We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.

An educated citizenry is a vital requisite for our survival as a free people. – Thomas Jefferson

Ceasefire Off, Risk Still On: Positioning Into a Loaded Week

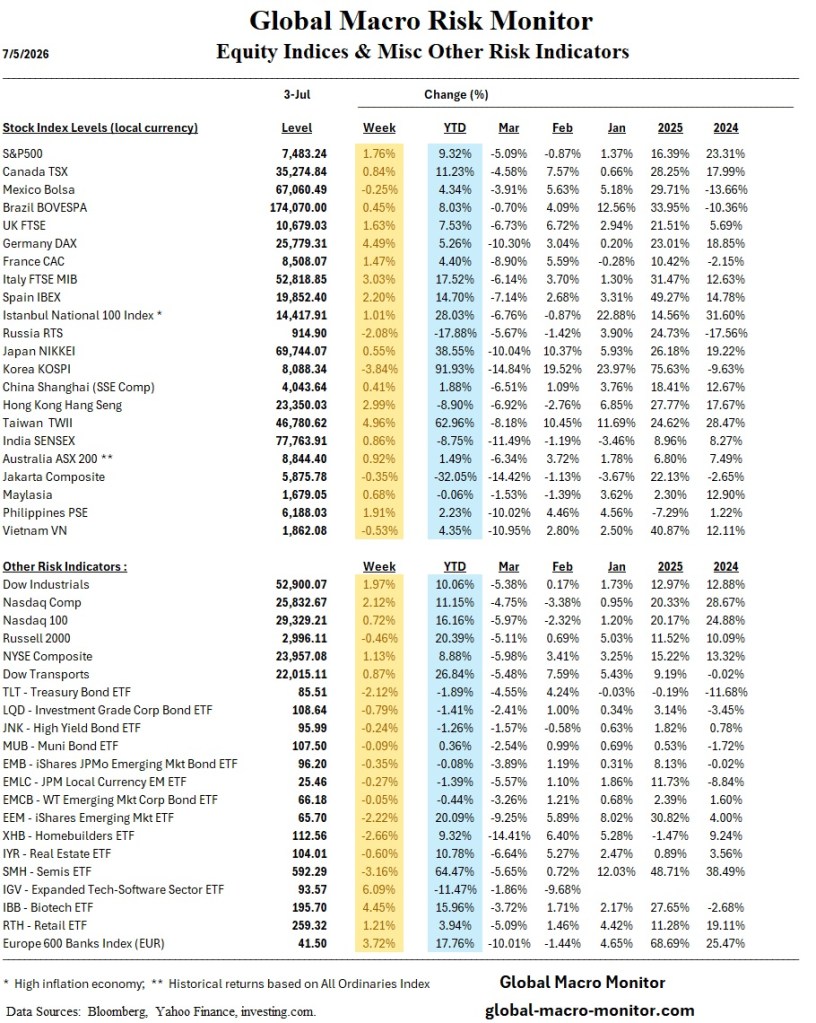

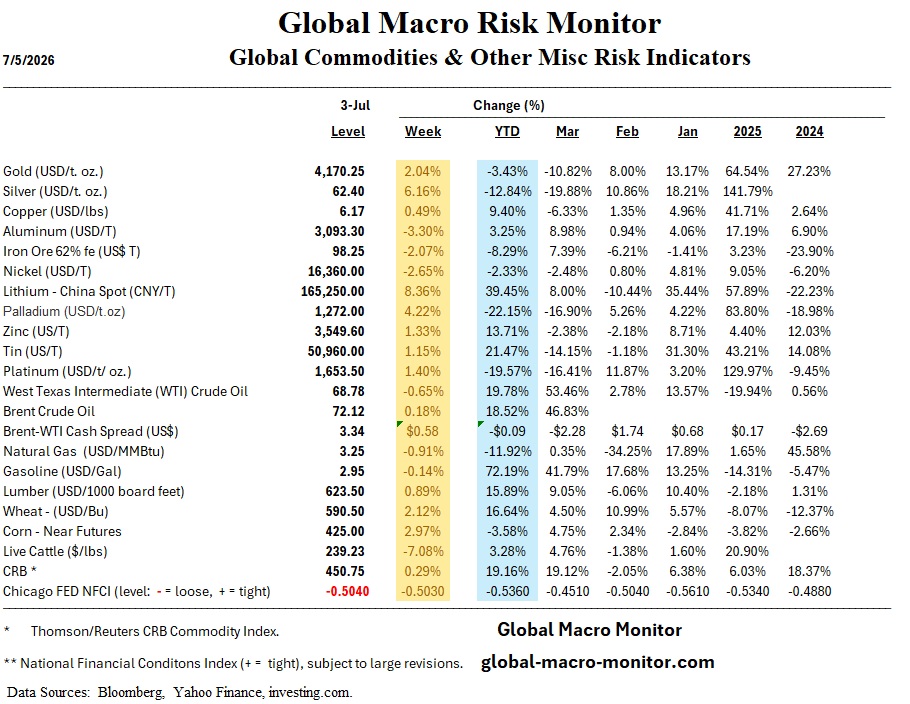

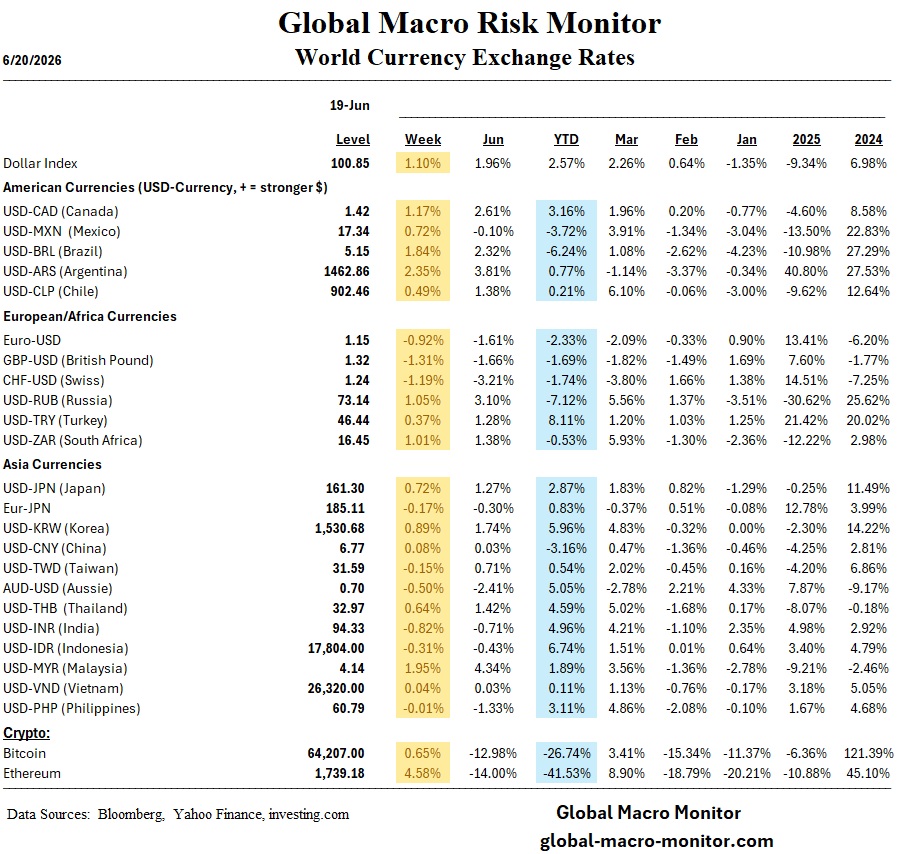

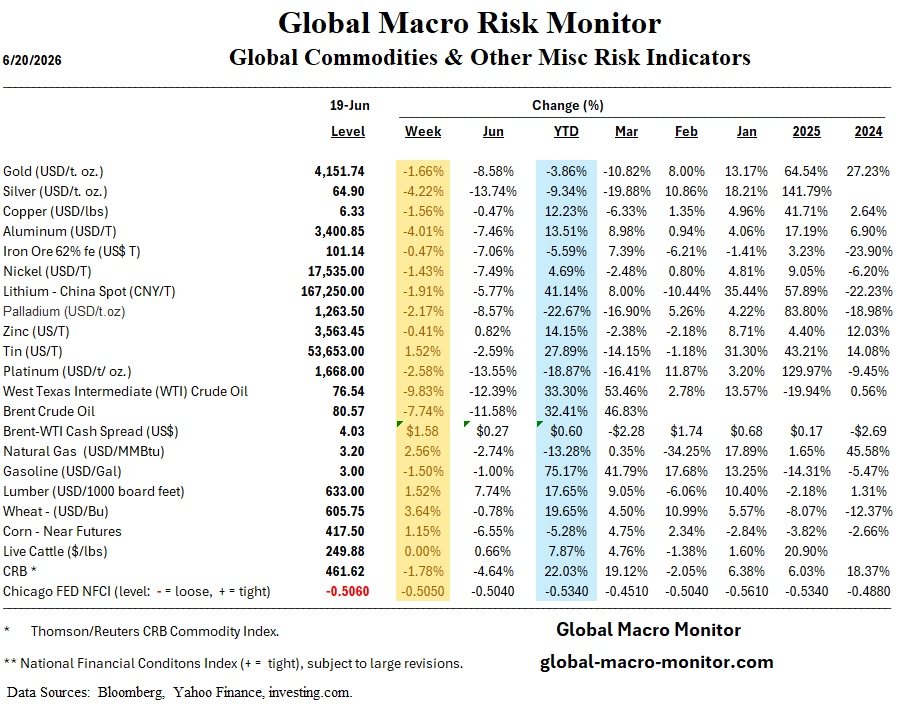

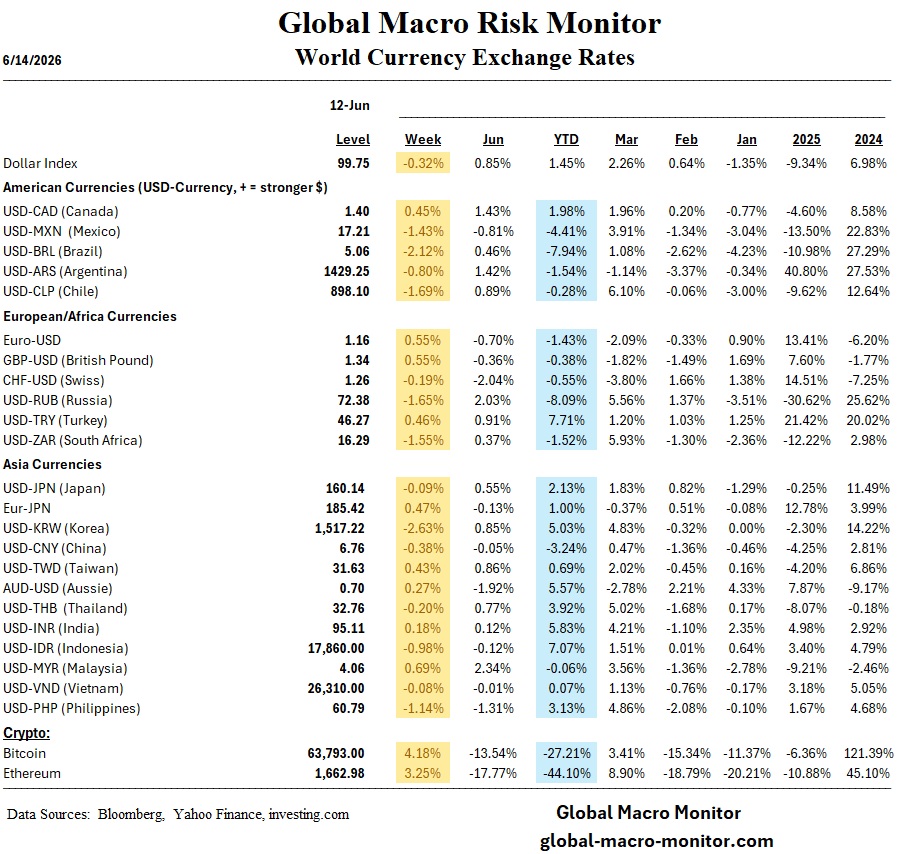

