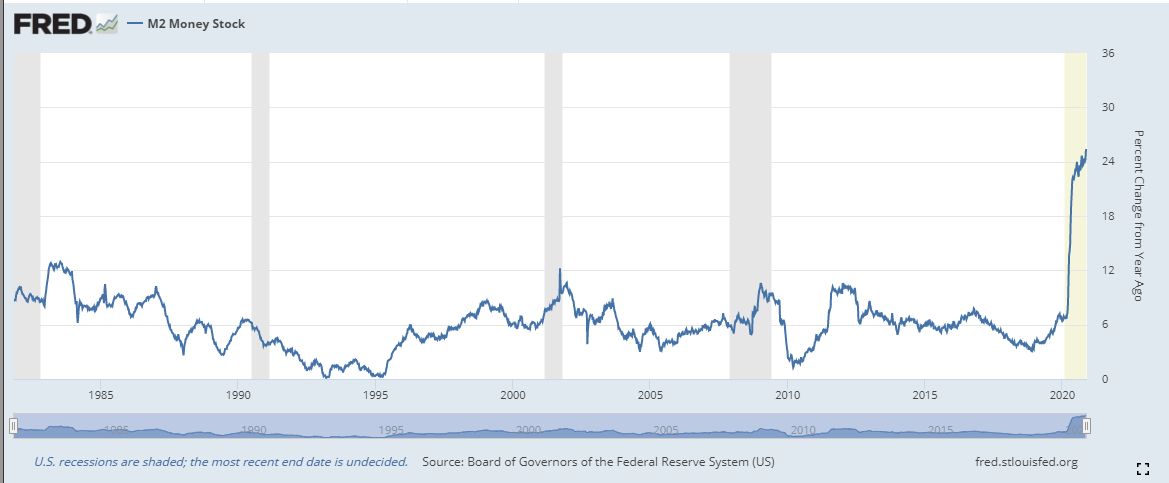

M2 Money Stock – Weekly % Year-on-Year Change

Stunning to see the weekly monetary aggregates (M2) continue to grow at an unprecedented 25 percent year-on-year rate. Not so stunning to see the stock market mania being led and fueled by the money supply growth.

Yet, it is stunning, actually frightening, to see stocks need the 25 percent money growth to sustain its momentum.

This is unprecedented and unsustainable as inflationary pressures are and will surely continue to build even in the flawed official measures. Recent data now show M2 grew north of 1 percent in November month-on-month. The challenge mounts in March when the moving prior 12-month stock of money will be at a much higher base.

The monetary aggregates are also subject to the creation of engodenous money and the vagaries of credit expansion and contraction in the private markets, which are increasingly harder to measure, track, and forecast. This crisis is the first that we can recall where the monetary emissions from the central bank have been so large and come without being in the midst of a major credit crisis.

One could argue, however, that a mini and stellar sovereign crisis erupted in the U.S in early March as the Treasury market began to seize up leading to the Fed’s massive intervention into the Treasury market in mid-March.

We posted the following just a few days before,

Can the U.S. government finance its $1.2 trillion plus annual deficits with an entire yield curve at less than 1 percent?

We seriously doubt it and the Fed is going to have to step-up big time with QE, non-QE, or let’s just call it for what it is, monetization. —GMM, March 8th

The stock market’s momentum must continue or else.

“There Is No Plateau, No Middle Ground”

The economic situation in a country after several years of bubblelike behavior resembles that of a young person on a bicycle; the rider needs to maintain the forward momentum or the bike becomes unstable. During the mania, asset prices will decline immediately after they stop increasing—there is no plateau, no ‘middle ground.’ The decline in the prices of some assets leads to the concern that asset prices will decline further and that the financial system will experience ‘distress.’ The rush to sell these assets before prices decline further becomes self-fulfilling and so precipitous that it resembles a panic. The prices of commodities—houses, buildings, land, stocks, bonds—crash to levels that are 30 to 40 percent of their prices at the peak. – Charles Kindleberger

