Summary

- Big move in 10-year yields fueled by dovish Fed and ugly German economic data

- German 10-year Bund yields crossed into negative territory

- Turkey and Brazil bond yields blow out on currency weakness and Brazil’s political risk we spoke about at the start of the year now biting

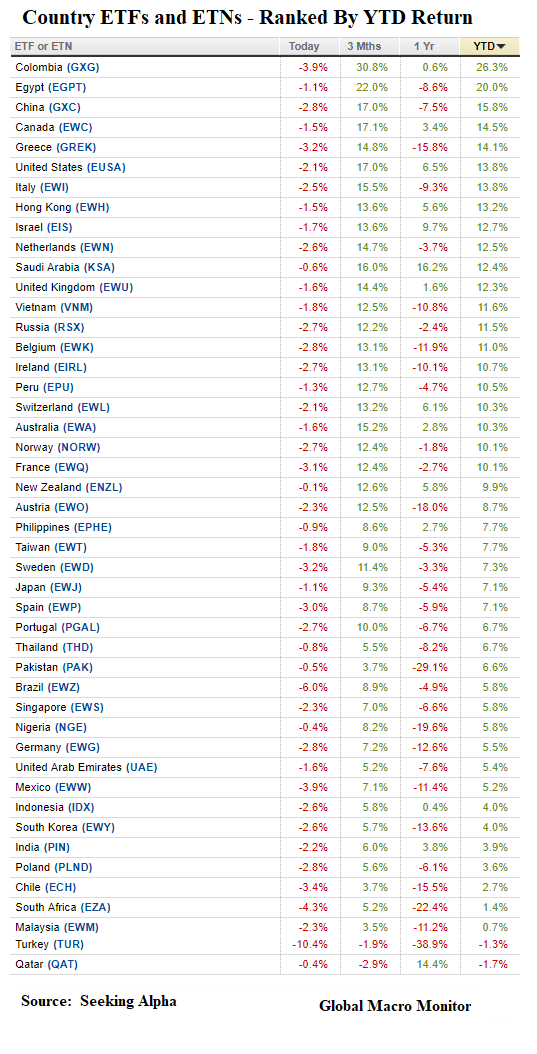

- Major Latin FX getting spanked why Asia hangs in

- S&P down less than 1 percent on the week though felt worse. Friday’s close fugly

- Latin stocks spanked

- Russell, the January, and February darling giving the most back of U.S. majors

- Gold starting to catch a bid again

Commentary: Our Power of Zero (POZ) thesis, i.e., markets are driven by yield-chasers panicked that interest rates are going to zero, had a big set back on Friday’s ugly German data and the feedback into the U.S. yield curve. As we said, last week POZ would be a bullish driving force for markets until we see the white in the eyes a global recession. The market thought they saw white on Friday.

Still, we believe the markets should settle down this week unless more super ugly economic data confirms. The yield curve is freaking out traders and investors, and the Fed is now paying the consequences of its over-engineering in the interest rate complex.

It’s not just the Fed, but the major global central banks. French Oats 230 bps through the U.S Treasury in a currency nobody can say with certainty will be around in ten years? Come on, man! Global monetary policy = reductio ad absurdum.

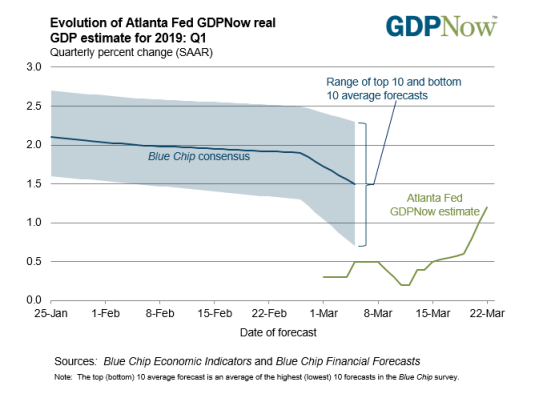

Staying close to home until we see if Friday’s volatility carries over into the new week and watching the data. Note the Atlanta’s Fed GDP now forecast for Q1 2019 has moved up from around 0.5 percent at the beginning of the month to around 1.2 percent, which is a big move lost on the markets.

