-

In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.

-

Join 1,198 other subscribers

Contribute To GMM

Categories

- 3D Printing

- Agriculture

- AI

- Algos

- Apple

- Automation

- Banking

- BFTP

- Bitcoin

- Black Swan Watch

- Bonds

- Brazil

- Brexit

- BRICs

- Budget Deficit

- Capital Flows

- Cartoon of the Day

- Cashless Society

- Chart of the Day

- Charts

- China

- Clean Tech

- Climate Change

- Coach C

- Commodities

- Coronavirus

- COVID

- Credit

- Crude Oil

- Currency

- Cyprus

- Daily Risk Monitor

- Day In History

- Debt

- Demographics

- Disinflaton

- Dollar

- Earnings

- ECB

- Economics

- Economist

- Egypt

- Electric Vehicles

- Emerging Markets

- Employment

- Energy

- Environment

- Equities

- Equity

- Euro

- Eurozone Sovereign Spreads

- Exchange Rates

- Fed

- Finance and the Good Society

- FinTech

- Fiscal Cliff Monitor

- Fiscal Policy

- Food Prices

- France

- Futurist

- Game Theory

- General Interest

- Geopolitical

- Geopolitics

- German Bund

- Germany

- Global Macro Watch

- Global Reset

- Global Risk Monitor

- Global Stock Performance

