Source: Bloomberg

The “surge in demand” is congesting the global container ports. That is, it’s a primarily (though not all, and getting less so by the day, at the micro level) an excess demand issue creating the shortage economy.

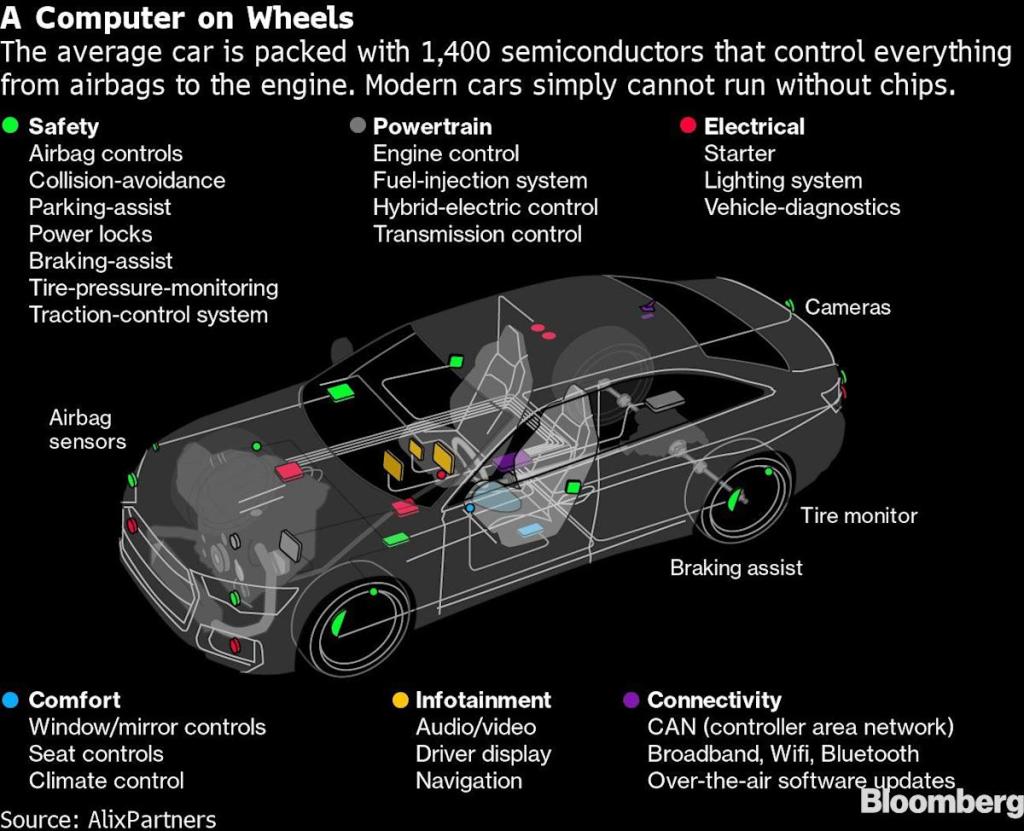

Some $10.4trn of global stimulus has unleashed a furious but lopsided rebound in which consumers are spending more on goods than normal, stretching global supply chains that have been starved of investment. Demand for electronic goods has boomed during the pandemic but a shortage of the microchips inside them has struck industrial production in some exporting economies, such as Taiwan.

...The risk now is that strains in the economy lead to a repudiation of decarbonisation and globalisation, with devastating long-term consequences. That is the real threat posed by the shortage economy. – Economist, Oct 9

American consumers are going to get a sense of what life is like in a more closed economy, one with heavy trade restrictions, this Christmas with empty shelves and big price spikes. We are not optimistic they will be able to make the right connection and proper extrapolations but we do hope we are wrong.

We are not even confident the policy makers clearly understand what’s driving the global economy. They are conducting an experiment that has never been tried in all of history. And the stock market is valued at 200 percent of GDP!

As they say in the supply chain, “it’s all downstream from here.”

We are reposting a repost of a piece we did last September.

Our sense is Mr. Xi is testing and doing the calculus if the U.S.is willing to fight WWIII over Taiwan.