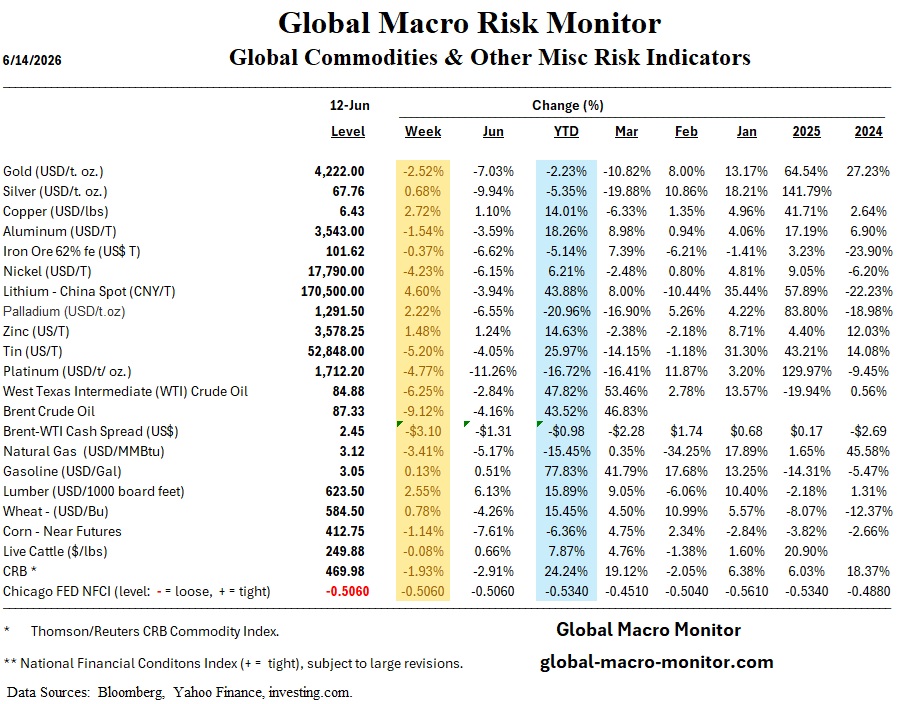

The market’s message last week was unambiguous: geopolitical tail risk gets sold, not bought. Trump declared the US-Iran ceasefire over, both sides exchanged attacks in the Strait of Hormuz, the VIX kissed 19 Wednesday — and the S&P 500 still closed the week up 1.23% at a three-week high, with VIX back to 15.25. As long as WTI stays subdued near $71.41, flows will keep chasing the economy and earnings, not Tehran.

