What a contrast between the current Citi CEO and the former who danced his bank over the edge and right into the Global Financial crisis.

…if you’re looking for signals, they’re everywhere. Treasury yields rose even as equity markets wobbled. The U.S. dollar, typically a safe haven, has weakened at moments when it used to rally. That tells us something deeper is going on, investors aren’t just pricing near-term risks; they’re reevaluating the credibility of long-held certainties. It’s showing up in how capital moves. Pensions and asset managers are tilting more towards Japan, India and parts of Europe. Hedge funds are being selective and didn’t chase the April equity bounce. Sovereign wealth funds are diversifying more aggressively. Hedging against the dollar is now at levels we haven’t seen in years. – Jane Fraser, Citigroup CEO

When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing. – Chuck Prince, Citigroup CEO July 2007

As we suspected in yesterday’s Global Risk Monitor, recent developments confirm a deteriorating trajectory in U.S. trade negotiations. Today’s Financial Times headline underscores the hardening U.S. stance, signaling heightened tariff risks for non-cooperative trade partners. This shift, when viewed alongside Moody’s downgrade of the U.S. sovereign credit rating announced post-market close on Friday, is likely to unsettle investor sentiment and amplify concerns over global economic stability.

Financial markets continued to rebound this week, buoyed by temporary trade de-escalations and looser financial conditions. However, beneath the surface of this rally lies a landscape of historically elevated valuations and persistent uncertainty. Market participants should temper optimism, as the sustainability of recent gains remains highly contingent on volatile policy developments and fragile macroeconomic signals. Nevertheless, it feels like the FOMO crowd wants to challenge the all-time highs made in February.

Euro Banks

European banks, often overlooked in recent years, have delivered an unexpected year-to-date return of 33% in euro terms, with an added 7% benefit from currency movements. Their outperformance, by over 40% relative to NVIDIA, for example, would have been dismissed as implausible and crazy at the start of the year.

Semis

The semiconductor sector led with outsized gains, with its SMH ETF advancing 10% this week and 16% in May. Renewed demand for AI infrastructure and chip exports contributed to this performance. Nonetheless, such sharp movements in high-beta sectors raise concerns about potential overextension, particularly in a market where overall valuations, such as the S&P 500’s forward price-to-earnings ratio of 22, already stand at historically elevated levels.

Fed Cut Pushed Out

The Federal Reserve’s decision to delay rate cuts has pushed out market expectations for the first cut at the September 17 FOMC meeting, with the second cut expected in December. Despite recent inflation readings coming in below expectations, the Fed appears unwilling to declare victory prematurely. Treasury markets reflected this prudence: the 10-year yield breached 4.5% this week, rising 32 basis points in May alone. While narrowing credit spreads may suggest improved sentiment, they could also reflect a mispricing of lingering risks.

Trade Risk Still On the Table

Complicating the macro outlook further are renewed trade tensions. President Trump announced that the U.S. will soon issue letters unilaterally setting new tariff rates for hundreds of countries, citing the impracticality of individualized negotiations. Markets may interpret this as a signal that the negotiation process is proving more contentious than anticipated. This blunt and unilateral approach injects further uncertainty into the global trade environment and could prove destabilizing if retaliatory measures follow. There is no question tariffs are headed higher from already historically elevated rates.

Japan’s position in the ongoing trade saga is illustrative of broader tensions. Facing domestic political challenges, Tokyo has hardened its stance, resisting any agreement that fails to deliver meaningful relief on the 25% U.S. auto tariff. While this impasse may delay resolution, it also reflects a pragmatic effort to avoid structurally imbalanced outcomes. The Japanese government is seeking to protect critical industries while engaging in high-stakes diplomacy with a U.S. administration increasingly focused on unilateral action.

Markets have moved on from the tariff debacle, but we say not so fast.

Keep this on your radar, folks.

Germany and Spain Über Alles

European equity markets, particularly in Germany and Spain, are among the stronger performers year-to-date, aided by robust industrial output and a 7% currency gain for unhedged foreign investors. However, the durability of this momentum is far from assured, especially as broader global demand remains uneven and subject to policy disruption.

Crude Oil and Gasoline Divergence

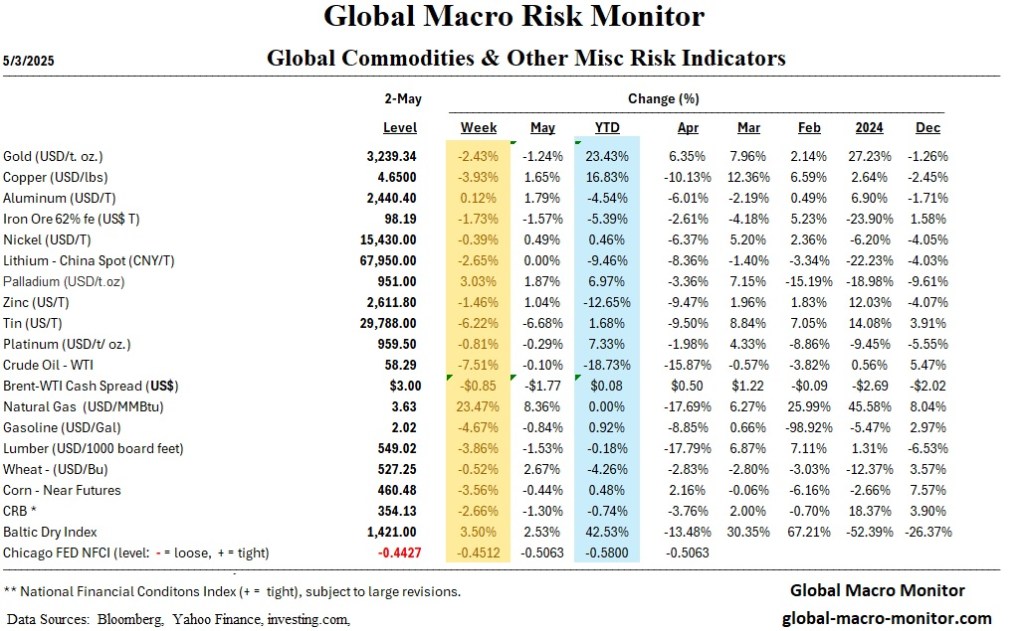

Commodities present a mixed picture: crude oil prices have fallen 13% year-to-date, while wholesale gasoline prices climbed 7%, reflecting possible supply chain inefficiencies or seasonal demand effects. These divergences add complexity to inflation forecasts, which remain central to monetary policy decisions. Furthermore, the political dividend of a drop in crude oil prices is almost completely cannibalized by the surprising increase in gas prices.

