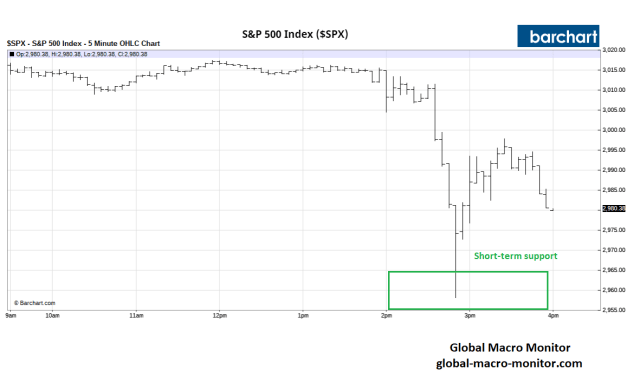

Gravity. Stock prices are waaay too high.

Stocks went down not because the Fed messed up. If they needed to cut 50 bps and signal more to come because of coming economic weakness, what in heavens name were stocks doing at record highs and extreme valuations? Nobody knows the future.

Expecting the Fed to see all, know all and precisely fine-tune the economy and markets is tantamount to having someone thread a needle with boxing gloves on and blindfolded during a rollercoaster ride. The belief that they can have distorted markets beyond all repair.

Seriously, folks, the lack of price discovery in all things financial is a big problem.

Valuations

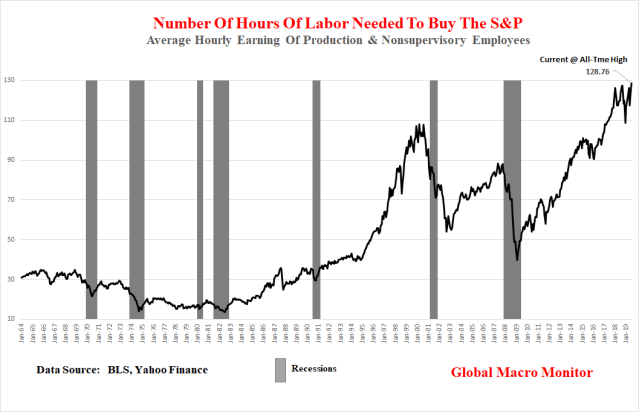

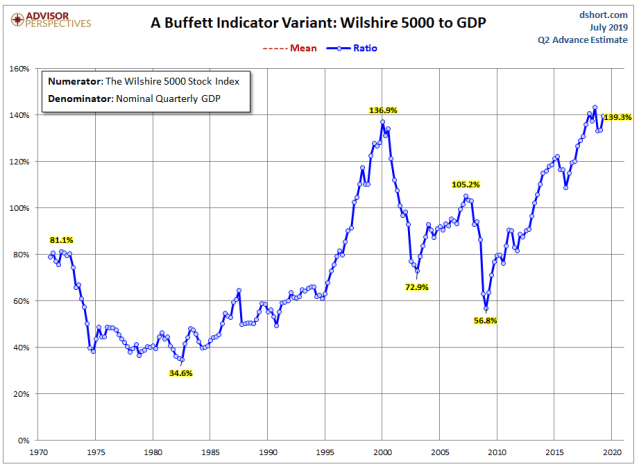

Check out the following macro valuation charts at historical extremes.

Earnings are slowing, we believe the economy is at secular peak margins and the international economic order is in tatters. The S&P is shattered!

Rally on, Garth, if you want to. Not with our long-term book, however.

The pressure on the Fed from the market socialists (see our last post) will intensify.

Moreover, given the New Economy’s feedback between asset prices, Jay Powell will soon be talking about QE if stocks are headed where we think they are.

Call it an unstable equilibrium, a stable disequilibrium, or an unstable disequibrium. You decide.

Pingback: A Short Stay At The Bear Trap Inn | Global Macro Monitor

I find two graphs both to be of interest, as to finding a valuation standard on which to view current stock valuations.

Yes, King. Micro measures are manipulated by CFOs and buybacks.