- Global Trend Indicators

- Gold

- Greece

- Healthcare

- Heat Map

- Hedge Funds

- Housing

- Human Interest

- Immigration

- Impeachment

- India

- Inequality

- Inflation/Deflation

- Infographics

- Innovation

- Institutional Investors

- Interest Rate Monitor

- Interest Rates

- Interviews

- Italian Yields

- Italy

- Japan

- Jobs

- Lectures

- Macro Notes from Conference Calls

- Manufacturing

- Masters

- Mexico

- Monetary Policy

- Movies

- Muni Bonds

- Muni Market

- Natural Gas

- News

- Nonlinear Thinking

- North Korea

- Overbought Markets

- Picture of the Day

- PIIGS

- PMIs

- Policy

- Politics

- Population

- Populism

- Poverty

- President Trump

- Qunat Strategies

- Quote of the Day

- Quotes

- Rare Earth Elements

- Readership

- Reads

- Real Estate

- Relative Strength Index

- Robert Shiller

- RSIs

- S&P500

- Sector ETF Peformance

- Semiconductor prices

- Semiconductors

- Social Media

- Socialism

- Song for the Week

- Sovereign Debt

- Sovereign Risk

- Spain

- Sports

- State and Local Government

- Tail Risk

- Technical Analysis

- Technology

- The Big Reset