Apple and Consumer Sentiment

Apple saw renewed investor interest, a potentially positive sign for consumer tech sentiment. Yet, such gains may also reflect momentum-driven positioning rather than fundamental improvement, particularly as consumer sentiment remains weak. The University of Michigan’s May index fell for the fifth consecutive month, with inflation expectations climbing—further highlighting the disconnect between soft data and asset pricing.

Easing Financial Conditions

Although financial conditions eased significantly in May, as reported by the Chicago Fed’s NFCI, the breadth and quality of this easing merit scrutiny. Much of the recent rally has been driven by multiple expansion rather than earnings growth, suggesting vulnerability if macro data or geopolitical developments disappoint.

In sum, while financial markets have posted strong returns in May, this strength masks underlying fragility. With valuations stretched, geopolitical risks intensifying, and macroeconomic signals mixed, a neutral to slightly bearish outlook is warranted. Investors should remain vigilant, as the path forward is likely to be shaped more by volatility and policy missteps than by sustained fundamental momentum. That said, the momentum whores (of which, we are one at times) have taken control of the markets and it wouldn’t be a surprise to see a continued move to the old highs.

Markets

U.S. Market Analysis

Markets Rise on Trade Optimism U.S. equities rebounded sharply as the White House and Beijing reached a 90-day tariff suspension, with U.S. tariffs on Chinese goods lowered from 145% to 30%, and China reducing its tariffs from 125% to 10%. This temporary reprieve lifted risk sentiment and propelled major indices upward:

Nasdaq Composite: +7.15%

S&P 500: +5.27%

Dow Jones Industrial Average: +3.41%

Russell 2000: +4.5%, still down 5.3% YTD

Investor Sentiment Remains Cautiously Bullish While the rally broke key technical levels (e.g., Nasdaq and S&P 500 moving above their 200-day SMAs), gains were underpinned by short covering, underexposure, and tactical positioning rather than fundamentals. Despite these technical wins, market breadth remains uneven and valuations stretched, with the S&P 500 trading at a 22x forward P/E—above historical norms.

Tariff Volatility Still a Risk Although trade tensions with China have temporarily eased, no long-term agreement has been reached. The path of tariffs remains fluid, and uncertainty continues to weigh on capital expenditure and production decisions, particularly among small businesses and manufacturers.

Global Market Analysis

Europe Responds with Diplomacy European stocks followed U.S. markets higher. Germany’s DAX (+1.14%), France’s CAC 40 (+1.85%), and Italy’s FTSE MIB (+3.27%) rose as optimism grew around renewed trade talks. Germany’s industrial output (+3.1% in March) and a record eurozone trade surplus (EUR 36.8B) offered support.

Germany Seeks Trade Reset Calls for a structured, zero-tariff trade framework by German officials aim to restore competitiveness and regulatory alignment. This reflects Europe’s attempt to play a stabilizing role in global trade while avoiding direct confrontation.

China Not Yet Aligned Chinese stocks rose modestly (CSI 300 +1.12%, Hang Seng +2.09%) as the trade reprieve met nearly all of Beijing’s demands. However, the easing of tensions also reduced pressure on Beijing to announce major stimulus, tempering equity gains.

Economics

U.S. Economic Overview

Tariff Intentions Still Unclear Markets remain uncertain whether tariff policy is aimed at reshoring supply chains, extracting concessions, or supporting fiscal goals. With the pause in place, attention has shifted to whether similar concessions will be made with the EU or Japan.

No Formal Progress with China Despite the 90-day pause, the deal lacks structural reform commitments. Consumers and businesses remain wary, as the effective tariff level of 30% is still significantly elevated relative to pre-April rates.

Price Pressures on Horizon April’s CPI rose 2.3% YoY and core CPI held at 2.8%, both below expectations. PPI fell 0.5% MoM, driven by margin compression. However, forward inflation expectations surged:

1-year inflation expectations: 7.3% (highest since 1981)

5–10-year expectations: 4.6% (highest since 1991) Consumers increasingly cite tariffs as a dominant economic concern.

Retail Sales and Sentiment Retail sales slowed to +0.1% MoM, with weakness in autos, sporting goods, and apparel. Sentiment plunged to the second-lowest level on record (University of Michigan Index: 50.8), highlighting deep consumer unease.

Global Economic Overview

Germany Advocates Efficiency Through Free Trade Eurozone industrial production rose 2.6% in March, the fastest in two years. Employment also accelerated. Germany argues that tariff reduction could preserve industrial competitiveness and supply chain integration.

Structural Conflict with U.S. Goals U.S. trade policy—focused on tariffs as revenue and domestic stimulus—clashes with Europe’s zero-tariff, rules-based approach. Tensions could rise if no common framework is agreed.

Europe Seeks Stability Before Recession Risk Builds The ECB is in no rush to cut rates, citing improving growth data. However, risks from prolonged trade disputes, particularly if the U.S. targets auto tariffs, remain elevated.

Week Ahead: May 19–23, 2025

Economic Data Releases

Monday, May 19

No major U.S. economic data scheduled.

Tuesday, May 20

Eurozone Inflation (April Final): Final figures for April’s consumer price index (CPI) will be released, providing insight into inflation trends within the Eurozone.

Wednesday, May 21

U.S. Existing Home Sales (April): Data on existing home sales will offer a snapshot of the housing market’s performance during the spring selling season.

Thursday, May 22

U.S. Initial Jobless Claims (Week Ending May 17): Weekly data on unemployment claims will indicate the health of the labor market.

U.S. New Home Sales (April): Figures on new home sales will provide further insight into the housing sector’s condition.

Friday, May 23

U.S. Flash PMI (May): Preliminary Purchasing Managers’ Index data for manufacturing and services sectors will shed light on business activity and economic momentum.

Corporate Earnings Reports

Monday, May 19

Trip.com: Expected to report a nearly 10% decline in earnings per share (EPS) to $0.75, with revenue growth of approximately 17% to $1.92 billion.

Qifu Technology: Anticipated to post a 71% increase in EPS to $1.72, with an 11% rise in revenue to $637 million.

