Summary

- The U.S. government’s cumulative monthly deficits in the first 29 months of the Trump Administration has almost doubled from the prior 29 months

- The sum of monthly deficits totaled $1.08 trillion during the period Sep. ’14 to Jan ’17 and has increased to $2.03 trillion in the 29 months from Feb ’17 to Jun ’19, rising from 5.9 percent of GDP to 10.1 percent of GDP. A significant increase

- The efficacy and efficiency of fiscal stimulus and deficit spending appear to be diminishing. For every dollar of deficit spending from Sep ’14 to Jan ’17 nominal GDP increased by $1.32 compared to $1.08 in the period Feb ’17 to Jun ‘19

- This raises a red flag that the U.S. and the world may be entering a debt trap similar to the monetary liquidity trap the world currently finds itself

- The fight over raising the national debt ceiling is heating up as the Treasury has warned Congress it may run out of money by September

- We layout, what we believe, is the grand narrative driving global markets in the first half of the post before diving deep into our analysis of the U.S. budget

I’m the king of debt. I’m great with debt. Nobody knows debt better than me. I’ve made a fortune by using debt, and if things don’t work out I renegotiate the debt. I mean, that’s a smart thing, not a stupid thing. – Donald J. Trump, June 2016

Nobody cares about debt and deficits anymore. Until they will.

The King Of Debt needs to get on with negotiating an increase in the debt ceiling before the government runs out of cash in September,

“It’s one of those cartoonish anvil-over-head moments,” one senior GOP congressional aide told CNN. “We all look around knowingly like ‘Man, we’re about to get crushed by this,’ but nobody’s really sure how to get out from underneath it right now.” — CNN

Grand Narrative & Why Interest Rates Can’t Move Higher

Debt stocks are becoming so large interest rates cannot rise to their equilibrium levels as the amount of global debt is not sustainable with higher rates, which would seriously destabilize the global economy and markets.

The major debtor governments‘ net interest payments would skyrocket, budget deficits would balloon, forcing deep spending cuts, and/or larger deficit financing, more monetization (most likely), and higher interest rates. Wash, rinse, repeat. The classic debt doom loop.

Higher long-term interest rates will also trigger a real come-to-Jesus moment for asset valuations.

Q4 2019 Mini-Bear Market

The markets’ nervousness over such a scenario was evident in Q4 2018 when U.S. 10-year yields broke out in late September and triggered the sharp and swift 20 percent sell-off in the S&P500 until the Fed was beaten into submission. The Q4 reckoning, albeit temporary, was just an appetizer for the full course coarse meal, which will inevitably be served up.

GMM Pop Quiz

Q: Why do dogs lick their….uh…um…….tails?

A: Because they can.

Q: Why don’t interest rates go up?

A: Because they can’t.

Excuse a little more diversion as we turn up the mood music and further set the narrative for our analysis of the current U.S. budget situation.

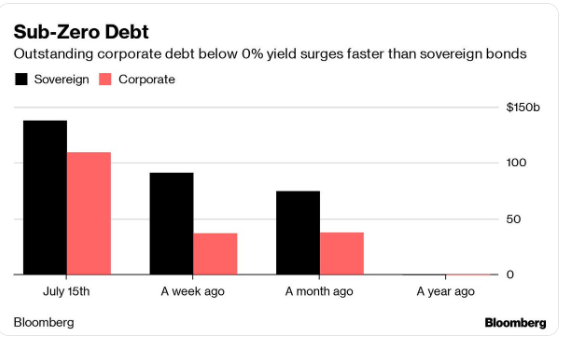

Global Bond Market Sucked Into A Black Hole Of Negative Yields

The total stock of negative-yielding debt is now is around $13 trillion dollars, including benchmark sovereign bonds in Japan, Switzerland, Germany, France, and the Netherlands, and even in some emerging markets. All of the Czech Republic euro bonds, for example, now trade with negative yields. That is just stunning.

Though all of the U.S. government’s $16 trillion-plus marketable debt still trades with a positive yield, the cost of hedging out the currency risk for foreign buyers pushes the effective yield into negative territory,

Hedged European investors now earn a roughly minus-0.5 per cent yield on a 10-year US Treasury on a three-month rolling basis, according to Bloomberg data, compared to an unhedged yield of 2.58 per cent. Hedged Japanese investors earn minus -0.3 per cent. – FT, April 17th

The rising cost of currency hedges has forced many European investors to abandon the U.S. and chase yield in the eurozone periphery and Eastern European emerging markets bonds, and also to take on more unhedged currency risk in their portfolios.

Italian 10-year bond yields are now trading 30 bps through U.S. 10-year yields. Never thought I would live to see that.

Yes, we get it, different currency, interest rate parity, yadda, yadda, yadda.

Do you really think the risk of another existential crisis in the eurozone in the next ten years is that low? And that eurozone policymakers have more firepower to fight the next crisis, which will most likely be triggered by politics?