Taiwan and U.S. officials have expressed alarm over nearly 150 flights near Taiwan in the past week by Chinese military aircraft. The Chinese aircraft have included J-16 jet fighters, H-6 strategic bombers and Y-8 submarine-spotting aircraft and have set a record for such sorties, according to the Taiwan government. – WSJ, Oct 7

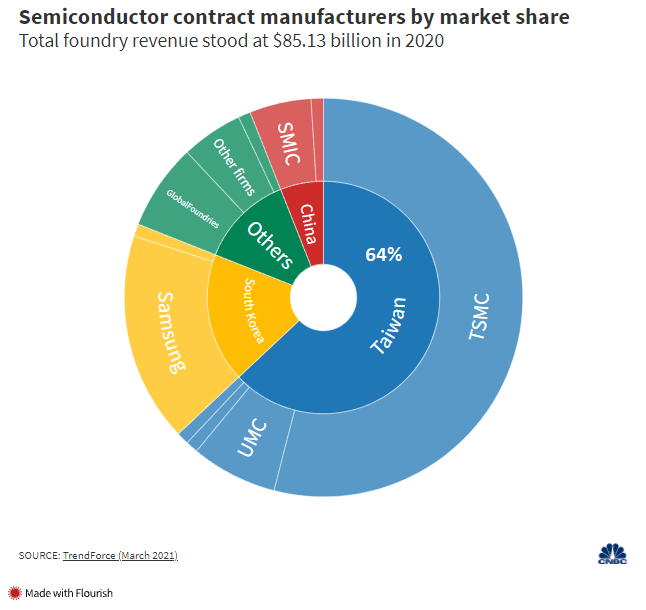

Taiwan is now the most geopolitically important country in the world in a way that no Middle Eastern country ever was. Semiconductors are the new oil, and Taiwan produces almost 2/3rd’s of semi global manufacturing.

Loose Lips, Sinks Battleships

No doubt Mr. Xi was taking copious notes as he viewed and listened to this very destabilizing and damaging interview, in which the POTUS effectively stated that America’s NATO allies were expendable. We called out how dangerous this talk was in our 2018 post, The Day “Strategic Ambiguity” Died..

Tucker Carlson: So membership in NATO obligates the members to defend any member that is attacked. So let’s say Montenegro, who joined last year, is attacked, why should my son go to Montenegro to defend it from attack?

President Trump: I understand what you are saying. I have asked the same question. You know Montenegro is a tiny country with very strong people… They may get aggressive, and congratulations you are in World War III…But that is the way it was set up, don’t forget I just got here. – GMM, July 2018

Trump is gone but Mr. Xi knows the country is divided and 74 million Americans voted for Mr. Trump.

If the Evergrand crisis spins out of control, will Mr. Xi need to Wag the Dog?

摇狗 Yáo gǒu?

As with all things in the market, it doesn’t matter until it matters. It is starting to matter.

Currently, low risk, high impact event with the temperature rapidly rising.

No Pom-Poms

Sorry, folks, we don’t do pom-poms at GMM.

Nevertheless, we have given up on how markets will react — to just about any and everything, for that matter — as tensions ratchet up in the Straight. We have are suspicions, and they don’t make us sleep better at night even in this everything market where everything is bullish.

Protect your Blind Side, folks. Keep the Taiwan Straight on your radar.

One of GMM‘s most excellent followers, who we very much like and respect, responded with this:

In an interview with Fox’s Tucker Carlson last night, President Trump seemed to question the raison d’être of NATO and foreign alliances in general.

Tucker Carlson: So membership in NATO obligates the members to defend any member that is attacked. So let’s say Montenegro, who joined last year, is attacked, why should my son go to Montenegro to defend it from attack?

President Trump: I understand what you are saying. I have asked the same question. You know Montenegro is a tiny country with very strong people… They may get aggressive, and congratulations you are in World War III…But that is the way it was set up, don’t forget I just got here. – The Day “Strategic Ambiguity” Died. GMM July ’18

Wonder what our dear reader is thinking now?

A nice little factoid to impress at a cocktail or…err…Cannabis party as we usher in the new quarter.

October is here, and in the Northern Hemisphere, that often means the days are flush with falling leaves, chilling weather, and growing anticipation for the holiday season.

The tenth month by our Gregorian calendar, October shares a root with octopus and octagon—the Latin octo and Greek okto, meaning “eight.”

Why is October named after the number eight?

According to the original Roman republican calendar, October was the eighth month of the year rather than the ninth. The Roman calendar was only 10 months long and included the following months: Martius, Aprilis, Maius, Junius, Quintilis, Sextilis, September, October, November, and December. As you can see, January and February hadn’t been added to the calendar yet!

Like its neighboring months September,November, and December, the month of October kept its numerical name, even after Julius Caesar expanded the calendar year from 10 months to 12. October entered Old English via Old French, replacing the English vernacular term Winterfylleð (“Winter full moon”). – Dictionary.com

Stunning. Hedge funds hoovering up trading cards as an “alternative to equities” with the same passion Brooks Robinson hoovered up ground balls.

This is usually a sign of the endgame for markets, i.e,, the precursor to a bear market. Think the “Great Beanie Baby Bubble” of 1999.