- The Weekend Read

- This Day In Financial History

- Trade War

- Trades

- Tweet of the Day

- Ugly Chart Contest

- Uncategorized

- US Releases

- Video

- Volatility

- Wages

- Week Ahead

- Week in Review

- Weekend Reads

- Weekly Eurozone Watch

- Whales

-

Recent Posts

Meta

The Story of Money: Why Nixon Ditched the Global Monetary System | FT

Posted in Uncategorized

Leave a comment

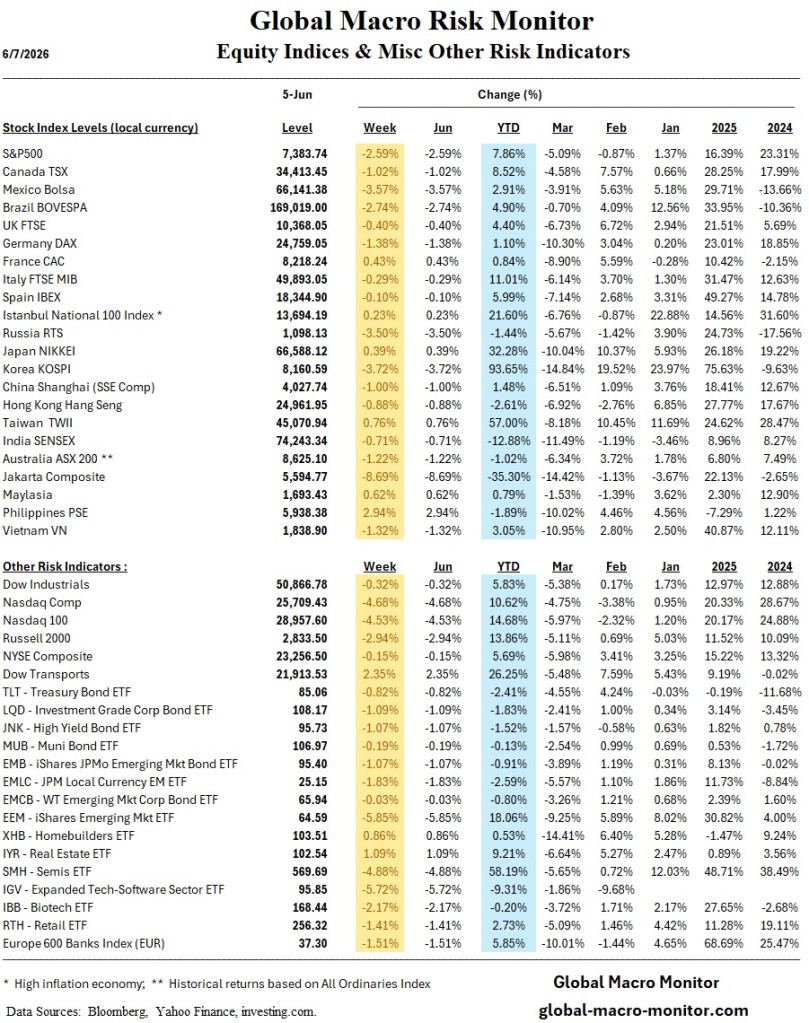

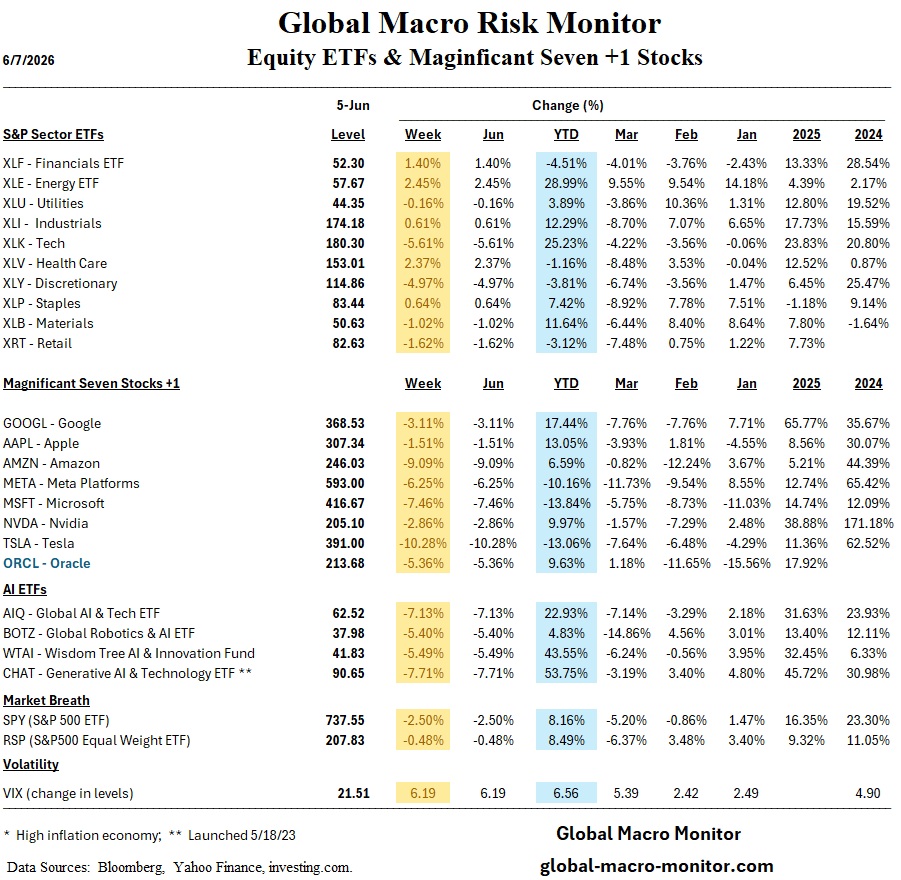

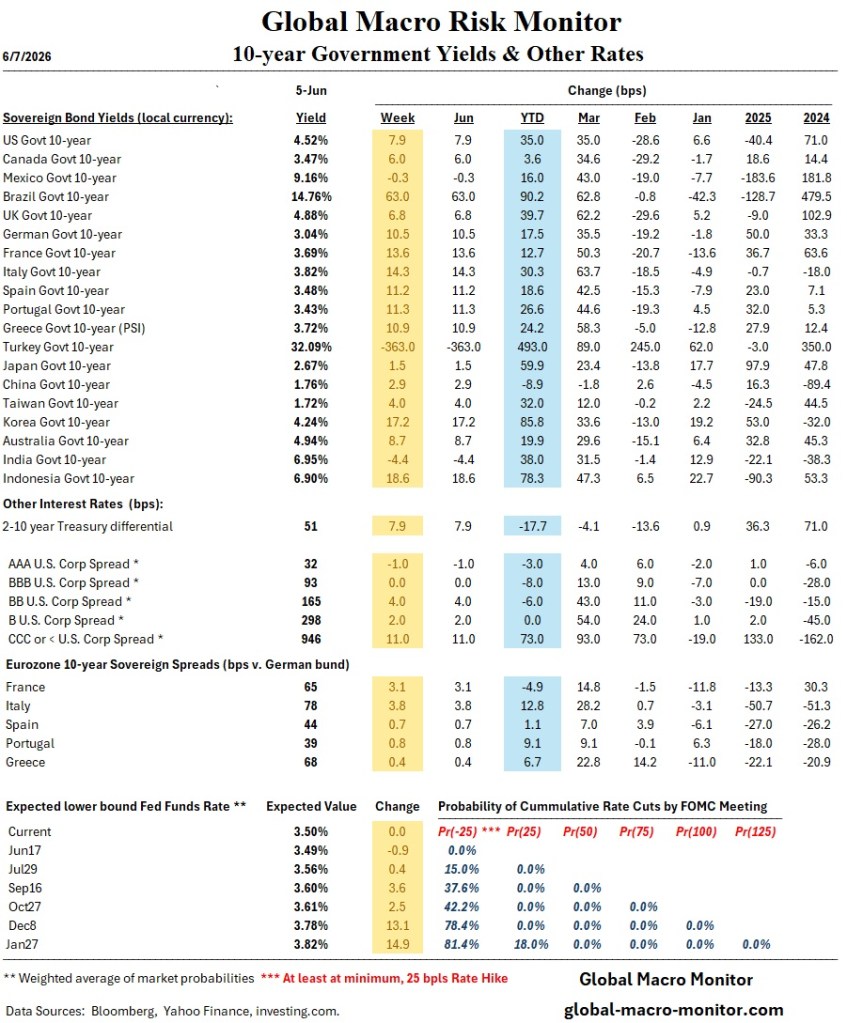

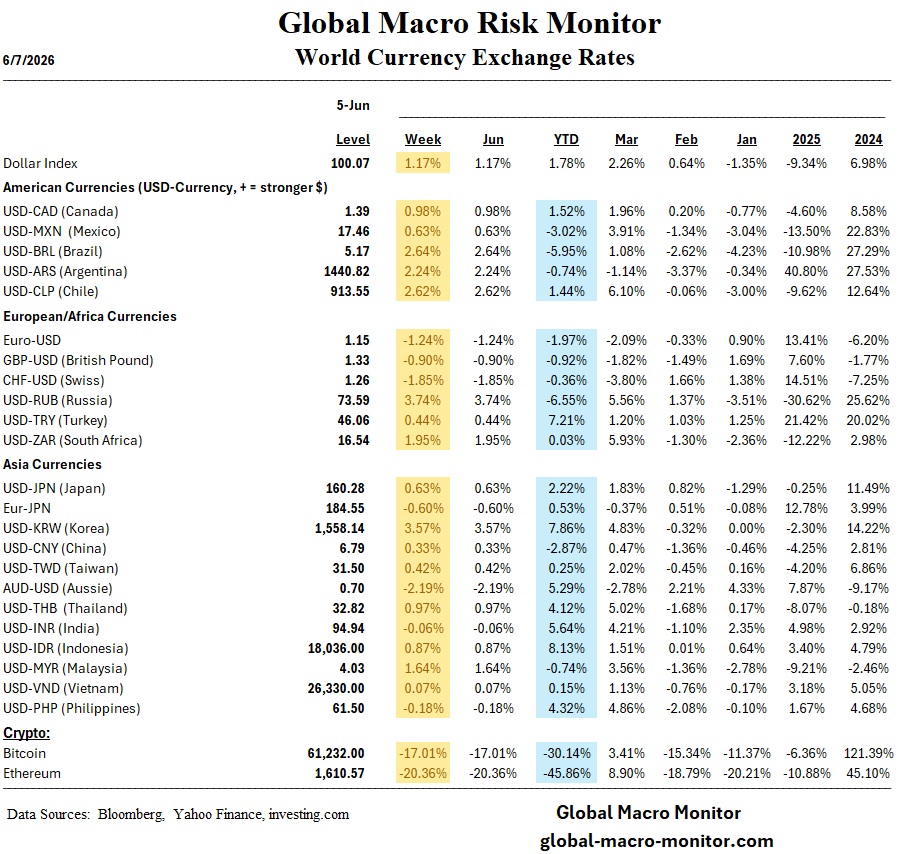

Global Risk Monitor: Week in Review – June 5

Markets in Motion: A Week of Reckoning

Global markets delivered a sobering reminder last week that sentiment can shift fast — and that the era of easy money remains firmly in the rearview mirror.

The sharpest single blow landed on semiconductors. The VanEck Semiconductor ETF (SMH) shed nearly 10% on Friday alone, rattling investors who had leaned heavily into the AI-driven chip trade. Whether this represents a healthy correction or the first crack in a crowded thesis remains the defining question heading into next week.