Rates Are the Real Story

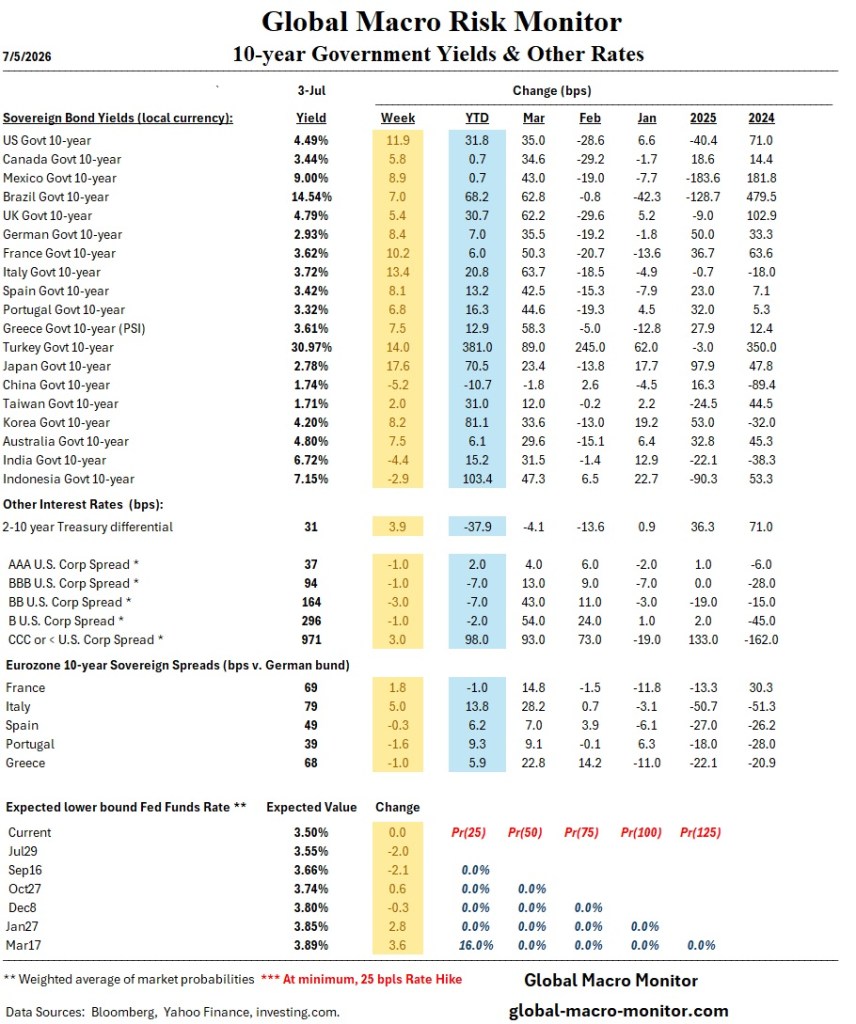

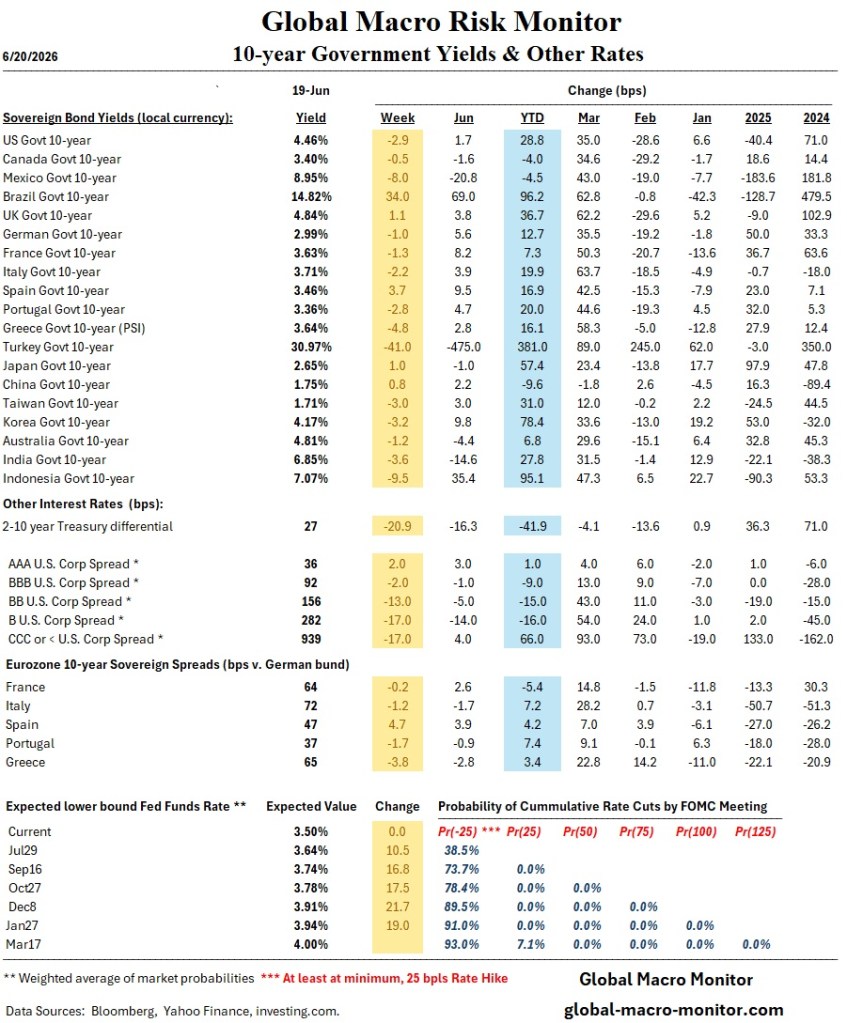

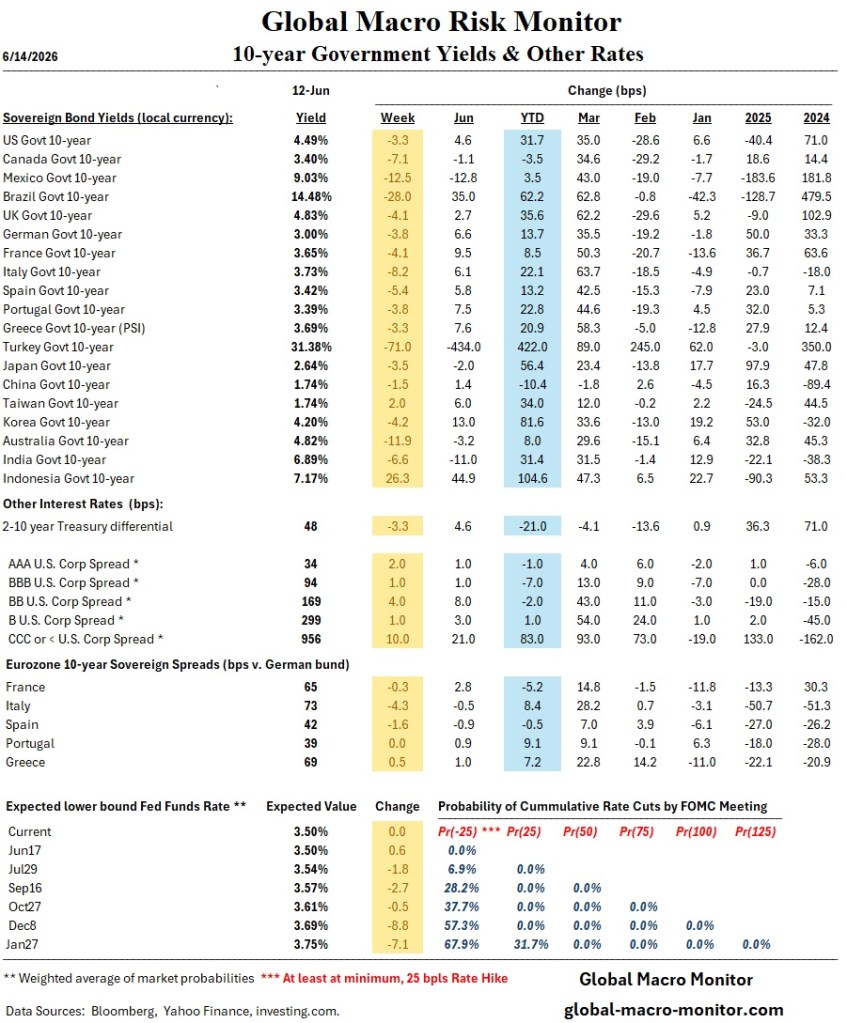

The bond market isn’t as sanguine. Yields rose ~7-8 bps across the curve (2Y 4.20%, 10Y 4.56%, 30Y above 5%), and hike probabilities repriced sharply: July FOMC odds jumped to 31% from 17%, September to 84% from 61%. The June minutes showed a committee split between holding and hiking, with near-unanimity that persistent inflation forces a move. Warsh’s first semiannual testimony Tuesday at 10:00 a.m. ET — hours after June CPI — is the week’s binary event. A hot print plus a hawkish chair leaves little cushion in duration.