Tuesday, May 20

Home Depot: Analysts expect a 1% decline in EPS and an 8% drop in revenue, reflecting challenges in the home improvement sector.

Gap Inc.: Projected to report a 7% increase in EPS to $0.44, with sales growth of less than 1% to $3.41 billion.

Workday: Expected to announce a 15% rise in EPS to $2.01, with revenue increasing by 11% to $2.22 billion.

Keysight Technologies: Forecasted to report a 17% increase in EPS to $1.65, with a 5% rise in sales to $1.28 billion.

Wednesday, May 21

Target: Anticipated to see a 19% decline in EPS to $1.65, with a 1% decrease in sales to $24.28 billion, amid slowing traffic and tariff concerns.

Lowe’s: Expected to report a 5.5% drop in EPS and a 2% decline in sales, reflecting challenges in the retail sector.

Urban Outfitters: Projected to post a 21% increase in EPS to $0.84, with revenue growth of 7.5% to $1.29 billion.

TJX Companies: Forecasted to report a 5% decline in EPS to $0.91, with a 4.2% increase in revenue to just under $13 billion.

Baidu: Expected to see a 28% decline in EPS to $1.98, with a 1.5% decrease in revenue to $4.3 billion.

XPeng: Anticipated to report a loss of $0.20 per share, with revenue surging 130% to $2.075 billion, driven by strong demand for its Mona 03 model.

Thursday, May 22

Ralph Lauren: Projected to report a 19% increase in EPS, with approximately 5% sales growth for its Q4 results.

Burlington Stores: Expected to announce EPS of $1.42, with revenue rising 7% to $2.65 billion.

BJ’s Wholesale: Anticipated to post an 8% increase in EPS, with a 5.4% rise in revenue.

Analog Devices: Forecasted to report a 21% increase in EPS to $1.70, with sales up 16% to $2.51 billion.

Autodesk: Expected to announce a 15% rise in EPS to $2.15, with a 13% increase in sales to $1.61 billion.

Intuit: Projected to report a 10% increase in EPS to $10.90, with sales rising 12% to $7.56 billion.

Atour Lifestyle: Anticipated to post a 6 cent increase in EPS to $0.32, with 28% revenue growth to $261 million.

Friday, May 23

No major earnings reports scheduled.

Global Events and Developments

May 20–22: G7 Summit in Banff, Canada

Finance ministers and central bankers will convene to discuss global economic challenges, including trade policies and currency volatility.

May 21: Google I/O Conference

Alphabet is expected to unveil new AI-related products and updates, potentially impacting the technology sector.

May 19: UK-EU Summit

A summit between the UK and EU is anticipated to address post-Brexit relations, with potential implications for trade and economic policies.

Global economic growth slowed in April 2025, with the Composite PMI falling to 50.8—its lowest in 17 months and below the long-term average.

Service sector expansion weakened significantly, while manufacturing remained tepid with only slight growth in consumer and intermediate goods.

Major economies like the US, China, and the euro area lost momentum, though India stood out as the only bright spot with accelerating growth.

New business and export orders softened, with exports contracting at the sharpest pace since December 2022.

Business sentiment hit a near five-year low, and global employment was flat as services hiring offset manufacturing job cuts.

Global economic output expanded at its slowest pace in 17 months, highlighting growing signs of fatigue in the world economy. The J.P. Morgan Global Composite PMI® Output Index fell to 50.8 from 52.0 in March, marking its eleventh consecutive month below the long-run average of 53.2. This deceleration was driven mainly by weaker service sector growth and persistently weak manufacturing performance, with particularly noticeable slowdowns in the United States, China, and the euro area.

The service sector, despite posting its 28th consecutive month of expansion, saw growth slow to one of the weakest points in its current cycle. Business and consumer services both experienced diminished momentum, while financial services was the lone sub-sector to record a slight acceleration. Meanwhile, manufacturing output saw only modest gains. Production in consumer and intermediate goods rose, but investment goods merely stabilized following a contraction in March.

Regionally, the economic deceleration was broad-based. The US, China, the euro area, and Australia experienced a loss of momentum. The UK and Brazil fell back into contraction territory, and Canada registered a deeper downturn. Conversely, India remained a standout performer, with robust and slightly accelerating growth.

New business volumes also showed signs of fragility. Although total new orders rose for the 18th straight month, the pace was the second-slowest in that sequence. Service sector new business growth was the weakest since November 2023, and manufacturing new orders contracted slightly—the first decline in four months. Export demand was particularly weak: after a brief uptick in March, new export orders fell sharply in April, posting the steepest decline since December 2022, affecting both manufacturing and services.

Business sentiment suffered due to increasing economic uncertainty and trade instability. Confidence hit a near five-year low, with pessimism rising in major economies including the US, euro area, China, Japan, and India. Only France and Canada showed improved outlooks.

Employment levels remained static in April. Job gains in the services sector, especially in business services and consumer-related categories, offset manufacturing job losses. Input costs continued to rise, extending an almost five-year inflationary trend. However, cost inflation eased to a three-month low and aligned with long-run averages. Businesses continued to pass some of these higher costs to customers through increased output prices.

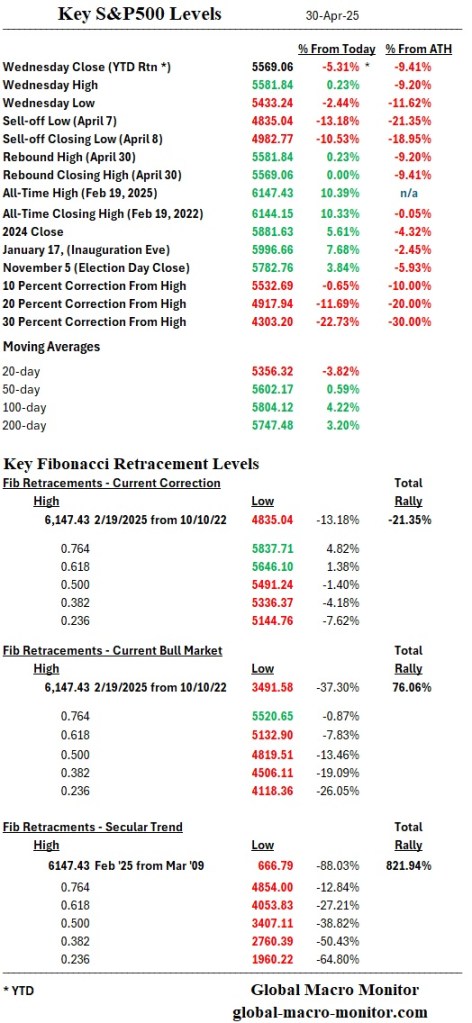

This week, global equities extended their recovery, buoyed by rising optimism over potential U.S.–China trade negotiations. Though no formal talks or trade agreements have been signed and most tariffs remain in place—including broad-based global levies—markets responded positively to U.S. administration signals suggesting some trade deals may be near (recall “Infrastructure Week” during Trump 1.0). This has helped drive the S&P 500 to its ninth consecutive gain, approaching a key technical level at 5747.66, its 200-day moving average.

