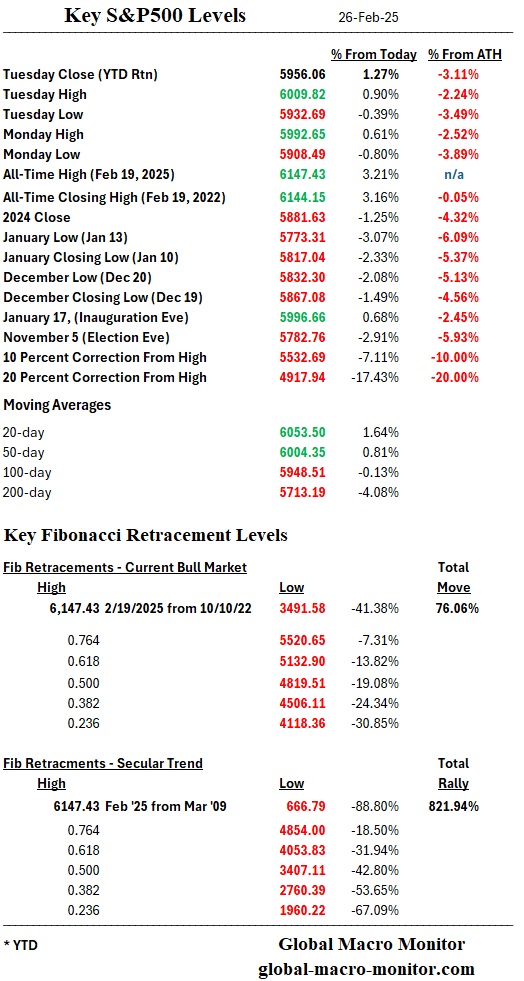

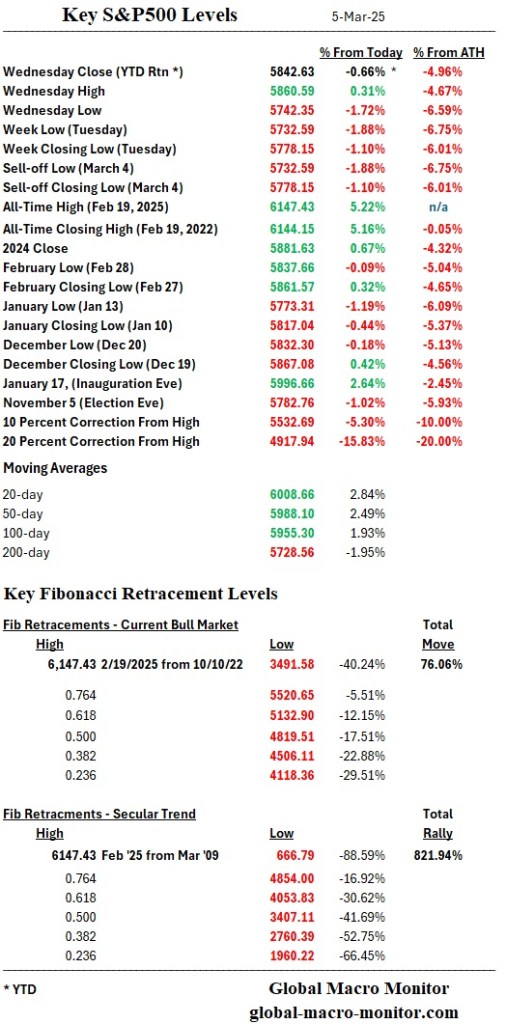

The line in the sand to the downside is 5737 and then 5700. Watch this space, folks.

The line in the sand to the downside is 5737 and then 5700. Watch this space, folks.