Technicals: Constructive, With One Caveat

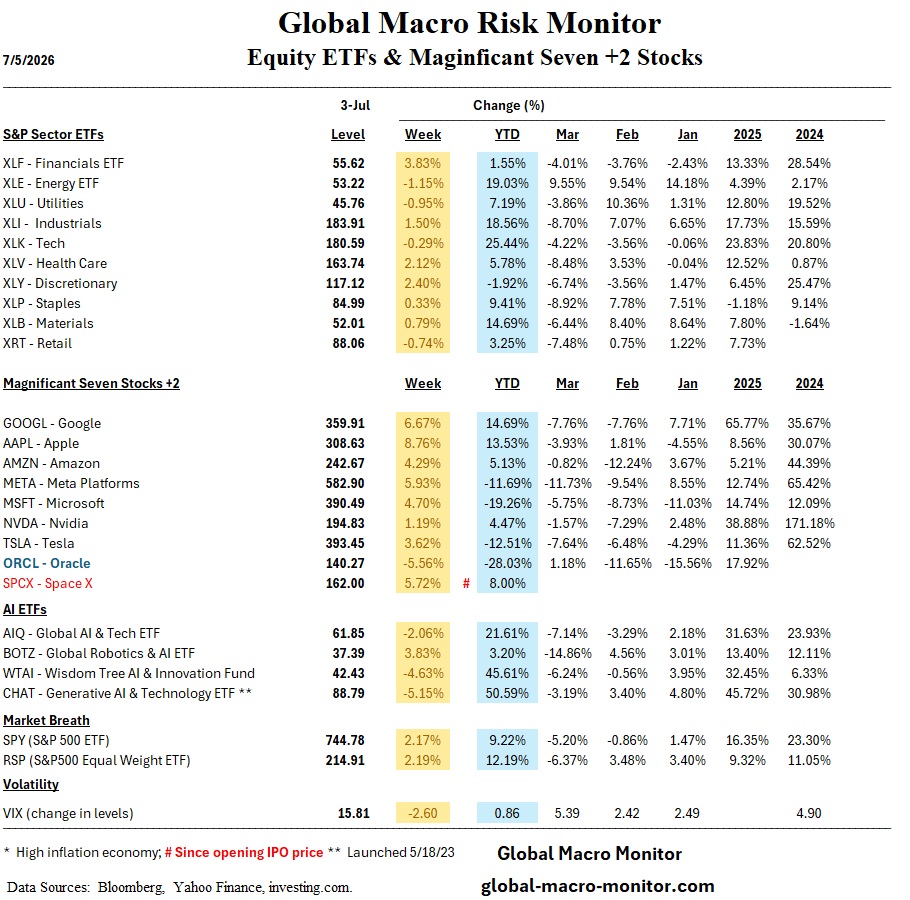

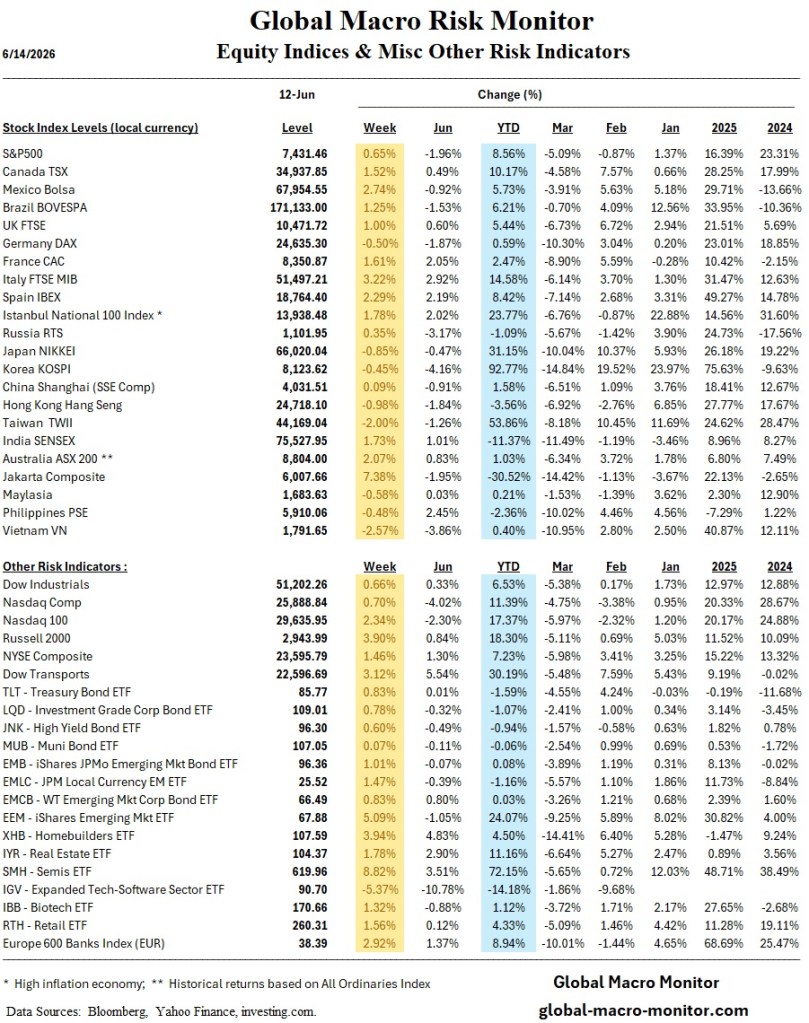

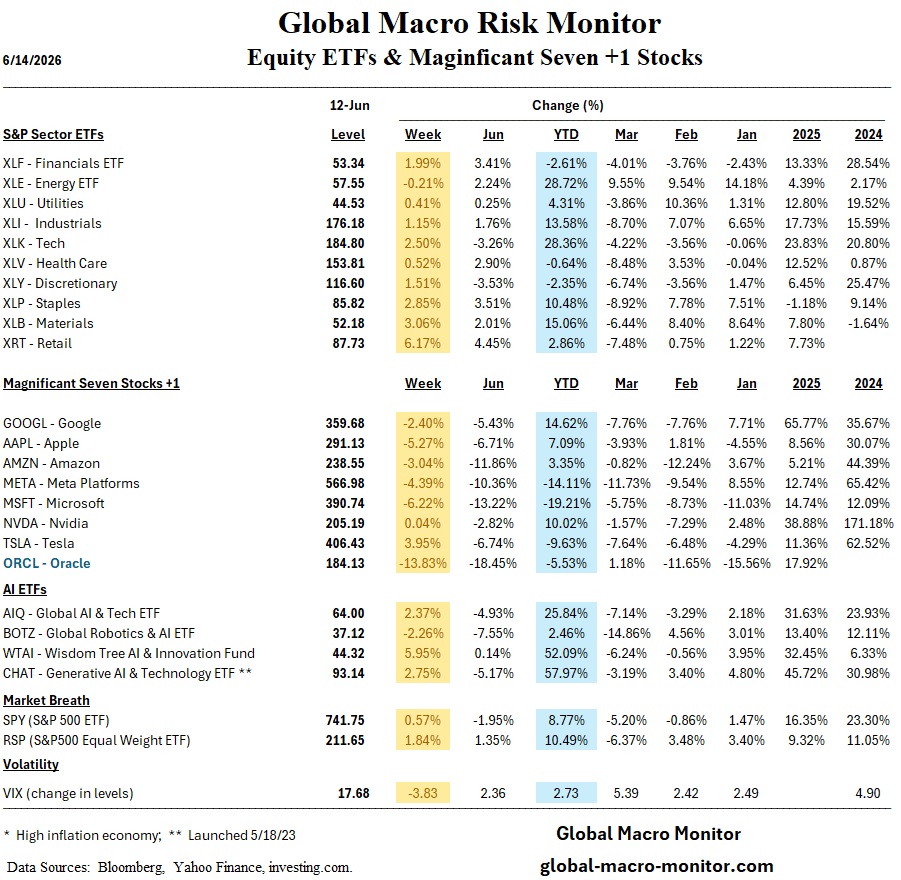

The SPX Equal Weight bounced firmly off its 20-day SMA — textbook uptrend behavior pointing toward new highs. Breadth confirms: 65.3% of SPX members above their 200-day, a four-month high. The caveat is semis. The SOX reclaimed its 50-day SMA after Tuesday’s 4% drop, but the price action is choppy rather than a clean V-bounce. If chips fail here, expect rotation rather than breakdown — but watch confidence.

The Week Ahead

Q2 earnings kick off with FactSet forecasting 23.3% YoY S&P 500 growth. Banks report Tuesday-Wednesday (JPM, GS, BAC, C, WFC, MS, BLK); ASML Wednesday and TSMC Thursday will stress-test the semi rebound. PPI, retail sales, and housing data round out the docket. Crypto desks should also mark August 7: Bitcoin’s BIP 110 soft-fork signaling window opens with only a 55% miner threshold — a governance dispute, but a potential volatility source.

Forecast: Slightly Bullish, with Higher Volatility. The risks to that call: an oil spike, or a hawkish Warsh pushing yields through the equity market’s pain threshold.

God help us. The godless Commies are on the march!

New York City has adopted a new rule that bans companies from using deceptive subscriptions to trap customers into paying for gym memberships, streaming services and other recurring charges, the city’s consumer protection office said.