Bond markets offered little refuge. Global yields marched higher across the board, reinforcing the message that fixed income is repricing for a higher-for-longer world. Traders are now pricing in an 80% probability of a Fed rate hike by December — a figure that, if realized, would continue to squeeze valuations across risk assets.

The dollar, meanwhile, flexed its muscles with a 1% weekly gain — a move with real consequences beyond U.S. borders. The Korean won bore the brunt, weakening sharply and casting a shadow over Korean equities, which face the familiar double-bind of a strong dollar and the speed wobble in semiconductor equities.

Finally, Bitcoin’s 20% weekly plunge underscored crypto’s persistent vulnerability to macro headwinds. Weekend stabilization offered some relief, but it does little to restore confidence in digital assets as a credible safe haven.

Adding to the pressure, a wave of mega IPOs is poised to flood the market in the coming weeks. Large new listings force institutional investors to raise cash by trimming existing positions, creating a mechanical headwind for broader equity prices. With risk appetite already fragile, the timing is particularly uncomfortable — heavy supply rarely finds a warm reception when the macro backdrop is tightening.

The throughline? Risk is being repriced — methodically, and across asset classes. Investors who positioned for a dovish pivot may find the fourth quarter considerably less forgiving than they hoped.

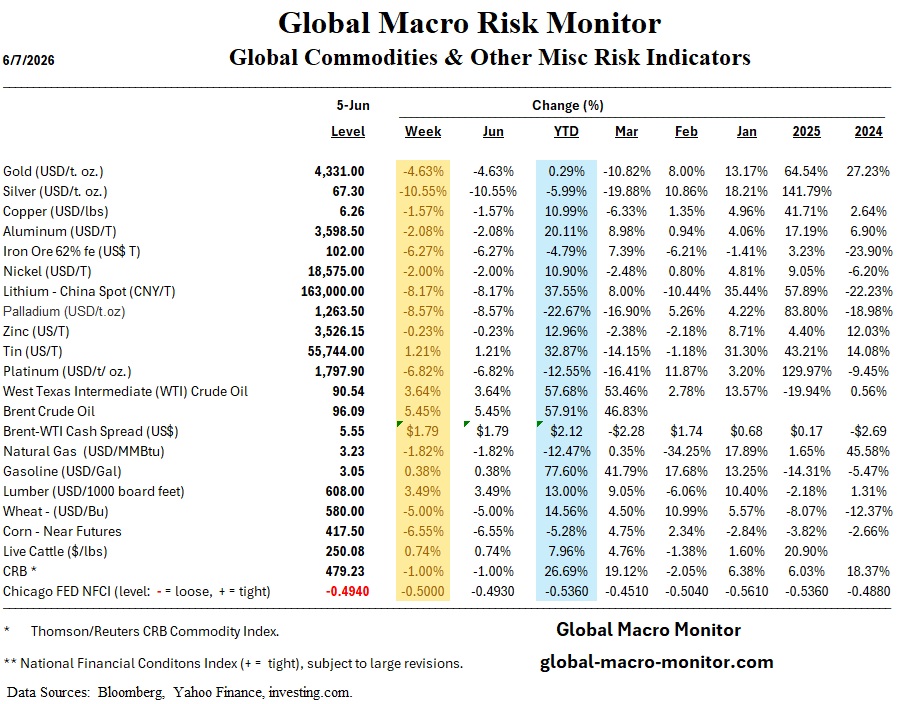

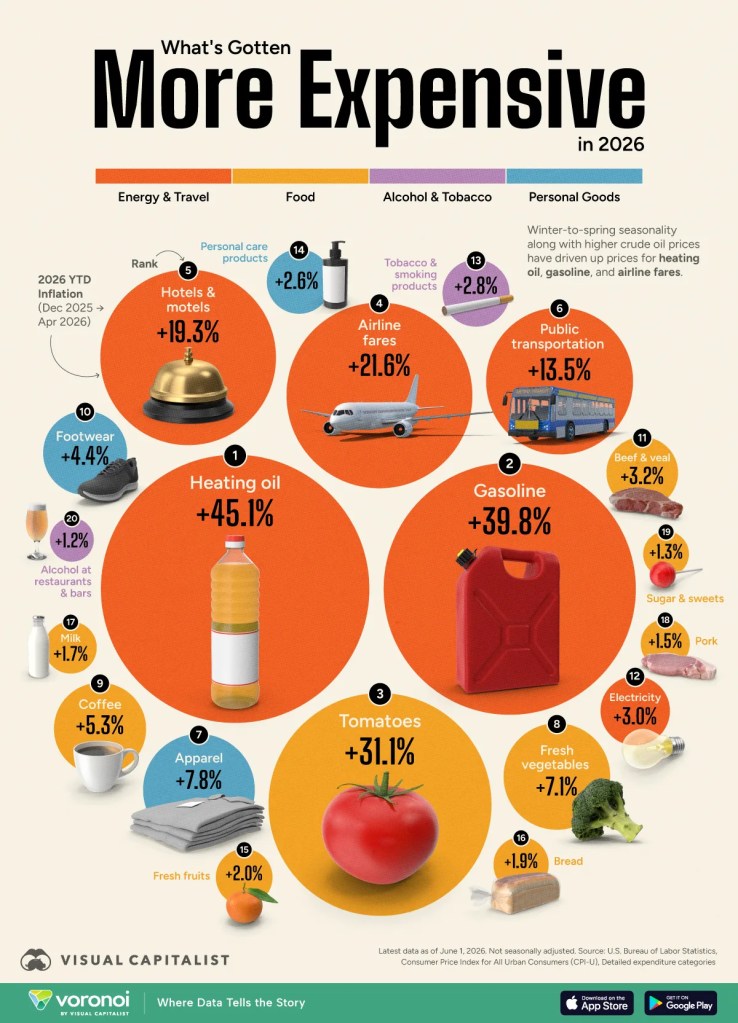

Pain at the Pump, Plate, and Plane: Breaking Down 2026’s Price Spikes

Posted in Uncategorized

Leave a comment

D-Day’s Must-View Movie: Pressure

The success of D-Day, 1944 (originally planned for June 5th) came down to a weatherman getting it right.

Ode to the Weatherman

“When I’m right, no one remembers; When I’m wrong, no one forgets.”

Posted in Uncategorized

Leave a comment

Of Course There’s No Inflation

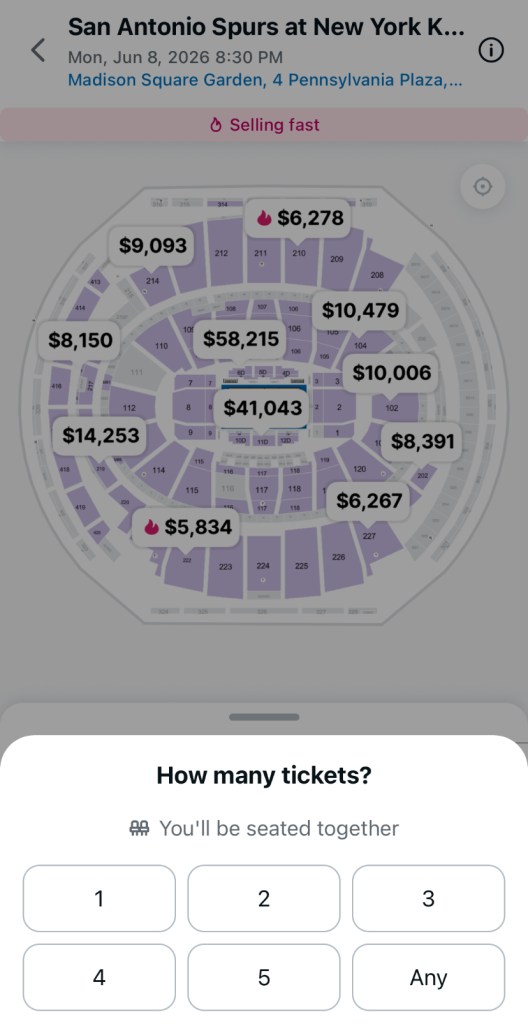

Classic stock market wealth effect. I’d bet the family jewels that if the S&P 500 was, say at 5,000, ticket prices would be one third of these prices. I am conflicted. Big Knicks fan during my Wall Street days during the Patrick Ewing era, but they broke my heart. I love Wemby, however.

Hat tip: C. Bless

Posted in Uncategorized

1 Comment

The Medicaid Surge: Economic Drivers, the Unwinding, and the OBBBA Retrenchment

Ten Key Takeaways:

