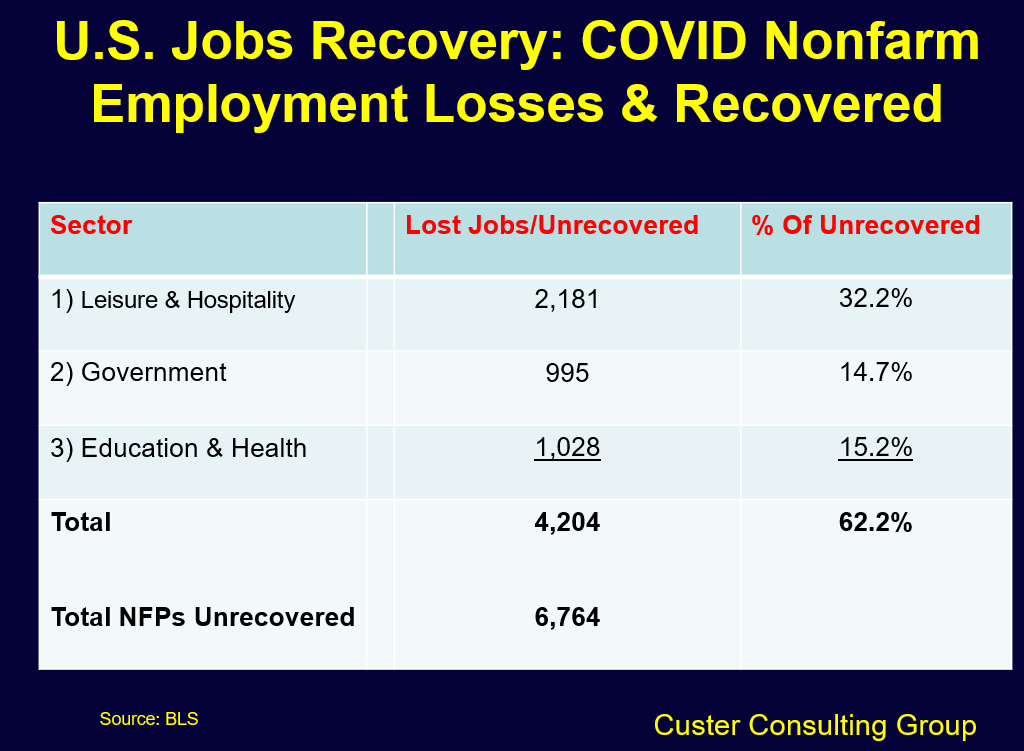

Isn’t that evident with 32.2 percent of the unrecovered jobs in the leisure and hospitality sector yet no workers can be found? Moreover, 62.2 percent of unrecovered jobs are in three sectors: leisure and hospitality, government, and education and healthcare. None lack for demand.

Next month will be a test for the labor market as the extraordinary COVID unemployment benefits roll off. Will the government allow them to fade, however?

Demand ain’t the problem, folks.

Maybe higher wages will attract more workers, which we are always rooting for but higher real incomes are only sustainable with productivity gains and/or changes in relative prices with respect to each sector.

Trying to monetize a supply shock only exasperates the problem. Ask the global supply chain, where almost hyperinflationary expectations rule the day.

Nevertheless, kudos to the policymakers for keeping the global economy out of recession but a big fail for maintaining the extraordinary policy measures way beyond their useful life, which are now becoming deleterious to producers.

Price pressures remained intense during July, with rates of both input cost and output charge inflation among the steepest in the survey history. Part of the increase in input prices reflected the ongoing disruption across global supply chains. Increased costs were passed on to clients in the form of higher charges. Rates of increase in both price measures were steeper at manufacturers than service providers. – Global Composite PMI, July 2021

We are so incredibly happy to report Carol K. is doing much better and has made it to the other side of her major medical procedure. Thanks for all your help but let’s not get complacent. Keep those prayers, thoughts, all of the above, and all other coming her way, folks. A full report up soon. #CKStrong

Just to be safe, let’s qualify the post title,

…as Tolkien once said, ‘Not all those who wander are lost,’ so too ‘not all Floridians are stupid’ but that gov’ner...