The new rule, which will start on 1 October, promises hefty fines and aggressive enforcement for violators. Companies that do not provide a simple way to cancel could pay $525 per user subscription, back fees and additional fines. – The Guardian

This graphic ranks the world’s most valuable unicorn companies — private firms commanding valuations of $1 billion or more, without ever answering to public markets.

Markets Navigate a Hawkish Fed Surprise as Asia Surges on AI Wave

Week Ending June 19, 2026

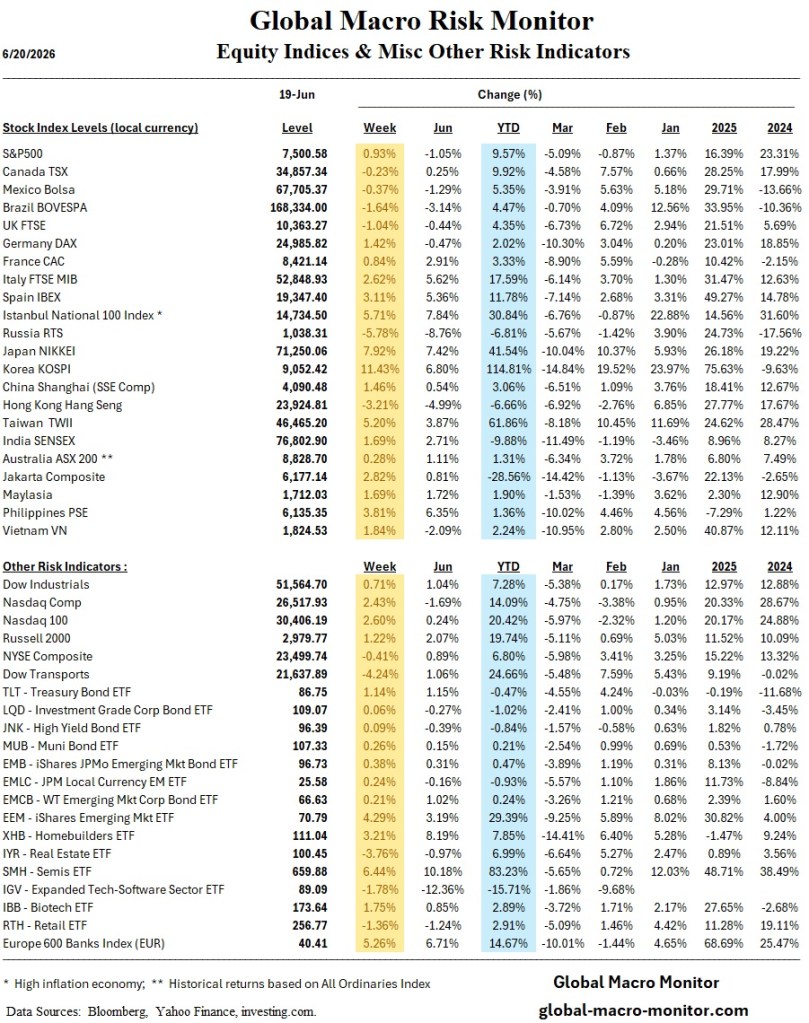

Markets delivered a split verdict this week — a resurgent Asia riding the AI/semiconductor wave higher, while Wall Street grappled with a Fed that just reminded investors it still has a trigger finger.

The Fed Drops the Hawk

The week’s defining event was Kevin Warsh’s first FOMC meeting as Fed Chair, and he wasted no time establishing his credentials as an inflation hawk. Rates were held steady at 3.50–3.75%, but that was the last dovish thing about Wednesday afternoon. The updated dot plot was a gut-punch: nine of 18 officials penciled in at least one rate hike in 2026, with six projecting two or more. Warsh declared price stability the committee’s “North Star” — strong, unanimous, and unambiguous. Translation: the Fed’s easing narrative is dead.