The markets are now pricing almost a 20 percent probability of a Fed rate cut by the June meeting, and a 67 probability by January 2020 with a 20 percent probability of an additional cut. We don’t see a recession this year in the U.S. and once the markets get through this squall should begin to move higher.

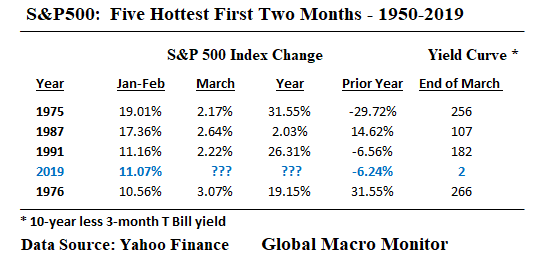

Unless this time is different. The year’s record start, after a down year, implies a higher S&P not only in March but by the end of the year. See the table below.

Back to back down years are very rare. We are working on a big piece on this which should be posted early in the week.

Nevertheless, though we think stocks finish the year higher, we don’t like the market and have been selling out on the way up. The longer-term valuations are way too high or close to record highs, the global geopolitical tectonic plates are shifting, and the post-War order is crumbling.

Longer-term investors should not be chasing markets here, in our opinion, and using the strength to take risk off into this, what we believe, will be the speculative blow-off before the Big Dipper, providing investors with a chance to buy cheaper.

Those depending on the year-end bone — all of the Street — and traders who depend on weekly cash flow to feed their children will end up chasing this market higher as TINA will seduce and force them in. TINA as in (T)here (I)s (N)o (A)lternative. Two percent 10-years in the U.S. and negative rates in Germany ain’t gonna pay the rent, folks.

Finally, global central banks have FUBARed the economic signals, which have been traditionally extracted from interest rates and yield curves. How in the hell is one supposed to divine info about anything after years of engineering yield curves and central bank bond purchases that now price Portugal’s 10-year sovereign risk (1.26 percent) at almost half that of the United States (2.46 percent)? That is a double rainbow in our book, folks. What does it mean?

Yada, yada, yada!. The relative Euro/U.S. 10-year yields reflect interest rate parity, and the path of the spot dollar will follow the forward rate lower against the euro over the next ten years. Yeah, right. Good luck with that trade.

How ironic would it be if market fears based on distorted interest rates and yield curves are a major factor in taking down the global economy?

Imagine Jay Powell trying to explain that one or POTUS and S. Moore trying to understand it!

2019 Q1 GDP Forcast Has Almost Doubled Since March 1

Is This Time Different Because Of The Yield Curve?

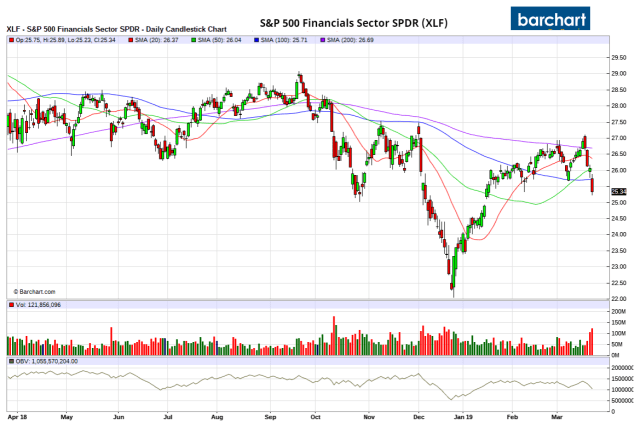

Financials ETF Breaks All Four Major Moving Averages

Brazil ETF Moves From Top Dog To Middle of Pack

Bg Move Down In Global 10-year Yields

Pingback: Beware Of Retrofitting Fundamentals To Price Action | Global Macro Monitor