In general, there are two types of assets,

Creating An Illusion Of Scarcity

Scarcity relative to the money stock is what its all about now, folks.

It probably won’t be long before the Fed has to bailout the baseball card market, no?

Full disclosure, I do own a Mike Trout rookie card.

Given the extreme valuations of all most all asset classes, coupled with the massive amount of money in the global financial system, markets are now really stretching, looking for, and actually attempting to create scarcity as a useful delusion to justify, rationalize, and drive speculation.

Maybe I will start collecting poop as an “anthropological asset,” put it the blockchain and super charge the price ramp by snapping a few pictures of each sample, converting them to NFTs to load up to the internet.

Then again, maybe all this is signaling the start of a big, big inflation cycle and the markets are looking to get out of cash and protect their purchasing power. But that’s too rational.

Can you believe what the markets have become, folks? It is hard to see clearly when everybody is making money.

#CKStrong Never forgetting Carol K. We are with you, girl!

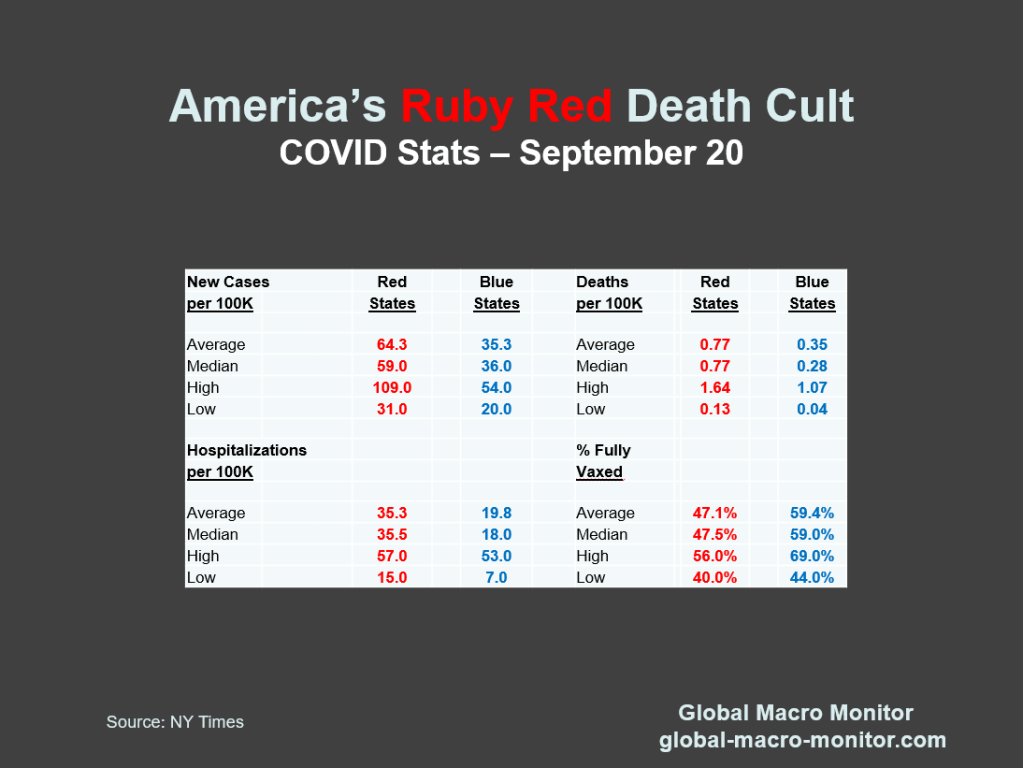

Anyone see a pattern here?

If you stare at the chart long enough, you can see the pink red elephant [in the room].

Sadly this chart is largely a function of the state’s politics. Doesn’t have to be that way and people shouldn’t have to die for it.

America’s Death Cult And The Pro Life States

Never thought a large swath of America or a major political party would morph into a Jonestown death cult but it has. The data speaks for itself.

The following was originally posted at custerconsulting.com.

Summary

As summer fades, the global economy is downshifting from months of super-charged growth, pumped up by unprecedented fiscal and monetary policy measures. Growth will continue throughout the year but at a sharply decelerating rate, and inflation will remain stubbornly high.

Supply chain issues — components, commodities, and labor shortages — are now the primary constraint on growth. We do expect demand to continue to soften over the next few months, however.

Even though global electronics production continues to rise, the rate of expansion has slowed significantly in the past few months.

We have constructed a narrative of the global economy, which we believe is unique and reflects the economic reality driving electronics manufacturing. As we have stated in the past, current market conditions are driven mainly by the macro.