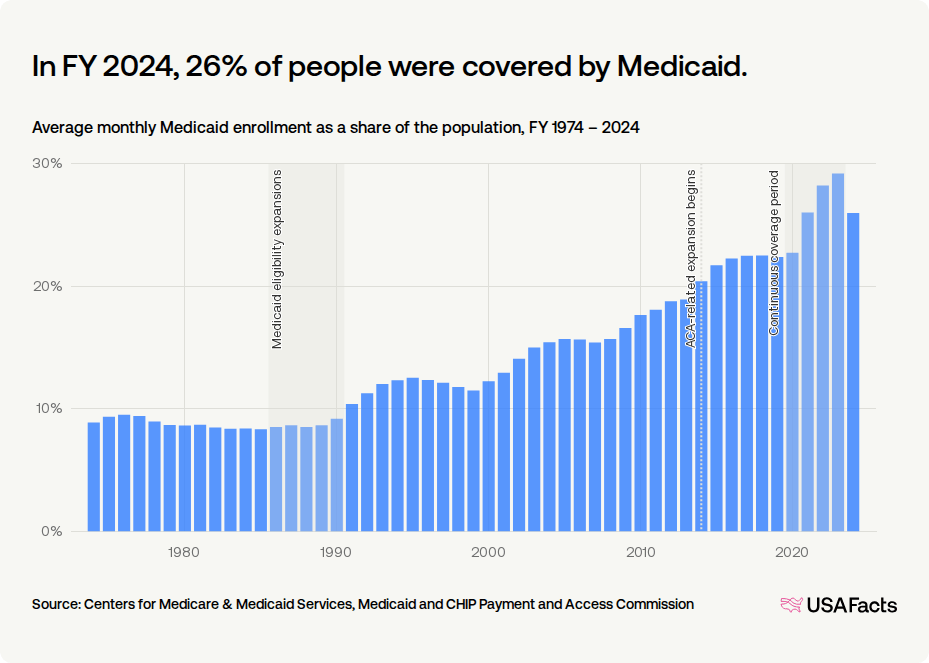

- Record Enrollment: Medicaid peaked at 26% of the U.S. population (88.2 million people) in FY 2024, cementing its status as the nation’s largest insurer.

- Decoupling Welfare: Structural growth began when late 1980s mandates disconnected healthcare eligibility from cash public assistance programs.

- Income Standard: The ACA replaced demographic restrictions with a standardized, income-based limit up to 138% FPL.

- Welcome-Mat Effect: Simplified enrollment processes prompted millions of previously eligible but unenrolled individuals to sign up.

- Continuous Enrollment: The 2020 FFCRA barred states from disenrolling anyone during the pandemic, stabilizing national coverage.

- Procedural Unwinding: The post-pandemic “unwinding” stripped coverage from 20.7 million people, though 68.7% of these were due to procedural paperwork errors.

- The OBBBA Shock: The newly enacted One Big Beautiful Bill Act of 2025 represents the largest-ever cut to basic needs programs, slashing over $1 trillion in federal healthcare spending and leading to over 10 million more uninsured Americans.

- Mandatory Work Requirements: Starting in 2027, able-bodied adults in the expansion population must meet an 80-hour monthly work or community service mandate, which is expected to disenroll over 5 million people.

- Administrative Barriers: The OBBBA doubles the frequency of eligibility redeterminations to every six months for the expansion population, threatening to disenroll an additional 700,000 people due to paperwork.

- State Funding Restrictions: Capping provider taxes from 6% to 3.5% under the new law severely restricts state fiscal capacity, creating deep budgetary pressures.

Our analysis in our recent post, “America’s Fiscal Mirage: Tariff Sugar Rush, Structural Hangover,” highlights that while recent deficit figures may appear to show a very slight improvement, they mask a deeper, persistent fiscal fragility driven by structural imbalances rather than sustainable reform. Despite temporary boosts from tariff revenue, many of which are now under threat from recent legal reversals, the long-term outlook remains grim, as mandatory spending continues to operate largely on autopilot. Central to this challenge is the sheer scale of entitlement costs; for instance, Medicaid spending alone now accounts for approximately 15 percent of total U.S. government outlays, creating a rigid spending floor that complicates any meaningful attempt to curb the nation’s mounting debt trajectory.

The structural landscape of American healthcare has undergone a seismic shift. As highlighted in the historical data, a monthly average of 26% of the U.S. population was covered by Medicaid in fiscal year (FY) 2024. For a program created in 1965 to act as a highly restrictive safety net tied strictly to cash welfare , this represents a fundamental social and fiscal transformation.

As an economist analyzing this trajectory, it is clear that this dramatic enrollment surge was driven by compounding policy waves visible in the historical trends:

1. Welfare Decoupling (The 1980s & 90s Spikes)

Originally, Medicaid required enrollees to receive cash welfare assistance. Congressional mandates during the “Medicaid eligibility expansions” of the late 1980s and early 1990s decoupled these requirements, expanding eligibility to low-income pregnant women and children regardless of welfare status. This separation was finalized by the 1996 welfare reform and the 1997 launch of the Children’s Health Insurance Program (CHIP).