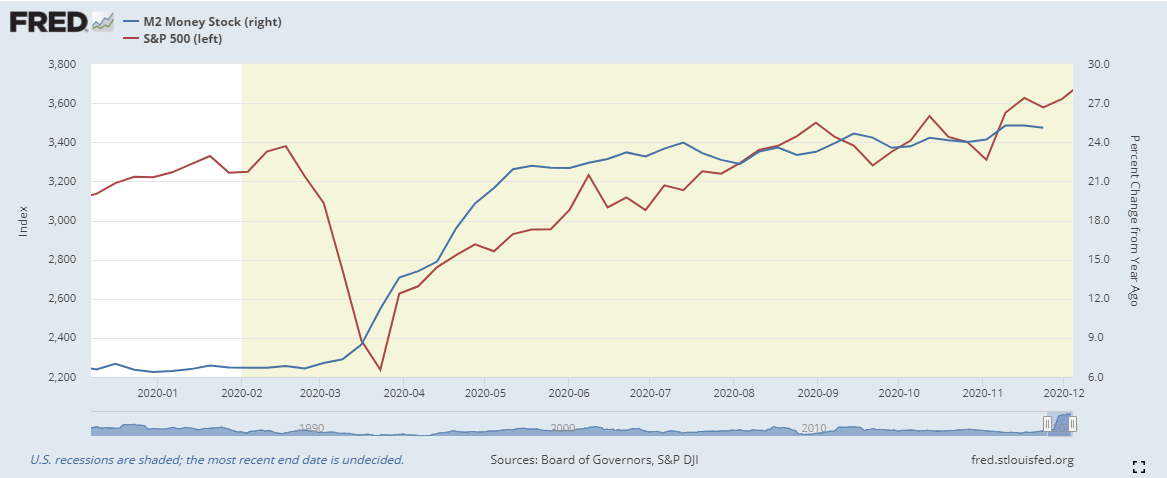

S&P500 And M2 Money Weekly Year-on-Year Growth

Inflationary Pressures Building

We closely follow the manufacturing industry, especially the electronics sector, where inflationary pressures are increasing dramatically.

This from the latest global PMI. Some hoarding is actually breaking out in various sectors as producers are expecting higher input prices due to continued supply chain issues and strong demand.

Some hoarding is actually breaking out in various sectors as producers are expecting higher input prices due to continued supply chain issues and strong demand.

Watch especially semiconductors. Recall our post on how the long secular deflation in semiconductor prices may be coming to end.

…what we believe has been one of the largest factors, along with globalization to the disinflationary forces over the past 30 years. That is the secular decline in the price of semiconductor prices. Semiconductors are the basic building block of today’s economy, as was oil during the industrial revolution. – GMM, Oct 2020

Inflation Expectations

Inflation expectations are also rising across the board.

Stocks and corporate bonds aren’t the only markets that have been looking past the pandemic—the bond market’s gauge of inflation expectations has strengthened back to pre-Covid levels as well. – Barron’s

Surprised?

After all,

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output. – Milton Friedman

The FED

We sense the Fed governors also sense and are growing increasingly concerned about all of the above and becoming reluctant to continue “carpet bombing” the economy with more monetary stimulus.

Federal Reserve Bank of Chicago President Charles Evans said Friday that although the latest job creation data is disappointing, he wasn’t yet ready to call for changes in central-bank monetary policy. – WSJ, Dec 4th

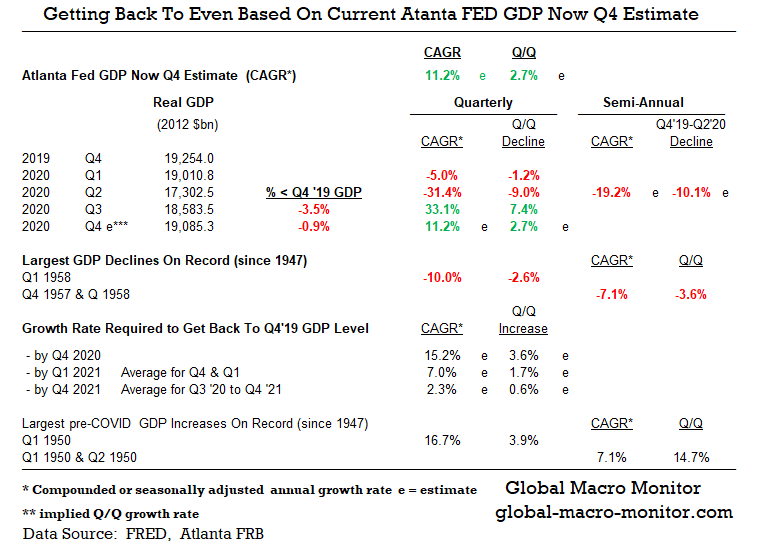

The economy as a whole is running pretty hot (GDP Now at 11.2% Q4 print) and even though the latest lockdowns as COVID cases spike could slow things a bit, economic output should be close to fully recovering its losses from the Q4 2019 peak by year-end.