Totally lost patience with the unvaxed and their lame excuses.

CK is still in the fight of her life. Again, we ask that everybody, everywhere please bring all and whatever you got in the form of prayers, thoughts, positive energy, manifestations, visualizations, anything and everything with powerful intensity her way.

We have been working on this post for some time and want to get it out before the data are too stale. We will break it up into three or four pieces because our analysis of the Treasury market usually results in exceptionally long reads. One reader wrote about our last big research piece on the T market:

This post is so big you can see it from outer space!

We also do not want to bury the lead.

Longer-term Treasury yields are so distorted by central bank buying they are now and have been for years worthless in providing any sound economic signal.

Nothing new here, but we provide you with some good fresh data.

An Ugly Feedback Loop

We have speculated in many posts over the years about the “what if.” That is, what if the Treasury market began to rally purely on technical reasons, yields fall dramatically, and other markets take their cue and act accordingly. You know, kind of like the past week, when equities sold off big on Monday.

The fake yields give a false signal that something nasty is coming; other markets close ranks, and “the bond market distortion yield” kicks the economy into a deep global recession.

Another scenario: What if policymakers base their decision on the distorted yields or “break evens?” The data below show the Fed has bought up the equivalent of almost 200 percent all new TIP issuance during the pandemic.

COVID Budget Deficit

Let’s first answer how bond yields can be so low if the government just ran up such a massive debt from the COVID crisis?

Those are humungo deficits — albeit mostly “transitory” — even by 1980’s Latin America standards, and they do not include large interest payment expenditures, as many of those countries experienced during their high inflation days.

To evaluate the government’s fiscal situation, analysts typically reference the total deficit — the gap between total federal spending and revenues. However, another measurement — the primary deficit — focuses on the difference between government revenues and spending, excluding interest payments. By excluding debt service, the primary deficit highlights the underlying structural imbalance between the amount of money that the federal government brings in each year (mostly through taxes) and how much it costs to provide government goods and services. – Peterson Foundation

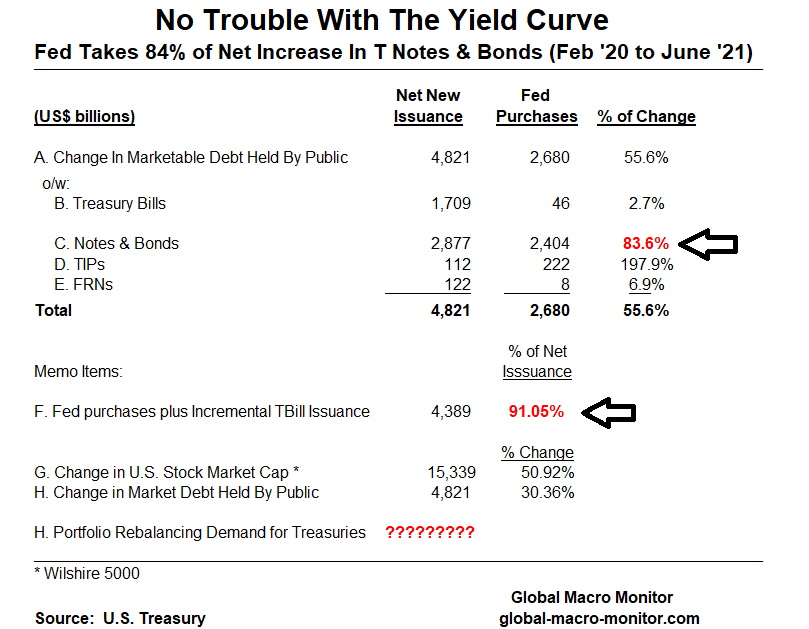

Change In Marketable Debt Held By The Public

So how could the government float another $4.8 trillion of debt in the market without significantly spiking interest rates? Is the bid for U.S. government debt that strong?

No.

In fact, one of our most prophetable (yes, spelling is correct) posts came in early March 2020, warning there was no way the government could finance what we expected to be huge deficits to support the economy during COVID.

We seriously doubt it and the Fed is going to have to step-up big time with QE, non-QE, or let’s just call it for what it is, monetization. – GMM, March 8, 2020

Take a look and stare a bit at the following table.