Investor sentiment has shifted, despite contradictory macroeconomic data. April’s U.S. payrolls report exceeded expectations with 177,000 new jobs, indicating labor market resilience. Meanwhile, Q1 GDP contracted 0.3%, driven primarily by an import surge ahead of expected tariffs. The contraction masked the underlying strength in consumption and business investment, which is probably distorted by the tariffs, pointing to front-loaded demand rather than structural strength.

Dazed and Confused

This divergence is creating confusion among economists. The rally appears disconnected from fundamentals, yet persists amid AI enthusiasm, solid tech earnings x/ Apple, and easing energy prices. Historically, markets revert to hopium and to a bullish default mode. Data from our “S&P500 Significant Digits” table supports this: since 1950, the S&P 500 has posted gains 72.46% of the time on an annual basis, with an average return of 8.71% and a standard deviation of 16.20%. On a monthly basis, the S&P500 is up 60% of the time.

Market breadth has improved, led by mega-cap tech, small-caps, and renewed strength in the AI sector. However, as noted in multiple reports, the post-tariff economic environment lacks historical analogs, similar to how language models operate without pattern certainty. Without a clear forward path, investors are defaulting to the historical mean—bullish.

Global Markets

Globally, Eurozone Q1 GDP surprised to the upside, but inflation remains sticky. UK sentiment and housing have softened. Japan’s BoJ held rates steady and pushed back policy tightening, citing trade uncertainty. Chinese PMIs deteriorated, yet signals of trade thaw, including selective tariff exemptions, have supported regional equities.

Upshot

In sum, the market rally reflects forward-looking optimism rooted more in narrative than in data. The next test lies at the 5747.66 mark—whether momentum can overcome macro headwinds remains uncertain. The 200-day is just a chip shot away. Until then, markets appear to be pricing in the best-case scenario, which, in our opinion, will not be the best case as the Administration appears not to know what it wants: 1) Reshoring of manufacturing? 2) The tariff revenue? Or 3) Lower tariffs for American exports and freer trade? The macro market is choosing #3, but we believe Trump wants #1; both are mutually exclusive.

We believe empty shelves are just a few weeks away.

Stay frosty, folks.

Markets

U.S. equities extended their recovery: S&P 500 posted a ninth consecutive gain, supported by strong earnings and easing trade fears.

S&P 500 approaching 5747.66, its 200-day moving average, a key technical resistance level.

Market breadth improved, with gains across large-cap tech and small/mid-cap stocks.

Investor sentiment is buoyed by optimism over potential U.S.–China trade negotiations, though no agreement has been finalized.

U.S. Market Analysis

Strong labor data: April nonfarm payrolls rose by 177,000, exceeding expectations; unemployment steady at 4.2%.

Q1 GDP contracted –0.3%, mainly due to a surge in imports ahead of tariff implementation.

Markets interpreted the negative GDP print as temporary and driven by front-loaded demand.

AI and tech stocks led gains; mega-cap earnings (e.g., Microsoft, Meta) surprised to the upside.

Treasury yields rose late in the week, reacting to jobs data; credit markets stable with narrowing spreads.

Global Market Analysis

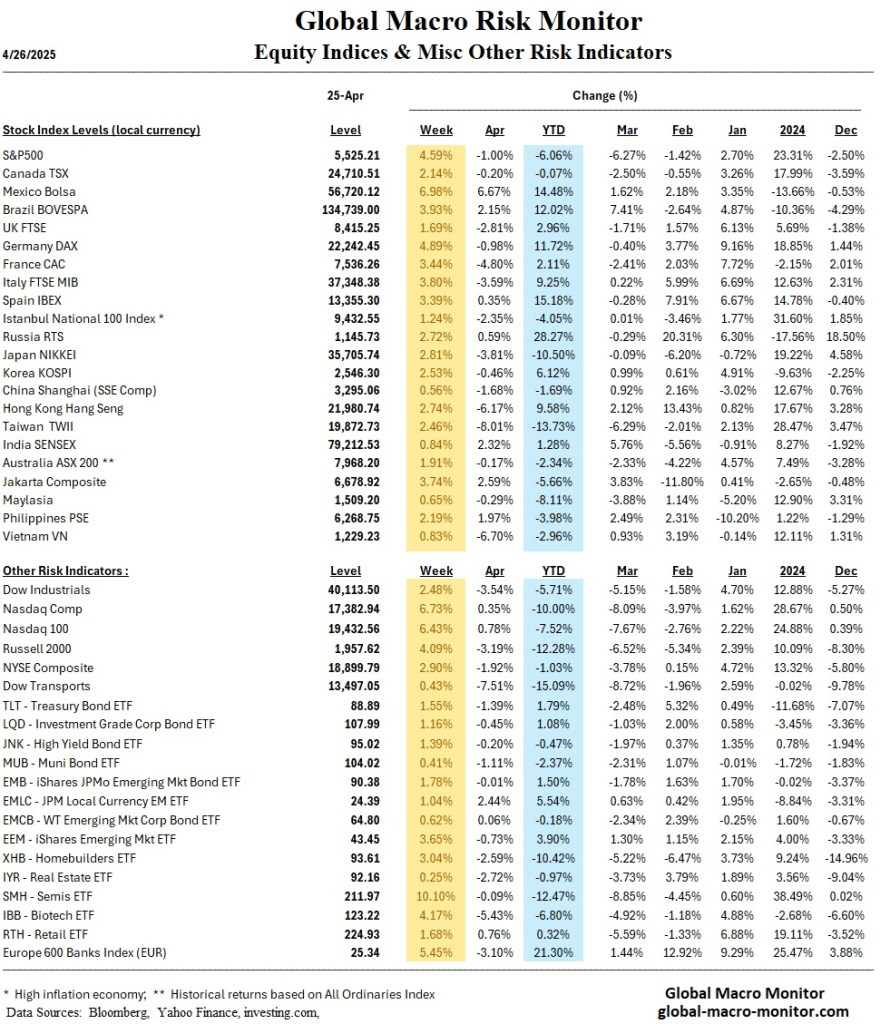

Europe: STOXX 600 +3.44% as trade tension eased; Germany +4.63%, France +3.57%, Italy +4.13%.