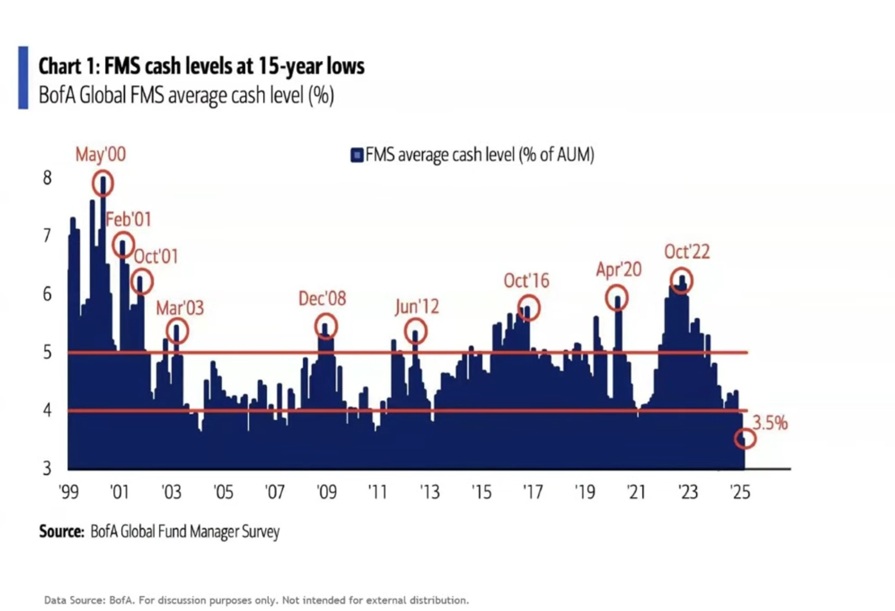

Warren Buffett is holding record-high levels of cash…

Fund managers are holding record-low levels of cash…

Hat tip: Charlie Bilelo

It looks like it’s Warren Buffett’s turn to say, “I told you so.” – Barron’s

As Trump seems to want to isolate and cut President Zelensky out of the peace negotiations while siding with Putin’s Russia, it conjures up an image of the Big Three – Putin, Xi, and Trump — carving up the world as they see fit. We sure hope not.

The Trump administration has, however, embarked on a significant departure from traditional U.S. foreign policy, emphasizing unilateralism over alliances and prioritizing economic negotiations over geopolitical stability. This shift mirrors historical instances such as the Yalta Conference of 1945, where great power negotiations reshaped European borders, and the treaties following World War I that rewrote the borders in the Middle East and beyond and attempted—often unsuccessfully—to enforce a lasting peace.

Trump’s approach to Ukraine, Europe, and global alliances reflects an emerging pattern of prioritizing national interests over multilateral commitments, raising concerns about the potential reordering of global power structures.

The Trump Doctrine: A New Yalta?

At Yalta in 1945, Franklin D. Roosevelt sought to secure a postwar order based on democratic principles but had to compromise with Soviet leader Joseph Stalin, resulting in Eastern Europe falling under Soviet domination. This decision was widely criticized as a betrayal of smaller nations in favor of great power pragmatism. A similar theme emerges in Trump’s handling of Ukraine. By shifting away from unwavering support for Kyiv and normalizing relations with Russia, the Trump administration appears willing to sideline Ukrainian sovereignty in pursuit of broader strategic objectives.

Trump’s treatment of Ukraine aligns with the concept of “great power deals,” reminiscent of the U.S. and Soviet agreement at Yalta. The difference is that Roosevelt operated within a multilateral framework, whereas Trump has abandoned such structures in favor of direct power negotiations. This reorientation represents a radical rethinking of U.S. commitments, raising concerns among European allies who fear becoming bargaining chips in a new geopolitical settlement.

Economic and Military Implications: The European Response

Europe’s reaction to Trump’s foreign policy echoes the aftermath of World War I when European nations struggled to establish an independent security architecture after U.S. disengagement. The Treaty of Versailles and subsequent treaties placed the burden of European security on fragile alliances, which ultimately collapsed with the onset of World War II. Similarly, Trump’s approach to Ukraine and NATO suggests a U.S. retrenchment that may leave European nations more vulnerable.

European leaders now face a stark choice: to assert their geopolitical independence or risk being sidelined. A recent analysis indicates that defending Europe without U.S. military support would require at least 300,000 additional troops and an annual defense spending increase of €250 billion. This suggests that European nations must urgently develop self-reliant defense mechanisms, mirroring past efforts to create European security structures in the interwar period.