The market reaction was swift. The 2-year Treasury yield spiked 15 basis points, briefly touching a 52-week high of 4.21%. The S&P 500 shed roughly 1.4% and the Nasdaq dropped 1.5% on Wednesday, though dip buyers salvaged the week by Thursday’s close.

The rate market is now doing the math. The probability of a July hike has jumped to 40%, and markets are pricing a 90% chance of at least one hike by December. This is a seismic shift from just two weeks ago, when a 2027 rate hike felt like a stretch.

Warsh also buried forward guidance — he stated it’s no longer suited to the current policy environment. Buckle up. Every data release now matters.

Asia Rips; Semiconductors Lead the Charge

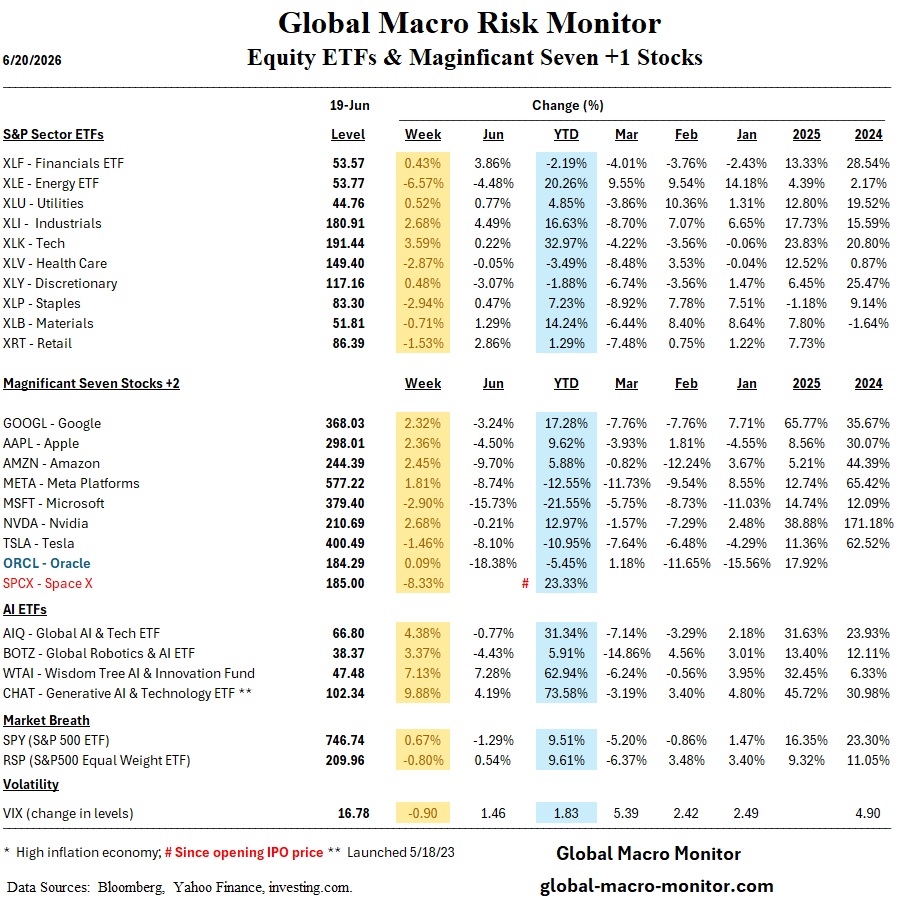

While Washington rattled nerves, Asia was ripping. Japan’s Nikkei surged 7.6% on the week, hitting fresh all-time highs, with semiconductor equipment and AI-linked tech stocks leading the charge. Korea exploded over 11%, powered by the global semiconductor rally. The PHLX Semiconductor Index (SOX) also notched fresh all-time highs stateside, and AI names broadly outperformed. The AI infrastructure buildout theme remains firmly in its expansionary phase — compute demand still outstrips supply, and the market is rewarding that scarcity aggressively.

Geopolitics Provides a Tailwind

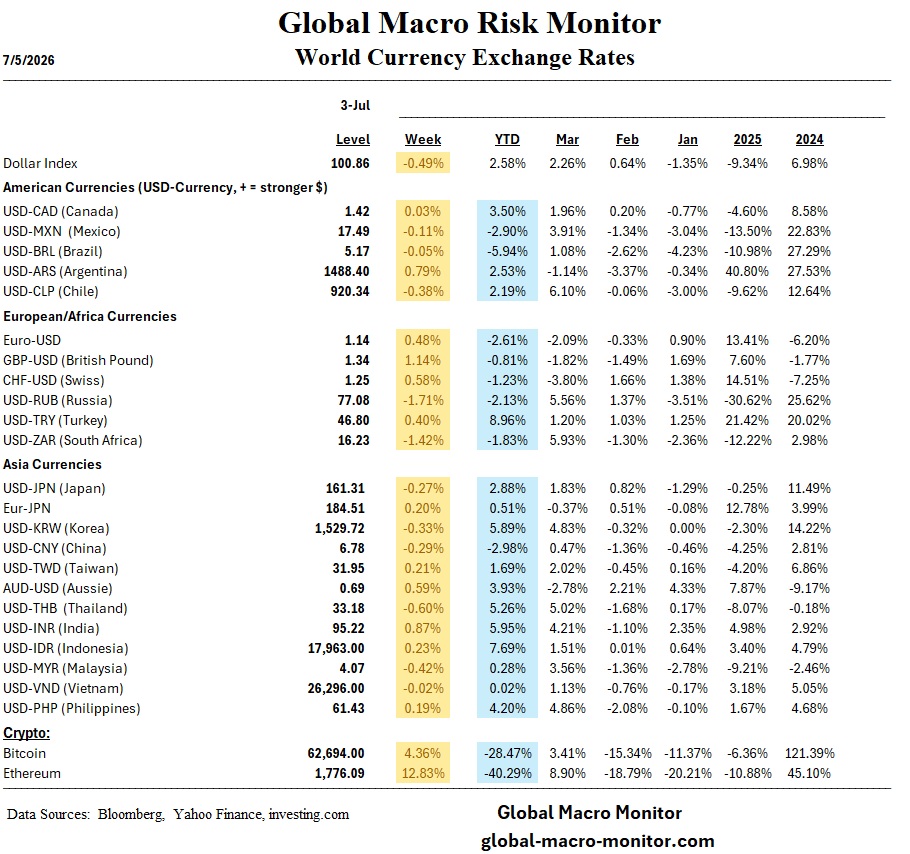

A U.S.-Iran memorandum of understanding, clearing a path to reopen the Strait of Hormuz, sparked a sharp Monday rally and sent oil prices tumbling toward $75/barrel — down nearly 40% from conflict peaks. Lower energy prices provided some inflation relief, though the hawkish Fed quickly overshadowed that narrative.