Eurozone GDP beat expectations in Q1 at +0.4%; inflation remained elevated at 2.2% headline, 2.7% core.

Japan: Nikkei +3.15%, TOPIX +2.27%. BoJ held rates steady and downgraded growth and inflation forecasts.

Yen weakened modestly; 10Y JGB yield fell to 1.26%.

China: Mainland indexes down slightly; Hang Seng +2.38%. Manufacturing PMI fell to 49.0—deepest contraction since Dec. 2023.

Beijing hinted at a willingness to resume trade talks with the U.S.; partial tariff exemptions granted on select U.S. goods.

Economics

U.S. Economic Overview

Labor market resilient, though early-week data (ADP, JOLTS) showed signs of softening.

Consumer spending rose 0.7% in March; PCE inflation flat, offering comfort to the Fed.

Market anticipates the Fed will hold rates steady in May; futures pricing of June cut has declined.

Surging imports dragged GDP but suggested stronger-than-expected demand fundamentals.

Equity markets extended their rebound today, bouncing smartly from a sharp early morning sell-off. The S&P 500 closed at its highest level since the recent correction, marking a notable shift in sentiment. Based on where futures are trading this evening, the index appears poised to open above its 50-day moving average (currently at 5602.17), a level closely watched by systematic and momentum-driven strategies. A decisive move above this threshold could trigger mechanical buying and attract further technical inflows.

The next resistance lies at the 0.618 Fibonacci retracement level (5646.19), a technically significant marker often associated with sentiment inflection points. Given the still-uncertain macroeconomic backdrop, reclaiming that level would be notable—if not perplexing.

The market continues to play chicken with the economic data, refusing to turn bearish until it sees the whites of recessionary eyes. Despite mixed macro signals, investors are holding their ground, unwilling to price in a downturn without clear, negative confirmation. So far, the data hasn’t delivered a decisive blow. Meanwhile, tonight’s strong prints from Meta and Microsoft underscore that the AI-driven growth narrative remains intact, providing just enough fuel to keep risk appetite alive, particularly in the mega-cap tech space.

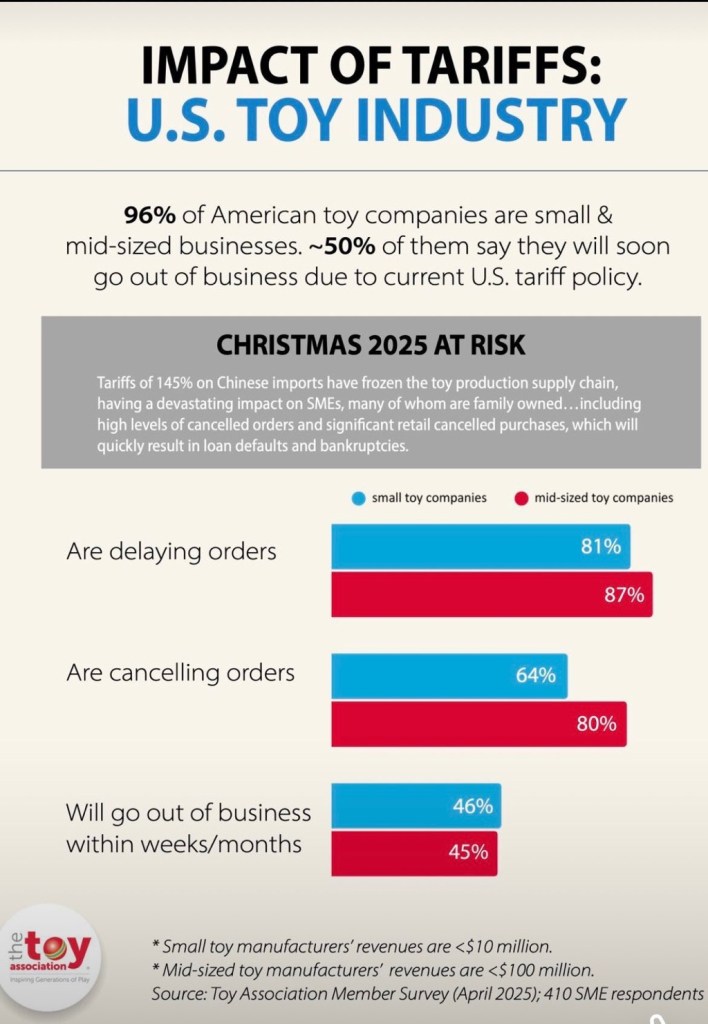

Struggling families may find they can’t afford presents this Christmas — or worse, they may face empty shelves altogether — thanks to Trump’s tariff policies.

And really, what’s the point? It’s hard to imagine a sudden surge of American elves lining up to work in toy factories — unless perhaps it’s immigrants, who are being shown the door anyway.

But never mind. The tariff revenue from imported toys will no doubt help finance another round of Ebenezer-sized tax cuts.

This holiday season’s best pairs trade? Short Santa Claus/Long Ebenezer Scrooge…And weep for our children

Note: As of the first seven months of last year, mainland China still made 79% of toys sold in the United States and Europe, versus 82% in 2019.

This will be a huge political loser for Trump and we wouldn’t be surprised to soon see exemptions for the toy industry. Stealing kids toys for tax cuts? We don’t think so.

Global markets staged an impressive rebound this week, fueled by growing optimism that trade tensions between the United States and China may soon ease and that some bilateral trade deals are imminent. Investors eagerly latched onto comments from U.S. Treasury Secretary Scott Bessent and President Trump suggesting that tariff levels were unsustainable and that some dialogue, formal or informal, might be underway. This generated a powerful relief rally, with the S&P 500 and Nasdaq surging approximately 4.6 percent and 6.7 percent, respectively. However, despite the ebullient market response, no formal negotiations or agreements have been reached, and the underlying political dynamics remain deeply adversarial.