That data show the U.S. G increased its stock of marketable debt held by the public by $4.8 trillion from the end of February 2020 through June 2021. Treasury Bill issuance increased by $1.7 trillion, something that many analysts miss when they make statements, such as

“the Fed has financed 50 percent of the COVID deficit.”

True statement but dig deeper.

Fed Purchases

The Fed purchased a total of $2.7 trillion of Treasury securities during the period, of which 90 percent went to the purchase of Treasury notes and bonds. Thus, the Fed COVID purchases amounted to almost 84 percent of all new note and bond issuance by the U.S. government, putting relatively little pressure on the yield curve.

Add the $1.7 trillion of net new issuance of T Bills, with the stock increasing from $2.6 trillion (15.2 percent of marketable debt) in February 2020 to $4.3 (19.7 percent) and that takes care of over 90 percent of the deficit. Easy money, no pressure on the yield curve.

Also note the Fed’s purchase of almost 200 percent of the TIP issuance during the period, which, no doubt was to manage the “breakeven rates.” The U.S. central bank now owns 22 percent of the TIPs market.

Once down the monetization rabbit hole, more dikes have to be plugged.

Rebalancing

The $473 billion difference between the new issuance of notes and bonds and Fed purchases during the period could have easily been absorbed and then some by just the rebalancing effect alone. The U.S. stock capitalization increased $15 trillion during the period bloating the equity allocation in many portfolios and forcing a reallocation to fixed-income, some of which to the Treasury market. No price sensitivity, auto pilot buying. No signal, bad noise.

Upshot

Now you can LOL, well, at least smile, next time you hear,

What is the bond market telling us?

We will concede that though yield levels are meaningless and should be much higher, direction may, at times, provide some some useful information.

Coming up in the next chapters of this post, we will look at the changing ownership of the Treasury market, the timing of how Treasury financed its COVID deficit, how foreign central banks are reducing their allocation to Treasuries, and how central banks — the Fed and foreign — own almost 60-70 percent of all Treasury notes and bonds with a maturity longer than seven years. Stunning.

Our Carol K. is entering a critical phase in her health battle. Everybody, everywhere please bring all and whatever you got in the form of prayers, thoughts, positive energy, manifestations, visualizations, anything and everything with powerful intensity her way.

Our Carol K. starts her new procedure tomorrow to fight off her AML. Come on, world, let’s will her to heath! You go, girl!

Check out the “spectacular” (ht/ CK) roundtrip in the price of lumber this year. After rising over 160 percent from January to May, Timber!

The commodity has fallen 70 percent and is now below its breakout price.

The pulp flop has brought out those preaching the the “D” word and point to lumber as a sign of deflation. O.M.G.!

Me thinks the price action reflects what I used to tell my young traders, who couldn’t resist chasing prices to the moon.

“Trees don’t grow to the sky,” an old German proverb translated from “Bäume wachsen nicht in den Himmel, which suggests there are fundamental and valuation limits on how high asset and commodity prices can go.

Given the speculative zeitgeist that has hijacked global society, lumber’s microstructure and it’s industry idiosyncrasies made it a good story for speculators to run it up, and run it up they did.

You know, the inelastic supply curve thingy, the lead time to get lumber to the market is long, like it takes 200 years to grow a Redwood tree, blah, blah.

Blood Clotting In Speculative Assets

Spec assets are like blood, folks, if they stop flowing (from lower left to upper right), they tend to clot, and many times kill the patient.

Something I tried explain to my buddy’s 16-year old son a few months ago when Doggie Coin was trading north of $.50 (now 60 percent lower). I quickly experienced a big beat down and he lectured me, “What do you know about the space?”

This kid knew nothing, and could care less about the story of crypto currencies: going to replace the dollar and the medium of exchange, scarcity value, etc. He was sucked in simply because the price was moving higher. Stories, themes, and memes are great fodder for the financial media to explain price action but not to sustain prices.

We suspect many others are about to learn about the “speculative space” once monetary policy reverses, if it ever does or can.

Our beloved Carol K. starts a new risky treatment this week to try and conquer her serious illness. Everyone at GMM and all of our readers are with you, girlfriend!