The increase in unhedged currency positions in global bond portfolios also significantly elevates the risk of a volatility spike in global capital flows and the currency markets. Recall the Tequilla, Asian and Russian crises of the late 1990s

Sovereign Borrowers Have Found A New Revenue Source

Moreover, if the rush to sub-zero percent continues, some of these government borrowers — can’t even rule out the U.S. G — are going to be convinced they have found a new source of revenue to finance profligacy. Generate more revenue by running bigger budget deficits to accelerate the expansion of negative-yielding debt.

It’s a wonderful thing to have your creditors pay you to borrow from them,

In Germany, 85% of the government bond market is underwater. That means investors effectively pay the German government 0.2% for the privilege of buying its benchmark bonds; the government keeps 2 euros for every 1,000 euros borrowed over a period of 10 years. — Bloomberg

The new zoom loop, folks. It’s a no-brainer!

Maybe that’s the genius of the Trump administration and what it is counting on by beating on Chairman Powell? Blowing up the budget deficit with the hope of generating revenues on soon to be negative-yielding debt.

Reading More Kafka

That’s why we are reading more Kafka these days. His writings keep us open and flexible to the fact that just when we think peak absurdity has been reached in the bizarro world and bizarro times in which we now live, there is another bizarro dimension out there to write the next chapter.

Asset Markets Have A Napolean Complex: A World Of Shortages

Seriously, the world’s not that hard to figure out. The metanarrative of the markets is we now live in a world with some serious shortages in key major asset classes.

We have posted several pieces on this new supply-side economics.

Because demand and supply curves are theoretical models and not observable, one should always suspect a negative supply shock (shift in the supply curve up and to the left) when prices are rising and quantity/volume declining.

Risk-Free And Stocks

The global central banks have generated a shortage of so-called “risk-free” and high-quality fixed-income assets with their massive asset purchases over the years, officially depressing key benchmark interest rates. The financial repression currently taking place in global markets makes North Korea look like Woodstock, circa 1969.

Corporations have taken advantage of the low-interest rates by borrowing and buying back their stocks creating a relative shortage of public equities.

Risk-Taking, More Saving, And Less Consumption

Mrs. Watanabe, the Belgium dentists, and all those widows and orphans now receive zero percent (or close to and some negative) on their CDs and savings accounts, suffering a shortage of income from relatively safe assets. They are forced into risky assets, such as stocks and 100-year Argentine bonds to pay for groceries and to keep the lights on. More demand for risk, though under duress, and less supply of assets for sale.

It doesn’t take a genius. True north for asset prices.

At least until Wylie E. Coyote has his epiphany that gravity is not fake news.

Moreover, many of these historically conservative investors, such as the graying Mrs. Watanable and the Belgium dentists, are forced to cut back on consumption to save more for and stretch their retirement funds, slowing economic growth, which works counter to the very policy goals of repressing interest rates in the first place.

Private Equity Shifts Residential Housing Supply Curve Big Left

Helped by the foreclosure crisis, private equity and investors have become the largest holders of single-family homes taking them off the market and converting to rentals, shifting the supply curve of the existing homes big left. This has driven up prices and helped to create a shortage of entry and mid-level single-family homes for young families. The cost of building new homes has also skyrocketed due to shortages of buildable land and construction labor. Higher prices, lower volumes – a classic negative supply shock.

All taking place as the financial world goes virtual with AA – Automation, and Algos.

Efficient markets?

What is the message of the market?

You have got to be shitting me.

The global asset markets are joined at the hip with the global economy in some serious funk and one strange and dangerous feedback loop.

Napolean’s Achilles Heel

Did you catch the Achilles heel in all this?

All that corporate debt issuance may be the beast that comes back to haunt the global markets. And when it does comes back, who will be the buyers? The JP Morgan and the Goldie bond desk? Good luck with that.

I have no doubt the same words uttered by one of my corporate bond traders during a major financial meltdown when I asked how his market was doing will once again show up in some tweet gone viral,

“My market’s fine. Prices are holding up because there’s no bid.”

The system is not that stable, folks. Yield chasers are skating on ice, which is much thinner than it looks.

Wish we could pinpoint the exact date when it cracks. We would buy you all yachts with what is left after first helping the less fortunate, who will be hurt the most when the music stops.

We think it’s much closer than the lathered up bulls think.

As always, we reserve the right to be wrong.

Enough.

Time to move to a topic with less conjecture, that is more factual and backed by hard data.

The Trump Deficits

We felt very Kafkaesque this afternoon when we came across the following data from the U.S. Treasury, which we present to you tonight. We were prompted by today’s Wall Street Journal article,

In the 12 months that ended in June, the deficit totaled $919 billion, a 22.6% increase from the same period a year earlier. As a share of gross domestic product, the year-over-year deficit totaled 4.4%, much higher than the previous 12 months. – WSJ, July 11th

We downloaded the data from the Treasury and started crunching.

Comparing Trump Deficits To Obama’s

We have juxtaposed the cumulative Federal deficits of President Trump in his first 29 months in office, and also the 21 months since the month of his first full fiscal year, which began October 2017, with similar similar periods of the Obama administration. The current administration can argue they inherited the 2017 fiscal year budget and should not be held responsible for that year’s red ink. We concur so we present you both periods

We compare the Trump and Obama deficits not only because we need a point of reference but also President Trump likes to tout his economic performance relative to his predecessors.

