Sit up and listen, folks. We may be in the midst of a Black Swan event.

Nobody knows for certain what is creating the turmoil in the repo and money markets but we suspect much of it has to do with the increase of the trillion-dollar-plus budget deficits during an economic expansion, i.e., pro-cyclical budget deficits, which have been very rare. We have been pounding this theme over the past month. See our last post here.

If you want some context and a comprehensive understanding of the changing dynamics of financing the budget deficit and the structure of the Treasury market, go to our tome, The Gathering Storm In The Treasury Market. That piece was posted last September, just before the spike in the 10-year Treasury yield, which caused the Q4 stock market crash.

The upshot of the post was that the technical factors of the Treasury market, supply and demand, are rapidly changing and the natural path of real interest rates are higher, and there are consequences to financial repression. We underestimated just how sensitive global markets were to an even 50 bps increase in long-term bond yields but we did hedge ourselves,

All bets off given a geopolitical shock — we are concerned how quickly U.S.-China relations are moving south; a collapse in stock prices, or a sharp slowdown in economic activity. Haven flows will likely swamp the structural factors pressuring yields higher. – GMM, August 24, 2018

So, here we are, one year later with yields 150 bps lower but the Treasury still is in need of $1 trillion in annual financing. We believe the distortions are now showing up in the money markets as interest rates cannot move higher to their steady-state normal equilibrium levels because markets perceive there is too much debt in the global financial system.

If you squeeze a balloon, the pressure and bulge shows up elsewhere. Classic Le Chatelier’s principle

The Bloomie opinion page also seems to get it.

I’d offer another angle that’s largely flown under the radar: The chaos in repo markets was a long time coming given the widening U.S. budget deficits and the lenders that are financing that shortfall.

Deficits, while nothing new, add up over time. And while they declined each year from 2011 through 2015, both overall and as a percentage of gross domestic product, the gap has widened again under President Donald Trump. Put it all together, and the amount of U.S. Treasury securities outstanding has roughly tripled since the financial crisis:

This growth was mostly under control in the years after the financial crisis because the Fed had been buying up large chunks of the Treasury market through its quantitative easing programs. But it was gradually reducing the size of its balance sheet from late 2017 until July, precisely at the same time that the Treasury Department was increasing the size of its monthly auctions to finance the bigger budget shortfalls. All told, the Fed now holds about $2.1 trillion of Treasuries, down from almost $2.5 trillion previously: – Bloomberg

Central Banks Financing U.S. Budget Deficit

Since around 2000, when the Federal budget was in surplus, the U.S. government has leaned heavily on foreign central banks and then the Fed post-GFC to plug it growing fiscal gap. The Fed cannot finance the government directly by participating in the monthly auctions (unless rolling over SOMA portfolio) but do so indirectly in their secondary market purchases either through QE, and, now we argue through open market operations OMO, which, we suspect, will soon morph into POMO and another permanent round of QE. This is now taking place when the annualized core CPI over the past three months is running at 3.4 percent.

Note, at the end of July, the Fed and foreign central banks held almost 50 percent of all marketable Treasury notes and bonds outstanding. That is just stunning.

The central bank financing of the U.S. government has freed up funds and liquidity to power other asset markets and capital spending, or buybacks.

Central Banks Pulling Back

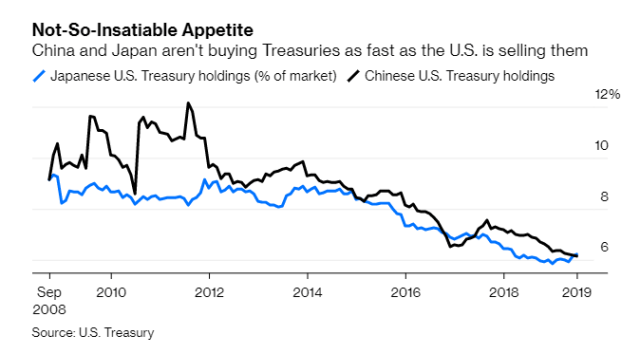

The Fed and the big central banks that matter and are scaleable – China and Japan – have pulled back their purchases of Treasuries at the same time interest rates have fallen way below, what we believe is their equilibrium technical level to clear the market. Think, rent control.

Source: Bloomberg

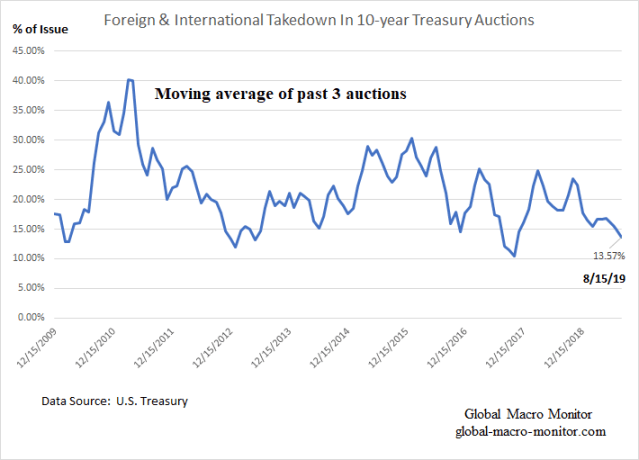

Even the narrative that foreigners are chasing Treasuries for yield doesn’t seem to be backed up by data — at least the 10-year note — from the recent monthly auctions. As of the issuance date on August 15th, foreigners were allotted just 13.6 percent on average over the past three auctions.