Can’t wait to hear the Chairman justify zero rate policy and deficit monetization with inflation roaring at > 5 percent. It would be entertaining, if it weren’t so damaging.

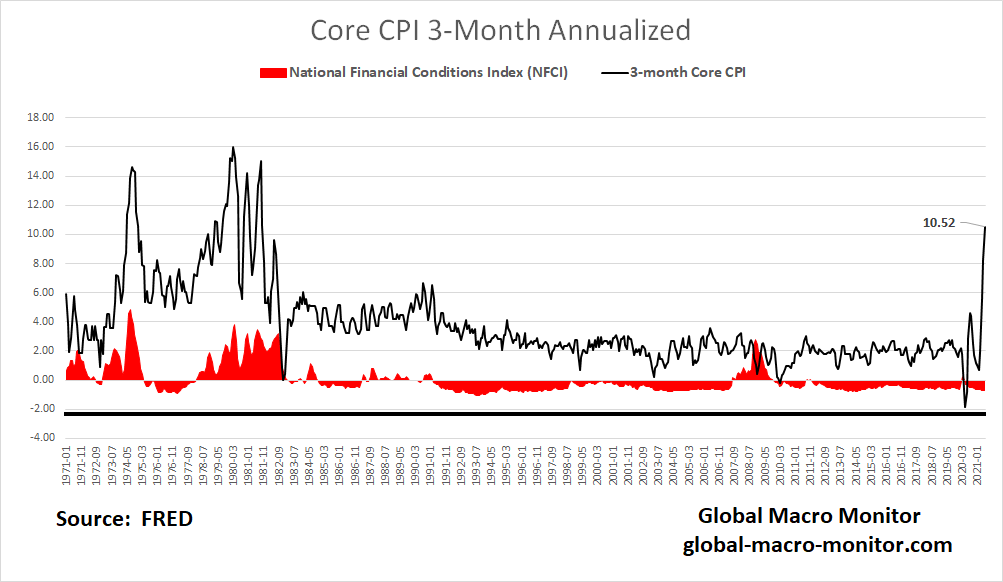

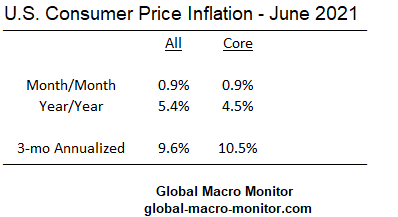

The past three months of core CPI inflation prints have been big, big, big — 0.9, 0.7, and 0.9 percent, respectively. There is zero “base effect” on these data, folks.

If annualized, as the GDP prints are, the economy hasn’t seen this type of three-month core inflation since 1981.

Sure, some have to do with the reopening, and some not.

Our priors are policymakers have distorted too many markets, over-stimulated the economy, and pumped too much high-powered money into the global economy. China rejoined the party last night.

My Lobster Roll Restaurant

We keep waiting for a new Lobster Roll (rare in Wine Country) restaurant to open up on my street, for example, and it’s taking forever. I spoke to the owner yesterday, who said he couldn’t find workers.

What the Fed believes is a demand problem to recover all the jobs lost to COVID is, in reality, a supply problem. Put the academic models down and go talk with the small businesses.

We maintain there is a shortage of labor at the given wage rates for much of the leisure and hospitality sector, which makes up about 12 percent of nonfarm payrolls yet 32 percent of unrecovered lost jobs lost to COVID. The jobs aren’t returning for lack of demand, mitigated by easy monetary policy. Still, most of the lost jobs are in three sectors, where we suspect will have to pay higher wages and benefits to attract workers.

We support higher wages if small businesses, which employ almost half the labor force, have the margins to pay and the ability to improve the productivity of their workers. Otherwise, they will pass the wage increases on with higher prices or shut the doors.

I believe we are witnessing that now.

Upshot

When today’s inflation print is put into the context of current financial conditions, as measured by the Chicago’s Fed Index, the U.S. economy has never seen this high short-term core inflation with such easy financial conditions, at least in the 50-year data set, we are looking at.

It won’t matter until it does, and then it will matter, and really matter.