Hope v Reality

The reality is that while hopes of de-escalation buoy markets, the U.S.-China standoff is mired in political ego. President Trump appears reluctant to make the first move toward a deal, wary of appearing weak ahead of the 2026 elections. Conversely, President Xi Jinping, emboldened by China’s relative economic stabilization and newly announced stimulus plans, is taking a patient, strategic approach. With no official meetings scheduled, the current atmosphere reflects more wishful thinking than tangible progress.

Therein lies the core risk: investors may be underestimating the political barriers to resolution. Trump’s current position is precarious. Without a trade breakthrough, the U.S. could soon face visible consequences—empty store shelves, rising consumer prices, and a dent in consumer confidence—as tariff impacts cascade through supply chains beginning next month. If economic pain intensifies, Trump may be forced into a humiliating climbdown to avoid severe electoral damage.

Bulls Back In Charge

Nevertheless, the S&P500 bulls captured a key level on Friday, the .5 Fibonacci retracement at 5491, putting the bulls in charge for now. Shorts are foolish to fight this market, especially knowing it is very likely that some large traders/investors have access to material non-public information and are trading on it, which is an absolute f$%king disgrace.

Watch Your Time Horizons

We believe that medium to long-term optimism may be mispriced. There is a prevailing belief that resolving trade tensions would automatically unlock a fresh wave of global growth. Yet this is misleading. Even if tariffs were significantly reduced from current levels, the global economy will still face the structural headwind that tariffs will be much higher than they were at the beginning of the year, reducing world trade and therefore global growth.

Imagine, for example, if Macy’s doubled its prices, then announced a 25% off weekend sale. Are customers really better off than before the price hikes? Of course not. Yet that’s exactly how the market seems to be reacting to the latest headlines. Sure, 25% off sounds better than a 100% increase—but seriously, Mr. Market? Tariffs will remain much higher than they were before this entire mess began.

Moreover, the uncertainty generated by the tariff wars has already inflicted lasting damage on investment confidence. The idea that a quick deal would fully reverse these scars is naïve.

A Zero Tariff Deal?

One significant development this week was the soft proposal, or more like an idea thrown out by German Finance Minister Jörg Kukies, for a comprehensive zero-tariff agreement between the U.S. and Europe. Kukies eloquently argued, “The easiest way to ensure balance and fairness is for everyone to go to zero. Then we have free trade, efficiency, and economies of scale. We can think about standardization, mutual market access, and many other things”.

From a pure economic perspective, this is sound logic. True free trade would enhance productivity, lower costs, and strengthen growth on both sides of the Atlantic.

However, President Trump does not align with free trade orthodoxy. His administration’s goal is not greater global economic efficiency; it is to reshore manufacturing and generate tariff revenues to finance prior tax cuts. These objectives fundamentally conflict with a zero-tariff deal. Accepting such an agreement would dismantle the entire strategic rationale, if there is one at all, behind the tariff regime. Thus, despite Germany’s overtures, it is highly unlikely that Trump would agree to zero tariffs—unless political and economic pressures render his position untenable.

Looking ahead, while the recent rally in equities has been impressive, there are clear limits to upside potential unless there is a definitive resolution on trade. The markets are functioning on hope rather than substance. Earnings risks are rising, though Q1 is shaping up to be better than expected, economic indicators are softening, and monetary policymakers, including the Fed and ECB, are increasingly hamstrung by uncertainty.

If trade tensions linger—and especially if tariffs continue to feed into inflation and constrain growth—the global economy could be pushed into a downturn in the coming quarters. The durability of the current market rally is, therefore, suspect. As real economic impacts begin to materialize, the cheerful narrative driving markets today may give way to renewed volatility and risk aversion.

Summary

While the past week brought a welcome reprieve to markets and may continue, the fundamental dynamics have not changed. The U.S.-China standoff remains unresolved, driven as much by political pride as economic strategy. The German proposal for a zero-tariff regime, while admirable, is almost certainly dead on arrival in Washington. Thus, caution remains warranted. Investors should not be lulled into complacency by superficial signs of progress; instead, they must prepare for the possibility that the real economic fallout of tariff escalation is only just beginning.

Markets

U.S. Market Analysis

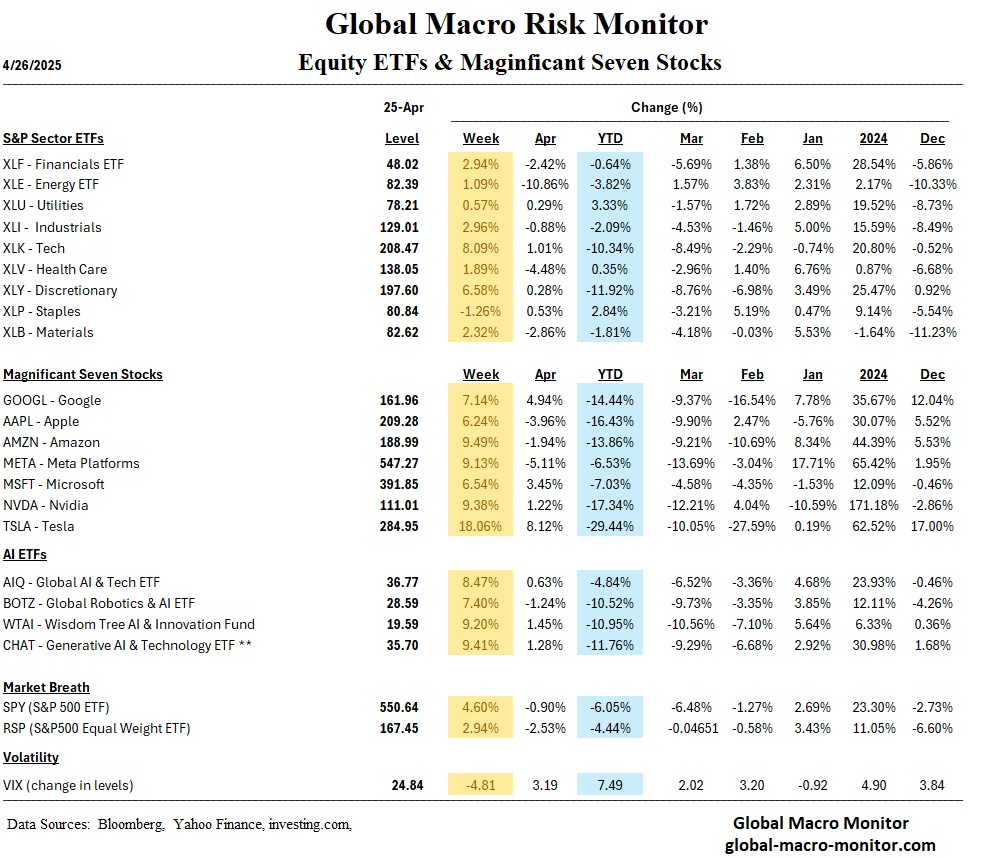

Markets Rebound Sharply: U.S. equities posted their strongest week since late 2023, buoyed by optimism over potential de-escalation in U.S.-China trade tensions. The S&P 500 rose 4.6%, the Nasdaq surged 6.7%, and the Dow gained 2.5%.