We believe it is essential that purchasing managers think “big” – i.e., the global macroeconomy – to understand their market conditions better.

If we could point to one piece of data or chart explaining current conditions and the economic trajectory over the next six months, it is Chart 8, U.S. Retail Sales Are 12.7% & 52-Months Ahead Of Pre-COVID Trend.

What’s The Matter With The Global Supply Chain

The bulk of the problems in the global supply chain are caused by excess demand. Policymakers have injected too much stimulus into the global economy. By combining income support through transfer payments, the central banks have effectively monetized much of the large deficits and spending run-up.

Our view is derived from Chart 8, where we use U.S. retail sales as a proxy for global aggregate demand. The EU’s retail sales chart looks very similar.

Chart 8 illustrates that spending unexpectedly came roaring back after an unprecedented drop when global economies were turned off in March 2020 and had a massive “Bullwhip Effect” on the global supply chain.

See below for the informative interview with TJ Rodgers, former Cypress Semi C.E.O.. on fixing the supply chain.

The spike in demand was, in large part, fueled by the governments’ income support policies and over $9 trillion of digital money created from thin air and injected into the advanced economies by central banks.

July’s retail sales – our proxy for global aggregate demand, which is not observable, by the way – are 12.7 percent above and running 52 months ahead of its pre-COVID trend. Retail sales are inflated by the policy measures and will need time (52-months of zero growth) and/or space (-11.2% down from current levels) to get back to trend. No doubt, it will be a combination of both time and space. A sharp, abrupt correction in retail sales could be painful and confuse the supply chain even further.

We believe only when demand returns to trend will the global supply chains begin to heal. Some will sooner than others, but it will take longer than most expect unless the global economy hits the skids big time or the central bankers panic.

In no way are we taking shots at policymakers. They had just as tough of a job like all of us trying to figure out what was going on after the pandemic began its rapid global spread. Moreover, the problem of too much demand and inflation is a better problem to have, much better, at least to us, than riding out a deep recession.

However, we do question the need to continue such policies, especially further monetary injections, and suspect policymakers fear a significant and hard sell-off in overvalued asset markets. If asset markets do correct hard, it won’t be long before we’re discussing deflation as the advanced economies have become very asset-dependent.

Transfer Payments Fading

Transfer payments, which make up the bulk of the income support policies, are starting to fade. The U.S. government emergency unemployment payments ended this past week, which will slow consumer spending on the margin.

Stagflation Cometh

Nevertheless, Christine Lagarde, president of the European Central Bank, who has started baby steps in pulling back Europe’s stimulus, recently stated,

“The lady isn’t tapering…”

It doesn’t appear governments have the stomach to take the economic pain of clamping down on demand, and our takeaway from the soft rhetoric from the central banks is “stagflation” cometh. That is, inflation will be around longer – not transitory – than conventional wisdom suspects as economic growth slows sharply.

Expanding Long-Term Capacity

Of course, the supply side can adjust, increasing production capacity to meet the current excess demand to bring imbalances into equilibrium. It would also reset the potential output trajectory for higher growth.

A significant expansion of long-term production capacity is not likely, as many producers, rightly so, are skeptical that demand, where retail sales are still two standard deviations above their three-year moving average, is sustainable (Chart 9). We suspect most producers will try to meet demand by working their factories and employees overtime rather than increasing their long-term capacity to produce through new factories, machines and hiring new employees.

We do believe the pandemic has ushered in a structural shift in semiconductor demand as the pandemic had accelerated the digitization of the global economy. (see Charts 5-6).

Demand In The U.S.A.

We suspect much of the excess demand is coming from the U.S.. Chart 10 illustrates most of the world’s ports seeing high congestion rates, are located stateside.

We don’t dismiss that real supply shocks, such as factory shutdowns due to new COVID outbreaks, are hitting the supply chain, but they are not the main driver.

Much of the supply chains problems are also in transportation, where ocean freight takes care of 95 percent of global trade. Check out Chart 11, which shows almost 50- ships are floating around the L.A. and Long Beach ports waiting to offload their cargo.

Last month we worried out loud how the low vaccination rates in Southeast Asia could impact the supply chain (Chart 12). The latest from Toyota,

Toyota Motor Corp. trimmed its production outlook for this year by about 3% because the spread of the coronavirus in Southeast Asia has disrupted access to semiconductors and other key parts. – Bloomberg

Based on our analysis, our best guess is that stagflation is not transitory and will be with us longer than anticipated, and the supply chain will not start to improve until U.S. retail sales move back to trend.

Sales are slowing. Since March, the charts illustrate sales growth has stalled, albeit at a very high level and well above trend.

Click here to view video