The Bottom Line

The bull market’s two pillars — 20%-plus earnings growth and AI infrastructure spending — remain intact. But the Fed has drawn a line. With rate hike odds surging and Warsh signaling data-dependency without a policy roadmap, volatility is the price of admission going forward. Asia’s momentum is real, AI is real — but so is the Fed.

Watch the PCE report Thursday and Micron’s earnings next Wednesday. Both could move markets significantly.

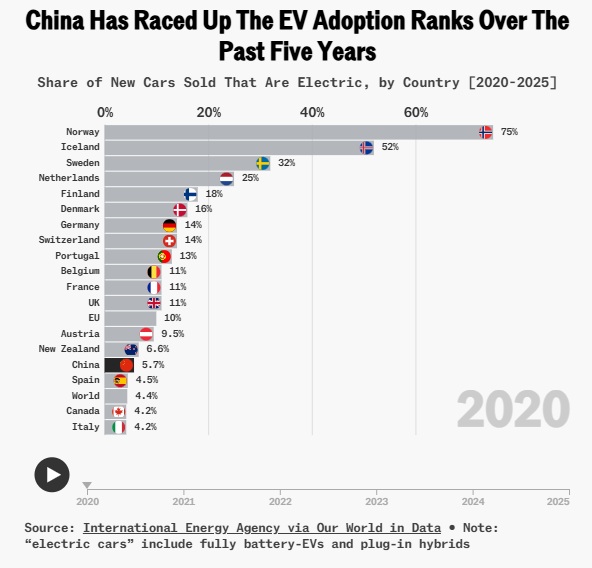

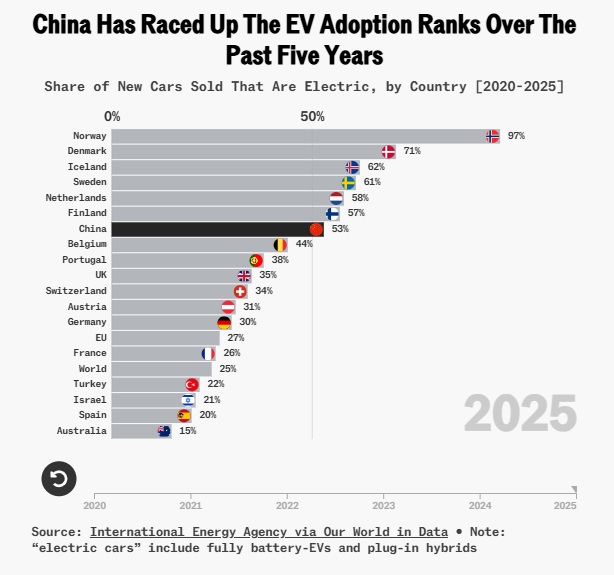

BYD’s Stella Li projects China’s EV market share could rapidly approach 80% of new car sales.

China’s EV penetration jumped from 6% of new car sales in 2020 to 53% in 2025.

China accounted for 60% of global EV sales and over half of the global EV sales increase in 2025.

China’s EV exports rose 78% year-over-year in Q1, with BYD’s European registrations up 115% in April (vs. Tesla’s 47%).

US EV adoption remains around just 10% of new car sales, hampered by weak policy support and expired tax credits.

China’s electric vehicle market is approaching a structural threshold that international economists and portfolio managers should be watching closely. BYD Executive VP Stella Li recently told CNBC that China’s EV penetration could “very quickly” approach 80% of new car sales, building on a base that the IEA describes as having grown at an extraordinarily rapid pace over the past five years.

The trajectory is striking. In 2020, electric cars accounted for just 6% of new car sales in China; by 2025, that share had surged to 53%. For context, that’s a near-tenfold increase in five years — a pace of structural transformation rarely seen in any major economy’s transportation sector, let alone the world’s largest auto market.

China’s dominance isn’t confined to its domestic market. The country accounted for six out of every ten EVs sold globally in 2025, and more than half of the entire global increase in EV sales that year. This single data point underscores why China effectively sets the tempo for the global EV supply chain — from battery materials to charging infrastructure standards.

What’s most relevant for international economists is the export dimension. China’s EV exports surged 78% year-over-year in the first quarter, while BYD’s new car registrations in Europe jumped 115% in April compared to a year earlier, more than double Tesla’s 47% growth in the same market. This export acceleration arrives even as domestic demand growth wobbled slightly after a trade-in subsidy program was temporarily paused, suggesting Chinese automakers are increasingly looking outward to absorb excess production capacity, a dynamic with direct implications for trade tensions, tariff policy, and industrial competitiveness in Europe and beyond.

The contrast with the US is stark. Electric cars still represent only around 10% of new car sales in the US, a market under pressure from weaker policy support, expired federal tax credits, and limited access to cheaper Chinese models.

For investors and policymakers, the takeaway is twofold: China’s EV ecosystem, from BYD to battery suppliers to charging networks, is compounding advantages that will be difficult for competitors to close, and the export wave now hitting Europe will likely intensify debates over tariffs, industrial policy, and “de-risking” strategies. The widening gap between China’s adoption curve and America’s stagnant one also raises longer-term questions about competitiveness in a sector increasingly central to manufacturing employment and energy policy on both sides of the Pacific.

The global EV race has left the starting gate and America’s still checking its tire pressure on a horse-drawn cart.

We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.

We anticipate monitor and comment on market-moving global economic and geopolitical issues. No dark side brooding, no wanting the world to end, no political rants. Traders, investors, policymakers, or market observers can’t afford to ignore us. In one word, perspicacity.