Small-Caps Lead Gains: The Russell 2000 rose 4.1%, outpacing large caps for the second consecutive week, helped by strong tech earnings and expectations of a more dovish Fed.

Market Breadth Improves: Participation broadened across sectors. The percentage of S&P 500 stocks above their 200-day moving average rose to 34.2%, up from 29.4%.

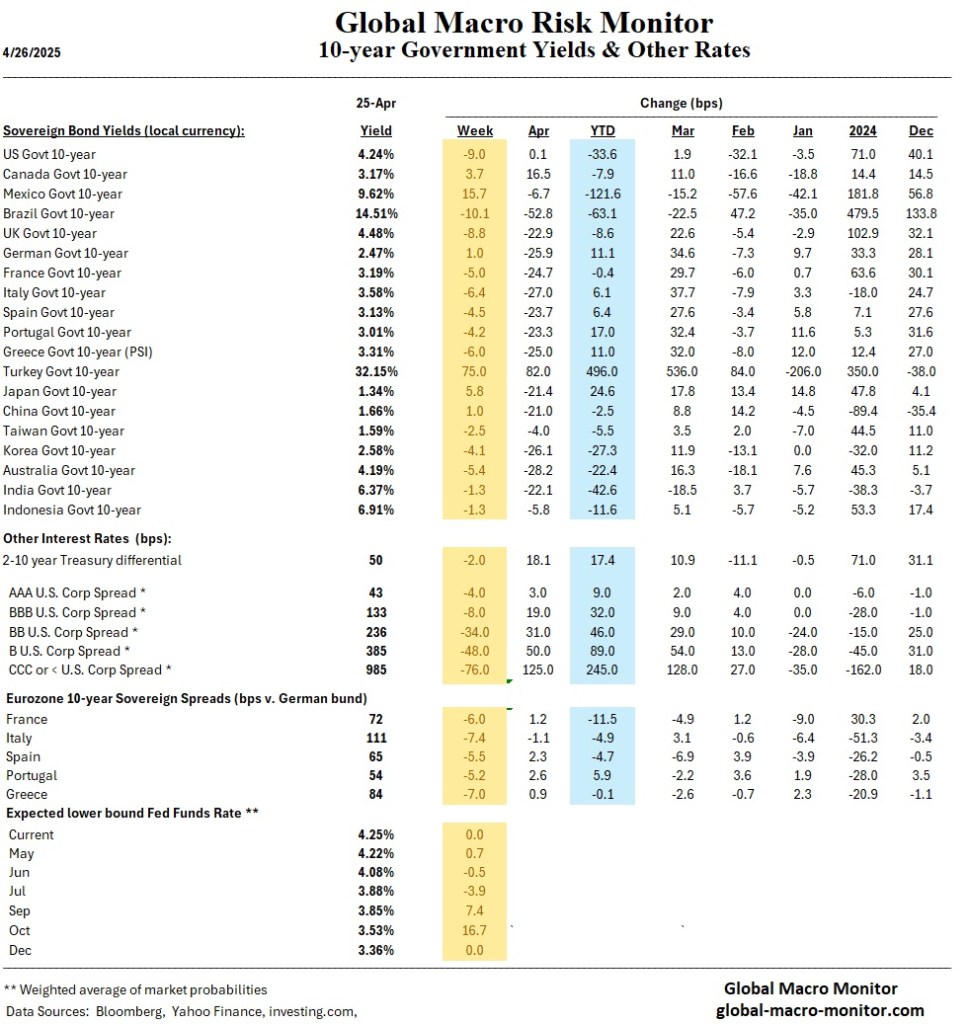

Bond Yields Ease: 10-year Treasury yields fell 8 bps to 4.24% as safe-haven demand moderated and growth concerns lingered.