Two Economies

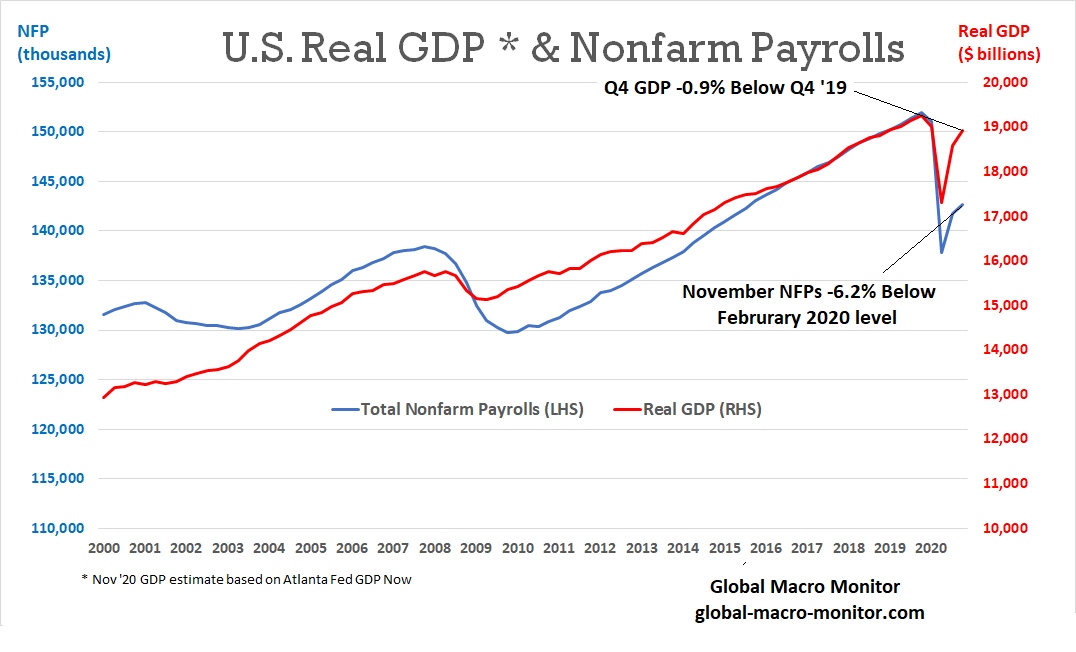

It is better to think of A Tale of Two Economies, the super-hot economy, which has benefited from the COVID crisis, and the depressed economy, such as travel and hospitality, where employment is still 20 percent below February 2020 levels vs -6.2 percent for total nonfarm jobs.

Labor Market Lagging Economic Rebound

The following chart illustrates the labor market is significantly lagging the economic recovery. Not uncommon but the distance between the two economic indicators is a bit surprising.

We suspect the hit to small businesses — who employ almost 50 percent of the labor force — accelerated automation and technology-led productivity increases are the main culprits, and we also suspect the pandemic has accelerated the disruptions and the technological-led structural economic change.

In other words, nobody knows what the future holds. Us mere humans think linearly and extrapolate past and present to the future, society and the economy progress in a nonlinear fashion.

It’s unlikely the FED is going to slam on the breaks anytime soon but it does sound they are growing increasingly concerned that there is too much stimulus in such a hot economy.

Cruise Missiles, Not Carpet Bombing

We believe economic policymakers will have to resort to strategic precision strikes on the weak pockets of the economy by bringing out the cruise missiles of targeted fiscal policies rather than using the blunt tools of monetary policy. Using monetary policy to fine-tune an economy, for example, especially an economy full of so many distortions, is tantamount to threading a needle with boxing gloves on. Good luck with that.

Still, the question remains how does Treasury finance another round of stimulus without resorting to the digital printing press as demand for its debt securities is so punk at these fake and repressed interest rates?

The Fed’s Dilemna

A 25 percent growth rate in the monetary aggregates is clearly unsustainable but the stock market is addicted and dependent on that liquidity emission, which is driving its forward momentum and keeping the bicycle rolling. Therein lies the rub, folks.

We don’t see a way out and expect the term “inflation” to come back into the lexicon of the market geniuses much sooner than most think.

A further issue to consider is given the substantial imbalances that have built up in the economy and financial market over the years, there is no middle ground on the inflation/deflation spectrum endgame but only what economists call a corner solution. That is lots of inflation or deflation.

What is going to happen to the stock market, for example, if the Fed normalizes monetary policy with the monetary aggregates growing only at their normal rates of, say, 5-8 percent year-on-year? What if the Fed has to keep the monetary spigots on to keep the asset markets afloat? It doesn’t take a rocket scientist to see the rabbit hole monetary authorities have descended in to over the past 10 years.

The Carol K. Provisio

Finally, we do have to give a shout out to Carol K., GMM’s crack stock picker, noting what she has pounded into us in 2020 — that the stock market is a market of stocks and some stocks, especially the tech stocks of the future, are in a secular bull market. We are thankful that she is on board and acts as a check on our natural contrarian tendencies to bet against the market.

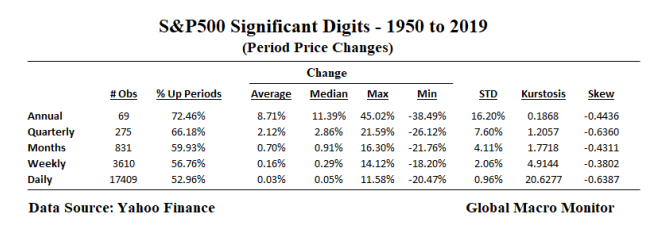

Permabulls automatically bat .700 as the stock market has risen 72 percent of the time on an annual basis over the past 70 years. That’s too easy.

Pingback: Inflation Cometh And So Is A Big Market Correction | Global Macro Monitor