2. The ACA’s Standardized Eligibility (2014)

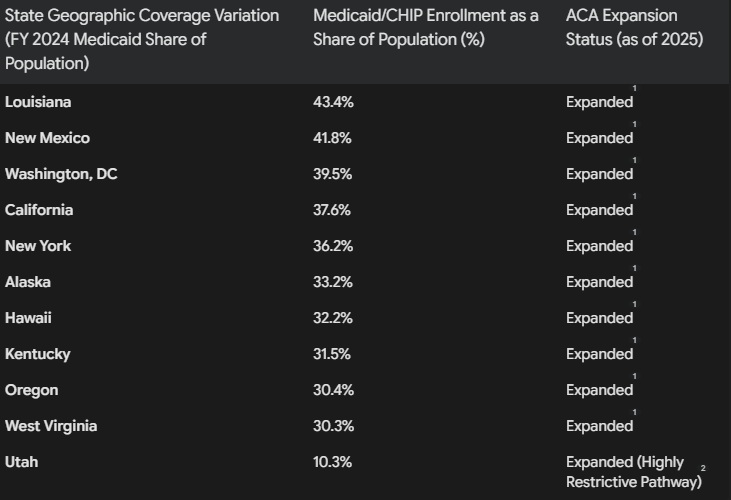

The Affordable Care Act of 2010 fundamentally modernized Medicaid by establishing a standardized, income-based model. In the states that adopted expansion, coverage opened to all nonelderly adults earning up to 138% of the Federal Poverty Level (FPL). This was incentivized by a permanent 90% federal matching rate (FMAP) and triggered a massive “welcome-mat” or “woodwork” effect, enrolling millions of previously eligible but unenrolled individuals.

3. Pandemic Continuous Coverage (2020–2023 Peak)

The most dramatic enrollment acceleration occurred during the COVID-19 pandemic. Under the Families First Coronavirus Response Act (FFCRA) of 2020, states received enhanced FMAP funding in exchange for keeping enrollees continuously covered. By halting annual administrative eligibility checks, this policy eliminated enrollment “churn,” sending rolls to a peak of 94 million by early 2023.

4. The Great Unwinding (Post-Pandemic Correction)

Following the end of the pandemic continuous coverage mandate, states began the massive “unwinding” process, conducting redeterminations that resulted in over 20 million disenrollments—moderating FY 2024 coverage back to 26%. Many individuals were disenrolled for “procedural” reasons—such as failing to return renewal paperwork—rather than for a true loss of financial eligibility.

5. The “Big, Beautiful Bill” and the Retrenchment Era

The historical upward trajectory of Medicaid coverage shown in the chart—where enrollment expanded from a modest 8% in the 1970s to a peak of 26% of the population in FY 2024 —is poised for an unprecedented reversal. On July 4, 2025, the budget reconciliation package colloquially known as the “One Big, Beautiful Bill Act” (OBBBA) was signed into law, enacting the largest-ever cuts to basic needs programs in U.S. history. To fund tax cuts, the legislation is projected to slash federal healthcare spending by over $1 trillion, including $911 billion in direct Medicaid cuts, resulting in an estimated 10 million fewer insured Americans over the next decade.

The single largest driver of this projected contraction is the nationwide implementation of mandatory work and community engagement requirements starting January 1, 2027. Under the OBBBA, non-disabled adults in the ACA expansion group (ages 19-64) must document at least 80 hours of work, community service, or education per month to maintain their coverage. The Congressional Budget Office (CBO) estimates this provision alone will reduce federal outlays by $326 billion over ten years, causing upwards of 5 million people to lose coverage. Furthermore, the law doubles the frequency of administrative checks, forcing these expansion enrollees to undergo eligibility redeterminations every six months rather than annually. This increased paperwork burden is expected to strip coverage from an additional 700,000 eligible individuals. Coupled with a reduction in the Medicaid provider tax cap from 6% to 3.5%—which severely restricts state funding capacity—this law signals a dramatic, policy-driven retrenchment that will sharply bend the historical enrollment curve downward.

Sources:

- USAFacts: Monthly Average Medicaid Enrollment & Population Share.

- Kaiser Family Foundation (KFF): Health Policy 101, Unwinding Tracking, and Reform Overviews.

- Medicaid and CHIP Payment and Access Commission (MACPAC): MACStats & Unwinding Data Brief.

- National Bureau of Economic Research (NBER): Research Papers on ACA Medicaid Expansions & Fiscal Federalism.

- American Medical Association (AMA): Briefings on the One Big Beautiful Bill Act.

- GoodRx & RAND Corporation: Impact analysis of the One Big Beautiful Bill Act.

Presidential Budget Deficits

We are reposting the Appendix added and updated to yesterday’s post, America’s Fiscal Mirage: Tariff Sugar Rush, Structural Hangover. We thought it important as President Trump has formally requested a historic $1.5 trillion national defense budget for Fiscal Year 2027. This represents a massive 44% increase over the current year’s base funding levels, marking the largest year-over-year military spending hike in post-World War II history. There is no doubt the markets will balk at deficit financing this without much higher interest rates, thus more pressure coming to cut spending on Medicare/Medicaid and Social Security programs. The “crowding out” chickens are finally coming home to roost.