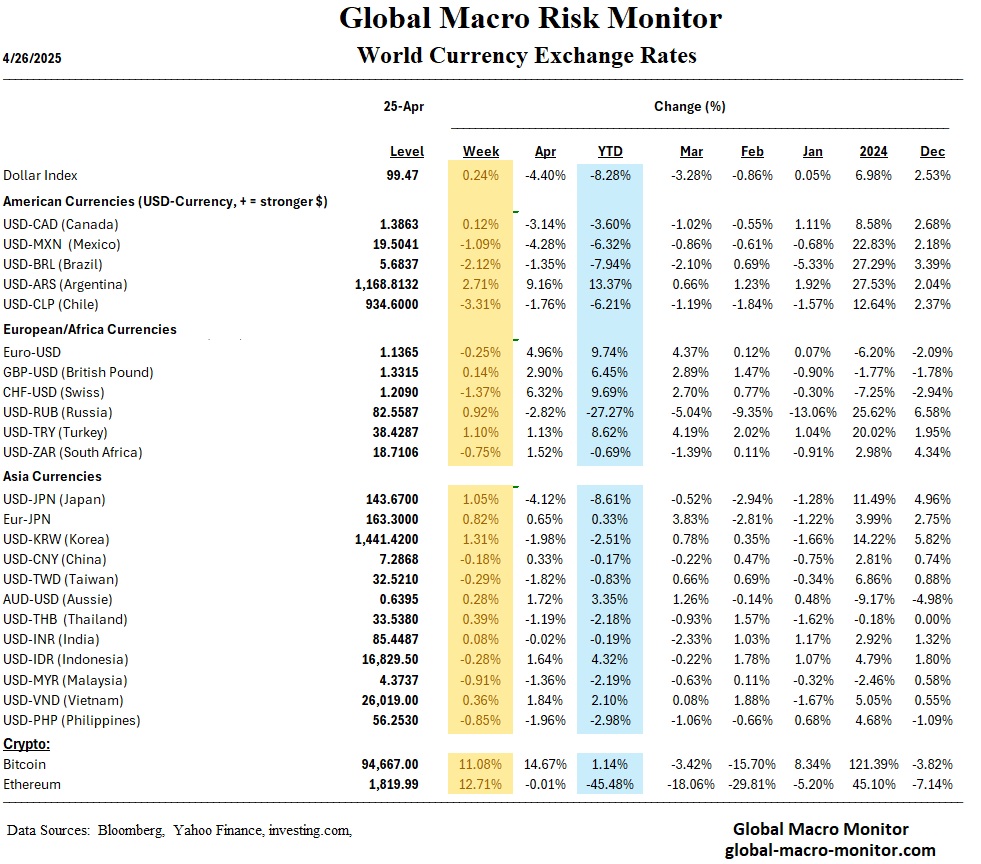

Bitcoin Rally Continues: Bitcoin surged over 11%, rebounding toward the $100K mark, supported by optimism around broader risk appetite.

Europe: STOXX Europe 600 gained 2.77%, led by Germany’s DAX (+4.89%) and France’s CAC 40 (+3.44%), following Trump’s softer tone on tariffs and improving earnings sentiment.

Asia:

Japan: Nikkei 225 advanced 2.8%. BoJ policymakers hinted at maintaining easy monetary policy amid tariff uncertainty.

China: Shanghai Composite rose 0.56% as stimulus expectations bolstered sentiment despite continuing trade tensions.

Emerging Markets:

Emerging Asia: GDP downgrades for Singapore, Malaysia, and Korea weighed on sentiment, but policy stimulus measures are expected to cushion the slowdown.

Latin America: Held up relatively well as supportive domestic factors offset external headwinds.

EEMEA: Caution prevails amid capital flow risks, but no immediate crises are detected.

Economics

U.S. Economic Overview

Positive Earnings, But Slower Growth: 73% of reporting S&P 500 companies beat earnings expectations. However, S&P Global PMI data showed business activity slowing to a 16-month low, especially in services.

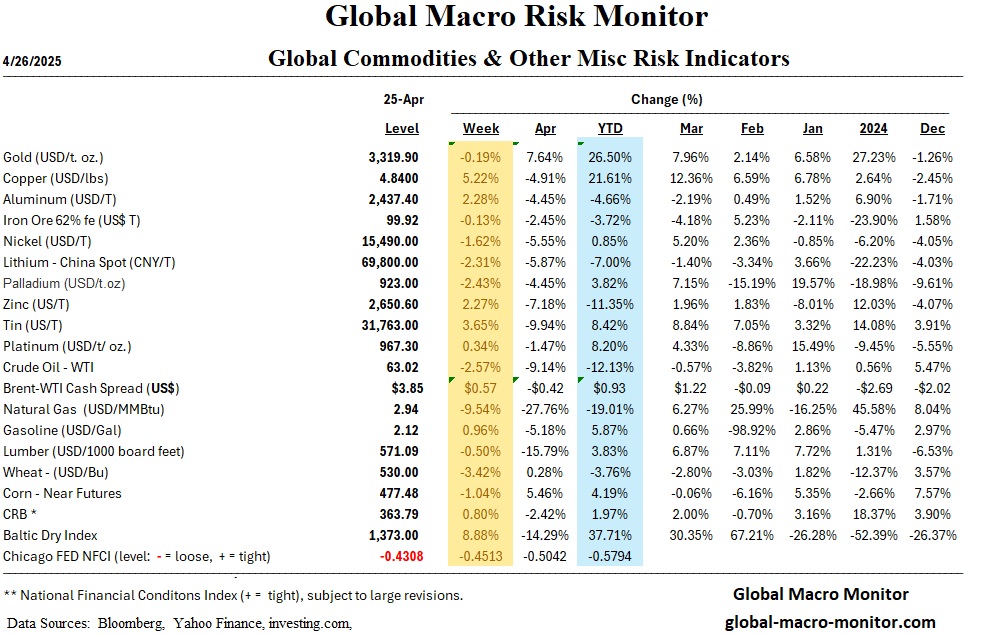

Tariff Inflation Risks Reemerge: Prices charged for goods and services rose at the fastest pace in over a year, largely due to tariffs.

Consumer Sentiment Weakens: University of Michigan’s Consumer Sentiment Index fell for the fourth consecutive month, highlighting persistent uncertainty around trade policy.

Fed Outlook Steady: Markets maintain expectations for two Fed rate cuts in 2025. Longer-term rates fell this week amid rising concerns about Q2 growth.

Housing Market Softens: Existing home sales plunged 5.9% in March to the lowest March level since 2009, weighed down by high mortgage rates.

Global Economic Overview

Eurozone: Growth outlook dimmed as April PMI data pointed to weakening services and manufacturing. German GDP forecasts downgraded to zero growth for 2025.

China: Despite better-than-expected Q1 GDP, new tariffs threaten future exports. Beijing’s Politburo announced preparations for emergency stimulus measures.

Japan: Tokyo CPI inflation rose faster than expected, bolstering the case for a BoJ rate hike later this year, but tariff risks complicate the timeline.

Australia & Colombia: Central banks kept rates steady; rate cuts still expected as global risks intensify.

India: RBI expected to cut rates by 25 bps following softening inflation and weaker growth.

Mexico & Norway: Key inflation data due next week will likely dictate the timing for further easing.

Week Ahead (April 28–May 2, 2025)

Key U.S. Events:

Economic Data:

Tue (Apr 29): Advanced International Trade, Consumer Confidence

Wed (Apr 30): ADP Jobs Report, Q1 GDP, Pending Home Sales

Thu (May 1): ISM Manufacturing Index, Jobless Claims

Fri (May 2): Nonfarm Payrolls, Unemployment Rate

Earnings:

Mega-Cap Tech Reports: Microsoft, Meta (Wed); Apple, Amazon (Thu)

Key Global Events:

China PMIs: Wednesday—will gauge early tariff impact.

Eurozone GDP & CPI: Wednesday—critical for ECB policy outlook.

Bank of Japan Meeting: Thursday—no change expected, but tariff commentary crucial.

Tariff Developments: Any new trade announcements could cause sharp market moves.