In my prior life I used to trade emerging market (EM) bonds and came up with the following analytical framework using options analysis to understand and teach the basic fundamental principles of how to value EM hard currency bonds. The analysis is relatively crude and simplistic but a very powerful tool to internalize the understanding of valuing emerging market fixed-income securities.

The analysis is timely given Argentina’s recent sale of a 100-year sovereign bond.

Option Based Analytical Framework

Because the value of corporate securities is, in effect, a contingent claim on the firm’s value, options analysis can be applied to construct an alternative analytical framework to determine and understand relative value. Equity is essentially the residual claim on the value of the firm after all liabilities have been paid. If bankruptcy occurs, equity holders receive nothing.

The economic return to equity holders is therefore the maximum of zero, or the total value of the firm’s assets less all outstanding debt liabilities. The equity claim is thus a call option on the value of the firm with the strike price equivalent to value of the outstanding debt.

Corporate Bonds As A Hybrid

In the event of bankruptcy, equity investors are off the hook if the value of the corporation falls below zero when liabilities exceed assets, but they lose the entire value of their claims on the firm, however. The limited liability of a common stockholder therefore corresponds to the limited downside of a holder of a call option.

Using this framework, corporate bonds are then effectively a hybrid of a risk-free bond and a series of annual puts written on the value of the firm. The strike price of the put is also equivalent the point at which the firm’s assets equal its debt outstanding.

If the value of the firm’s assets fall below its debt liabilities, the loss to the bondholder is similar to the loss of a writer of a put option. The loss to the bond holder is the difference between the liquidation value of the firm and value of the debt outstanding. The bond’s credit spread over the comparable risk-free rate is equivalent to the annual option premium bondholders receive for writing the implied put.

Note this a very simplistic analytical framework and ignores many factors such as the firm’s capital structure, for example, but has very powerful conceptual value. The same analysis can be applied to credit default swaps (CDS).

Application to Emerging Market Sovereign Bonds

The option-based framework can be extended to better understand the nature of sovereign risk, particularly transfer risk, inherent in emerging market hard currency bonds. The option based analysis is modified, however, from a balance sheet perspective to a cash flow perspective. Lack of clear international bankruptcy proceedings and access to the sovereign’s balance sheet limits the analysis to a flow (cash flow) versus stock (balance sheet) variables.

Emerging market dollar denominated sovereign bonds can similarly be viewed as a hybrid of a risk-free bond and a series of puts written on the level of the international reserves of the issuer country. This assumes all risk factors, including political, economic, willingness to pay, and the global macro factors are reflected in the level of the country’s international reserve position. Not an unrealistic assumption as material changes in these risk variables will impact capital flows and the country’s reserve position.

Strike Price On International Reserves

The strike price of the put is the minimum level of reserves to cover the country’s debt service. The credit spread on the emerging market bonds is therefore the option premium for writing the annual put on FX reserves.

As the reserve position declines, for example, and moves closer to the strike price, or minimum level of reserves, the put premium or credit spread should increase. If reserves move below the minimum level, the loss to the bondholder is the same as the loss on the put, or difference between debt service actually paid and the contractual payment.

Conversely, as reserves rise to a debt sustainable level, the put moves further out-of-the-money and the options premium or credit spread declines. The expected volatility of capital flows, the country’s foreign exchange reserve earnings, and import volatility will also affect the premium value or credit spread.

The figure below shows the annual payoff of each put written on the value of the country’s foreign exchange reserves. As reserves fall close to or below the minimum level for debt service, the put moves in-the-money.

Default

If the country defaults calculating the recovery value is much more difficult than in a corporate default as bondholders rarely have access to a balance sheet and a bankruptcy judge. The workout is subject to good faith negotiations and the estimated debt servicing capacity of the country. Fairly complicated.

We’ve done some back of the envelope calculations on a 10-year bond with a credit spread of 330 bps at issuance. The present value of the credit spreads or “put option premiums” is about 30 percent of the value of the bond.

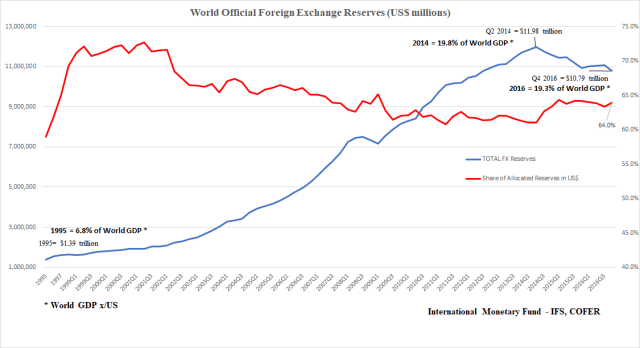

Large Increase In International Reserves

From the mid-1990’s to around 2014, the world experienced a large increase in international reserves. This was the result of three major factors.

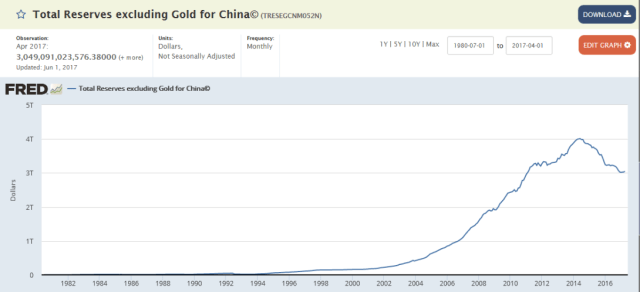

First was the rise of China as an export powerhouse and its massive build up of FX reserves.

Change in FX Regimes

Second, after the Mexican peso and Asian Financial crises of the mid-to late 1990’s, emerging market policy makers learned a hard lesson that running large current account deficits as the result of strengthening currencies could lead to a very destabilizing and costly balance of payments crisis. Policy makers became very vigilant not to allow their currencies to become overvalued and intervened in their foreign exchange markets purchasing the dollars and thus increasing their reserve positions.

Third, the U.S. began to run larger current account deficits and effectively monetized them though relatively easy monetary policy. The result was an abundance of excess dollars in the international financial system, which found their way into the official accounts of foreign central banks.

Tight Spreads and High International Reserves

Using the above analysis makes it easier to understand why EM sovereign dollar bonds are trading so tight, or so wide, for that matter. Just take a look at the following time series of the international reserve position of some of the major emerging market countries.

.

.

.

.