Until then everyone’s making money, the Wall Street crowd tells us everything is awesome, and to party like its the 1920’s, maybe right off a fiscal cliff.

Wall Street and the government, who have a vested interested in low inflation prints, will promote the transitory narrative. Seniors and those on fixed-incomes will suffer until their Social Security cost of living increases (COLA) partially make them whole.

We also doubt seniors are buying used cars. Someone should go ask them if their monthly purchasing power is increasing or decreasing.

Markets

The markets?

They’ll get religion but the timing is tough.

When they do, however, and start selling assets, the “D” word, as in deflation will be back in the headlines because that is the kind of asset-dependent economy the U.S. has morphed into, folks.

Marx (Karl, not Groucho) was wrong on many things but had a brilliant analysis of how society progresses through conflict, explained by the Hegelian dialectic. We apply it to monetary policy analysis

In the asset-dependent economy, where asset prices need to rise to stimulate demand as wages and income are insufficient to clear the goods market, valuations eventually overshoot, consumers begin to feel like millionaires, and start to spend that wealth.

Goods and service price pressures increase, monetary authorities react — not sure if they can now given valuation and debt levels — by pumping the breaks and asset markets flop. Wash, rinse, repeat.

We concede the wealth effect is much less prominent with the uber wealthy as they have much lower average and propensities to consume than the middle class but the asset markets have a much larger outsized effect than most economists tend to believe. This is being tested in real time with the COVID as real “helicopter money” is getting to the hands that need it and spend it. But inflation…

The thesis – inflation — sows the seeds for the anti-thesis forces – deflation – when monetary policy is perceived to be about to change. From that conflict arises the synthesis, a new and more convoluted monetary policy to prop up assets.

The dialectic is probably coming to an end, however, as inflation ticks up and the Fed is now perceived as the problem and not the cavalry.

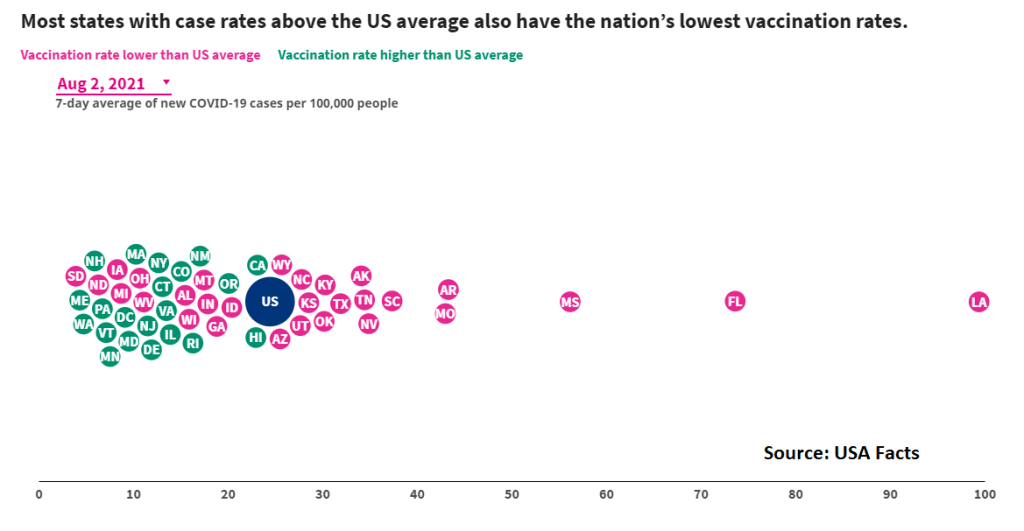

Just a follow-up to our last post, Will The Delta Variant Shut Down The Economy?, take a look at how surprisingly low Taiwan and South Korea’s fully vaccinated populations are. Taiwan’s rate is so low, that we suspect (with little conviction) it could be bad data.

The countries that have not done mass vaccinations could be hit hard with the Delta variant. Some had dodged the COVID bullet in 2020 and became complacent, not making sufficient efforts to secure vaccines, while others could not afford them.