The Economic Reordering: Parallels to the Interwar Period

Trump’s foreign policy also recalls the economic consequences of post-World War I diplomacy. The punitive economic measures of the Versailles Treaty fueled nationalist resentment and economic instability, leading to World War II. Similarly, Trump’s imposition of tariffs on European allies and his transactional approach to international relations risk disrupting global trade.

His administration’s proposed “economic reordering” aims to restructure the global economy in favor of U.S. interests, pushing European nations to align with Washington’s new trade and security frameworks. However, as history has shown, economic isolationism can backfire, as it did in the 1930s when protectionist policies deepened the Great Depression and undermined international cooperation.

Conclusion

Trump’s foreign policy represents a break from the multilateral traditions of the post-World War II order, favoring direct negotiations and economic leverage over alliance-based diplomacy. This shift echoes the compromises made at Yalta and the fragile peace efforts after World War I, both of which had long-term geopolitical consequences. If European nations do not take proactive steps toward greater autonomy in defense and diplomacy, they risk becoming passive participants in a new great power realignment. The historical lesson is clear: in an era of shifting alliances, European nations must assert their sovereignty or risk being dictated by external forces once again.

So, here’s the deal: Putin gets Ukraine and…Xi gets Taiwan, and Trump gets Canada, Greenland, and the Panama Canal? God help us.

The S&P 500 closed right at its 100-day on Friday. The Nasdaq bounced right off its 200-day. Stay tuned.

Firefly Aerospace’s Blue Ghost lander has successfully touched down on the Moon, making it only the second privately built spacecraft to achieve this milestone. The Texas-based company developed the robotic lander as part of NASA’s Commercial Lunar Payload Services (CLPS) initiative, supporting the Artemis program aimed at returning humans to the Moon.

Launched aboard a SpaceX Falcon 9 rocket, Blue Ghost spent two weeks orbiting before its hour-long descent to the lunar surface, landing this morning at 3:36 a.m. ET. The control room in Austin, Texas, erupted in celebration, marking another step in the growing private-sector involvement in lunar exploration.

The lander is carrying 10 NASA science instruments to study the Moon’s surface and interior. Among its tasks, it will:

While in orbit, Blue Ghost also captured stunning imagery of the Moon’s south pole and far side, providing valuable data for future missions.

This landing follows Intuitive Machines’ Odysseus mission in February 2024 and kicks off a wave of lunar expeditions. Another Intuitive Machines lander is set to land around March 6, while a Japanese ispace lander, launched alongside Blue Ghost, is on a longer trajectory, arriving in May or June.

NASA awarded Firefly $101.5 million for this mission, reinforcing private-sector contributions to lunar exploration and future human landings.

Source: NBC News

Check out the video of Firefly’s Blue Ghost lander, which captures stunning 10x-speed footage of the Moon’s far side and its thruster maneuvers from 100 km above the surface. Stunning.

This video image of our home from the moon never gets old. I have a framed print of Earthrise above my desk, which was taken by Apollo 8 astronaut William Anders.

Winston Churchill once remarked on his attentive relationship with President Franklin D. Roosevelt by saying,

“No lover ever studied every whim of his mistress as I did those of President Roosevelt.”

No doubt Putin and Xi scrutinize the current POTUS just as closely. But is the vigilance reciprocated?

Churchill called Roosevelt “Franklin” in private, reflecting their deepening friendship. In return, Roosevelt called Churchill “Former Naval Person” but later called him “Winnie.”