In fact, the August 15th (August 7 auction date) issuance allotted only 12.02 percent to foreigners and international buyers, the lowest since September 2016.

Bad Timing

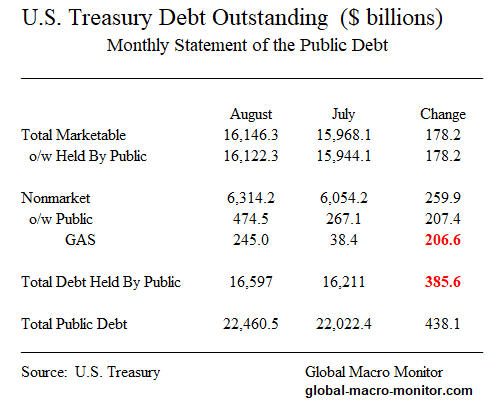

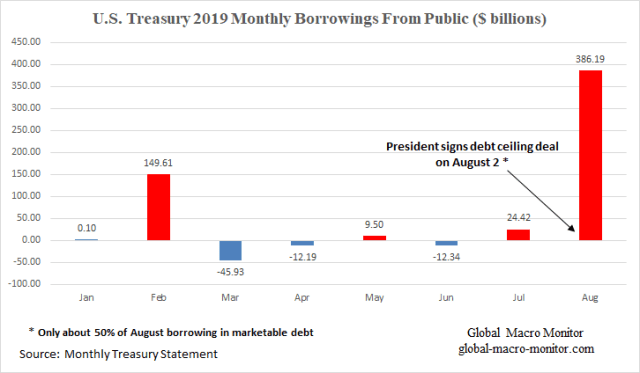

Bad timing as the Treasury, who had been forced to finance its budget shortfall prior to August by running down its balances at the Fed and by other means due to the debt ceiling, borrowed almost $400 billion from the public in August. That may, underscore may, have shocked the financial system. Kind of like the pressure building up on a beachball, which is held underwater then suddenly released.

The Treasury is pretty good at managing its borrowing to maintain market stability and issued around $200 billion of $386 billion in the form of nonmarketable General Account Series debt to the public. These Treasuries are usually issued to intragovernmental agencies – i,e, nonpublic — such as the Social Security trust funds

Who took down the $200 billion of GAS? We suspect it is a fudge factor account and we have reached out to Treasury trying to nail it down. Will let you know as soon as we find the answer.

Banks Getting Stuffed

Moreover, it does seem banks, including primary dealers, are choking on Treasury securities.

So if it’s not the Fed, it’s not China and it’s not Japan, where are all these Treasuries going?

U.S. commercial banks are certainly a place to start looking. They’ve done their part since the financial crisis, but especially lately, with holdings of Treasuries and agency securities climbing to almost $3 trillion as of Sept. 11:

Primary dealers, a select subset of banks that are obligated to bid at Treasury auctions, were saddled earlier this year with the most Treasuries ever — an outright position of almost $300 billion. Even now, their holdings are more than double what they were a year ago as they’re required to take down larger pieces of the U.S. government’s debt sales.

There are simply too many bonds (or, in the language of the repo market, “collateral”) sloshing around in the financial system and not enough cash on the other side of the trade. America’s budget deficits are being financed domestically and leading to a relentless drain on reserves – Bloomberg

So there you have it, folks, it’s not rocket science.

Too much supply in all the wrong places and not enough demand from all the right places. If rates were allowed to go to their natural equilibrium level, demand for Treasuries would increase from natural buyers and I seriously doubt the money market markets would be seizing up. But, as we know from Q4 2018, interest rates can’t go up because the stock and asset markets will and did crash.

The End Game

We have been concerned for quite some time about the financing of big budget deficits, and we mean big – the deficit from October to August 2019 is equivalent to the combined GDPs of Austria, Ireland, and the Czech Republic, especially given the distortion of global interest rates,

A question has been nagging us for some time. If the current sovereign yields are repressed and fake, many of which are negative, can the borrowers issue any significant amount of new debt at these current yields? Especially to long-term holders?

We are just thinking out loud here but our priors are that of the Big Three — U.S., Germany, and Japan — which have relatively transparent markets as opposed to China, the U.S. is the only government that needs to issue a significant supply of debt and bonds into the market. – GMM, Aug 6th

It doesn’t surprise us one bit the turmoil taking place in the money market though we thought the pressure would show up more in the monthly auctions. It could be the banks are being stuffed to window dress the auctions. Maybe, we don’t know.

We will find out soon as the Treasury will have to ramp up its net new issuance after their creative cash flow management during this year’s debt ceiling negotiations. We seriously doubt they can without another round of quantitative easing, and that monetization just may be the beginning of the end of dollar hegemony and set us on the happy road to higher inflation, which everyone seems to be wishing for. Not us, by the way – GMM, August 6th

If we are right, the turmoil in the money markets is more of a structural problem, which may, periodically, calm down depending on the matching of public and sector cash flows or the distortions may show up elsewhere and in other markets.

It does seem, however, the day of reckoning has or is coming soon on the deficit/debt-bomb so many have been warning about for so long. Of course, they will say nobody saw it coming.

The only real political choice will be to monetize the deficits, which will only significantly increase economic and financial distortions, further expanding the minefield of potential Black Swans.

Yikes, can I monetize my Soc Sec payments with some kind of viatical settlement. I need a stash so I can move to Mexico.

Pingback: What Are They Thinking? | Global Macro Monitor

Pingback: It’s Always About The Treasury Flows | Global Macro Monitor