We suspect Japan’s low vax rate, even though the country has thus far kept COVID at bay, led to Prime Minister Yoshihide Suga’s decision to declare a state of emergency. New cases are starting to tick up just as the Olympics are ready to begin, running through July 23 to August 8, and will be held entirely under emergency measures.

France Considers Mandatory Vaccinations

With only 36 percent of its population fully vaccinated, France is now considering making COVID-19 vaccinations compulsory as it struggles with lagging take-up of injections and a growing wave of new cases of the Delta variant

Semiconductors

In December, Trend Force projected 82 percent of total semiconductor foundry revenue would come from Taiwan and Korea, the primary reason why advanced economies desire to develop and expand their semiconductor manufacturing base.

Taiwan Secures Vaccines

Major Taiwanese tech companies have inked a deal to buy 10m vaccine doses for Taiwan, sidestepping months of complicated geopolitical wrangling between Beijing and Taipei.

…The US$350m purchase from German manufacturer BioNTech, is split between TSMC, the world’s largest semiconductor manufacturer, and Foxconn, one of the world’s largest contract electronics makers, and its charity foundation. The two companies will donate the vaccines to Taiwan’s central epidemic command centre for distribution.

Taiwan is suffering major shortages of vaccines, in large part due to global supply issues, but it has also accused Beijing of scuttling an early deal to secure 5m doses directly from BioNTech. Beijing denies the accusation, saying Shanghai-based Fosun Pharmaceuticals had sole distribution rights for the region including Taiwan, and that Taiwan was welcome to go through them.

But to accept Chinese-made or -donated vaccines would be “the kiss of death” politically for Taiwan’s ruling party, analyst Drew Thompson said last month. Despite never ruling Taiwan, China’s Communist party (CCP) government claims it as a province, which it vows to retake. The CCP has recently increased pressure and military intimidation of the island and its occupants.

Taiwan has rejected China’s offers as fake altruism. China has accused Taiwan of putting politics above its people, while simultaneously lambasting doses donated by the US and Japan as foreign interference. – The Guardian, July 12th

Here’s to hoping the vaccines are distributed quickly, like yesterday.

Tune out the nonsense, turn off the news, and stick to the data, folks.

The Wall Street clowns are at it again, spreading fear and loathing about the new strain of COVID, the Delta variant, retrofitting a new negative narrative to explain the nonsensical bond market action.

They thrive and need to create volatility to make their year-end bone.

No Signal, All Noise

The Fed nationalized the bond markets long ago. Trying to decipher an economic signal from bond yields is equivalent to guessing what price the central authorities in the old Soviet Union would set for blood sausage.

Are bond yields falling because the economy is about to go into a tailspin or a stock market collapse is imminent? Anything is possible, and nobody knows the future, but highly unlikely, at least until the Fed starts to pump the breaks. There is way too much money in the global monetary system.

The collapse in bond yields is all technical, baby. What a tremendous shorting opportunity if it were a proper market with true price discovery. We have done a lot of work analyzing the bond market in the past week and hope to post it for you this weekend.

Wait for it. It will be good. Promise.