The data show that the cumulative monthly deficits during President Trump’s first 29 months in office have almost doubled those of President Obama’s last 29 months, increasing from $1.1 trillion to $2.0 trillion, or 5.9 percent to 10.1 percent of GDP. The increase is not insignificant.

During the 21 months since Trump’s first full fiscal year in office, the cumulative monthly deficits have increased from $902 billion in Obama’s last 21 months to $1.53 trillion, or 4.8 percent to 7.5 percent of GDP. The increase has occurred even as nominal GDP grew at a 2.5 percent faster clip. In today’s economy, the norm is for a much smaller budget deficit, or even a surplus as deficits should be declining in proportion to GDP with faster nominal economic growth.

One major caveat is the seasonality in the budget data. For example, April is a month of huge budget surpluses as revenues flood into Treasury to meet the April 15th tax filing deadline. This may or may not affect our timeframes and calculations, which may cause the data to look more favorable for one administration. We will take a look at it later but suspect the impact is marginal and de minimis, however, and have no idea which, and how each administration’s cumulative deficit is affected.

Marginal Product Of The Deficit (MPOD)

We also calculate the marginal product of the deficits, which attempts to measure the efficiency of deficit spending and the impact of the stimulus. That is, how much does the nominal GDP increase given each dollar of deficit spending? It’s a crude and rude measure, suffers from many shortcomings, but interesting, nonetheless. It is also very similar to the concept of the Incremental Capital Output Ratio (ICOR).

Red Flag Warning

The data show it is taking more and more of deficit spending or an increase in debt to generate an additional dollar of nominal GDP. In the full 29 month period, Obama’s MPOD was 1.32, which translates — for every dollar of deficit spending or increase in debt, nominal GDP increased by $1.32. The MPOD under Trump drops to 1.08, which illustrates the diminishing efficacy of fiscal stimulus.

Note the Treasury can and does temporarily finance itself not just by issuing new debt but by running down its cash balance at the Fed or by other means, such as running arrears on certain payments. This is a very small fraction of their financing over the longer-term and really only matters during debt ceiling fights, like in the now.

There is a legion of possible reasons for the decline in the MPODs, such as how tax cuts are allocated, how, where, when and in what sectors the increased spending takes place, is the public spending investment or consumption, too much existing debt, or it could be just noise. We will leave it to the academics and Ph.D. dissertations to nail it down and deal with the other issues, such as the relative seasonalities in the different data series,

Take heed, however, the U.S. and world may be or have already entered a debt trap just as it similarly finds itself — more so for the rest of the world — in a monetary policy liquidity trap.

Conclusion

The data couldn’t be more clear. President Trump is no traditional conservative. Not concerned about the deficit or the increase in the national debt. The data speak louder than words in tweets.

The above analysis reminds me of a modern-day version of the old LBJ-Barry Goldwater political colloquialism,

In November 1964, my liberal friends told me if I voted for Barry Goldwater, there would be a major escalation in Vietnam. I voted for Barry Goldwater and, sure as night follows day, we got the escalation in Vietnam.

The modern-day version goes something like this,

In November 2016, my conservative and Tea Party friends told me if I voted for Bernie, the budget deficit would explode and the national debt would skyrocket. I voted for Bernie and….. Do I need to finish?

Debt Ceiling

Finally, keep the debt ceiling debate on your radar, folks.

Treasury Secretary Steven Mnuchin warned House Speaker Nancy Pelosi that the government may run out of cash in early September if Congress doesn’t raise U.S. borrowing authority. — Bloomberg

The jousting continues,

“I am personally convinced that we should act on the caps and the debt ceiling,” Pelosi told reporters, “prior to recess.”

For a brief time, White House negotiators agreed the two issues should be coupled, but they have since started to change their minds as a deal with Democrats on the top-line spending numbers has proved elusive.

They are now worried that a spending deal with Pelosi will add more than $300 billion to the deficit over the next two years and damage Trump’s reputation as a fiscal conservative with Republican voters.

By separating the debt limit from the spending talks, White House negotiators believe they will have more leverage to press Democrats to accept a smaller spending increase for domestic programs.

But congressional Republicans are warning the White House that a vote on just the debt limit would invite trouble. — The Hill

The White House worried about the “damage to Trump’s reputation as a fiscal conservative with Republican voters?” I want some of the Tea that party is drinking.

There it is, folks, one small step beyond peak absurdity and one great leap into that next bizarro dimension waiting for the next chapter to be written.

Let’s keep it real. Show me the money data!

Appendix

Why do we look at the Obama administration’s last months rather than the first months in office? The two economic environments we compare need to be and are very similar. Obama assumed office during an economic collapse and it took many months for the nation to stabilize.

Notice The Continuity In The Job Markets Over Past Five Years?

Fiscal Years 2018 and 2019 – The Last 21 Months

Sources Of Federal Revenues And Outlays – Fiscal Year 2019

Hat Tip: Professor Greg Mankiw, Harvard University

![file-2[11755].jpeg](https://global-macro-monitor.com/wp-content/uploads/2019/07/file-211755.jpeg?w=611&h=458)