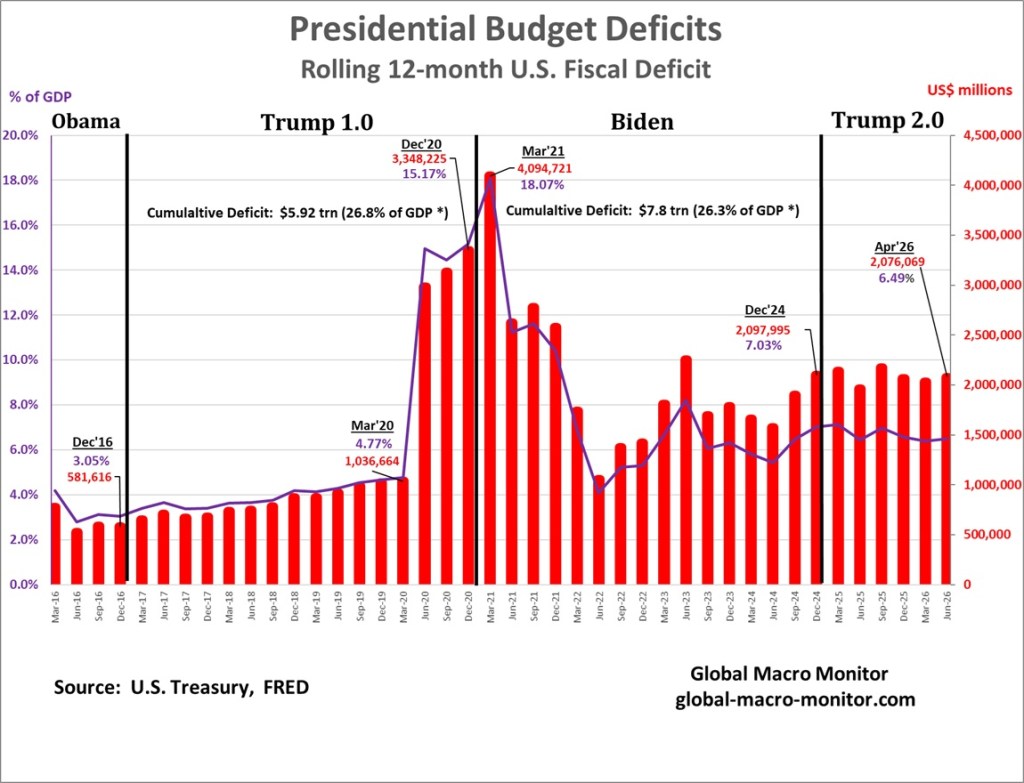

The conventional political narrative holds that Biden blew up the federal deficit. The data tell a more complicated story, and one that will surprise many.

Presdient Obama left office with the rolling 12-month deficit at a relatively disciplined 3% of GDP. Trump 1.0 then widened the structural deficit to nearly 5% of GDP by March 2020, before the COVID pandemic began to spread in the United States. The pandemic did the rest: emergency spending exploded the deficit to 15.2% of GDP by December 2020. What is rarely acknowledged is that Trump handed Biden a deficit already running at 15% of GDP — among the largest in U.S. peacetime history. Biden’s early months pushed it marginally higher to a peak of 18.1% by March 2021, but the trajectory was largely baked in before the inauguration.

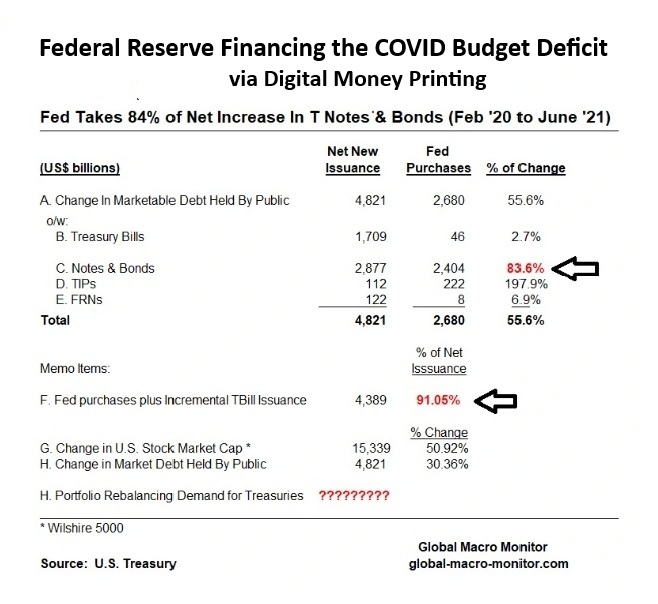

The fiscal shock was too large for private bond markets to absorb. The Fed stepped in as the bond and U.S. Treasury debt buyer of last resort, purchasing 83.6% of all net new Treasury notes and bonds issued between February 2020 and June 2021 — funding 91% of net issuance when incremental T-bills are included. That is digital money-printing at scale, and it is the true origin story of post-COVID inflation in both financial assets and goods and services.

(Source: U.S. Treasury, FRED, Global Macro Monitor. Full fiscal scorecard: global-macro-monitor.com)