Good Gawd, Such Nonsense

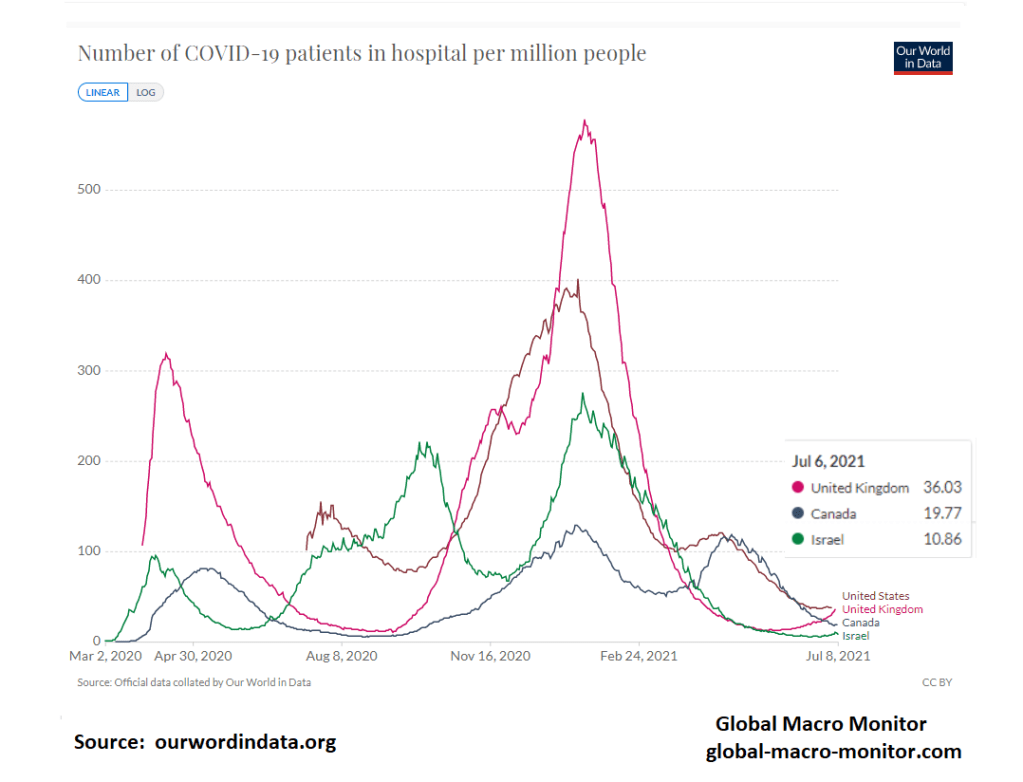

The Delta variant is a real threat to the unvaccinated, especially in the states with relatively low vax rates.

However, many states and advanced economies are almost at herd immunity — vaxed plus COVID recovered — including the UK where cases are spiking.

…it seemed inevitable that new cases of Covid-19 – which had been steadily declining since early January – would begin to rise again. On June 24, the number of daily infections in the UK crossed 16,000, levels not seen since early February when the UK was still in full lockdown.

But the third wave will look very different to the last two. While the Delta variant is considered to be more virulent than any that have previously followed, the UK’s successful vaccination campaign appears to have broken the seemingly inevitable link between cases, hospitalisations, and fatalities. The current hospitalisation rate remains low. There were 182 new hospital admissions on June 22 – a rate of 16 per 1000 new cases – compared with 3,812 admissions on January 12, the height of the second wave, a rate of 84 per 1000 new cases. – Wired

Share Of Population Fully Vaccinated

Number Of COVID-19 Patients In Hospital

Let The Games Begin

Though Japan has been relatively successful in keeping COVID at bay, the country’s low vaccination rate is rattling nerves as the athletes arrive and the Olympic Games are about to begin.

Olympics organizers are banning all spectators from the games this year after Japan declared a state of emergency that’s meant to curb a wave of new Covid-19 infections.

It’s the latest setback for the Summer Olympics that have already been delayed for a year and racked up high costs for postponement. The state of emergency will begin Monday and run through Aug. 22, while the games are scheduled from July 23 to Aug. 8. – CNBC

Upshot

Ignore the noise, folks, stay data-dependent. Change your view as the facts and data change.

Of course, there are states and countries still at high risk with their low vax rates. The advanced economies need to pull out all the stops to do all they can to help get shots in the arms of those at risk.

It’s kind of tough, however, given all the ignoramuses spouting their fascist conspiracy nonsense. They are the true modern-day brown shirts.

The far right-wing lawmaker has likened COVID-19 vaccination outreach to the reign of terror mounted by Hitler’s “brown shirts” during the Nazi era. – Daily News

I used to go home every night as a young Wall Street trader worried about how instability on the “Arab Street” would adversely impact my long unhedged positions. If you have been a reader of the Global Macro Monitor over the past few years, you know we have been concerned about U.S. political stability. – Global Macro Monitor, May 8, 2020

He was born on the fourth day of July So his parents called him Independence Day He married a girl named Justice who gave birth to a son called the Nation And she walked away

Independence would daydream and he’d pretend That some day him and Justice and Nation’d be together again But Justice held up in a shotgun shack Wouldn’t let nobody in So a Nation cried… – John Cougar Mellencamp