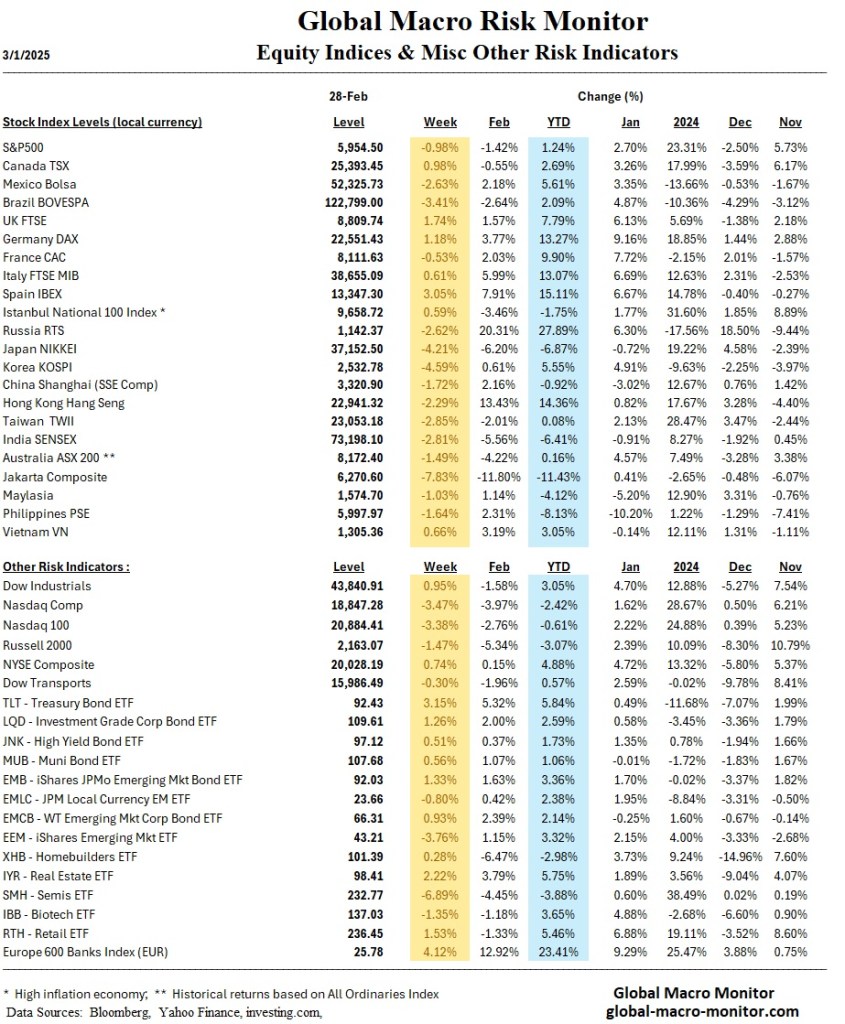

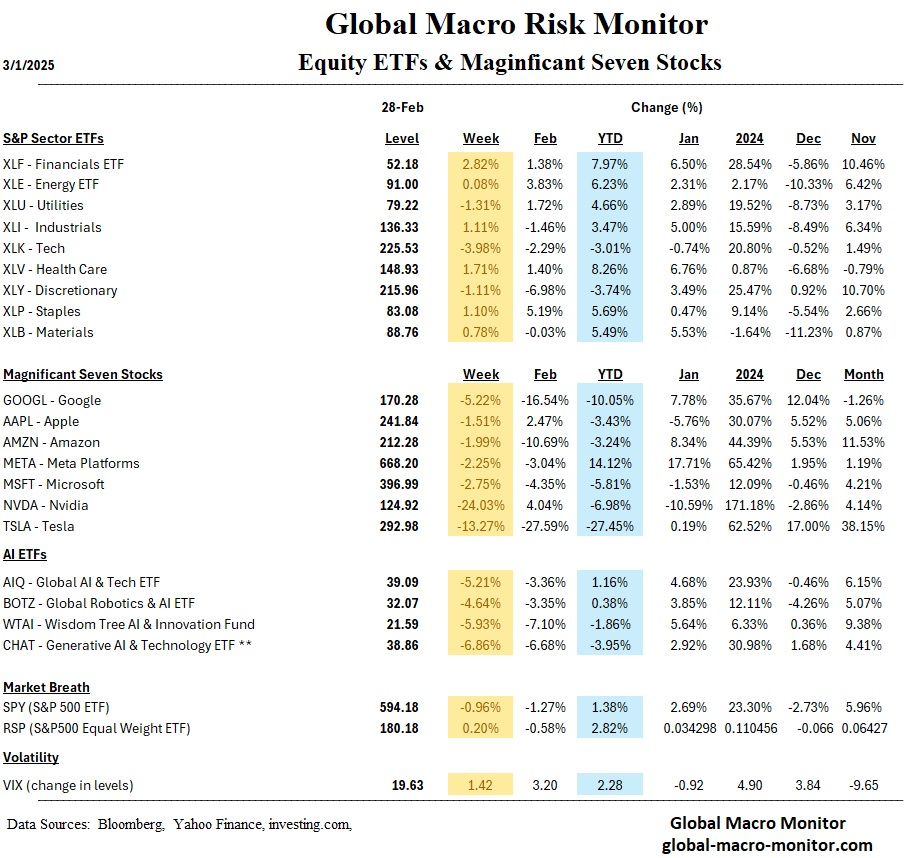

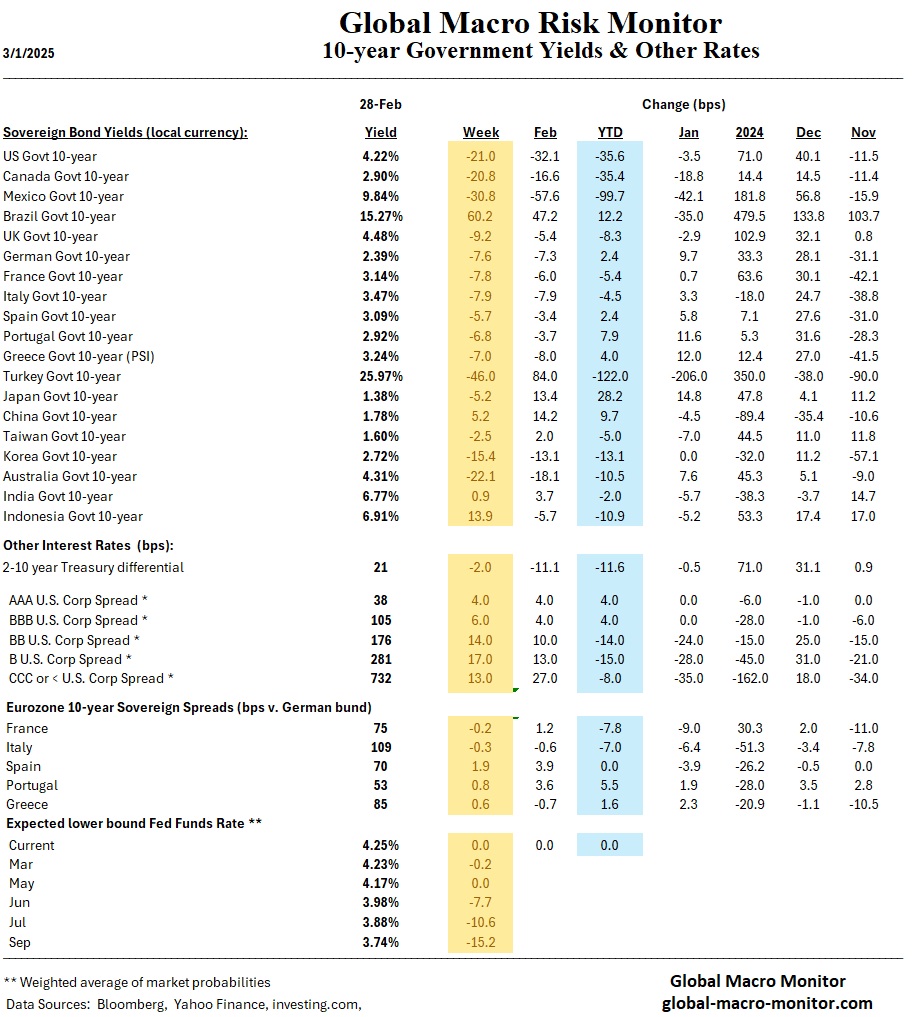

The past week saw heightened market volatility, with the S&P 500 and Nasdaq declining due to fading AI momentum and a growth scare, while the Dow Jones outperformed. The Atlanta Fed’s GDPNow model slashed Q1 GDP growth projections to -1.5%, signaling a potential contraction, exacerbated by weaker consumer spending and falling confidence levels. The bond market is flashing recessionary signals, as Treasury yields fell, and the yield curve remains inverted.

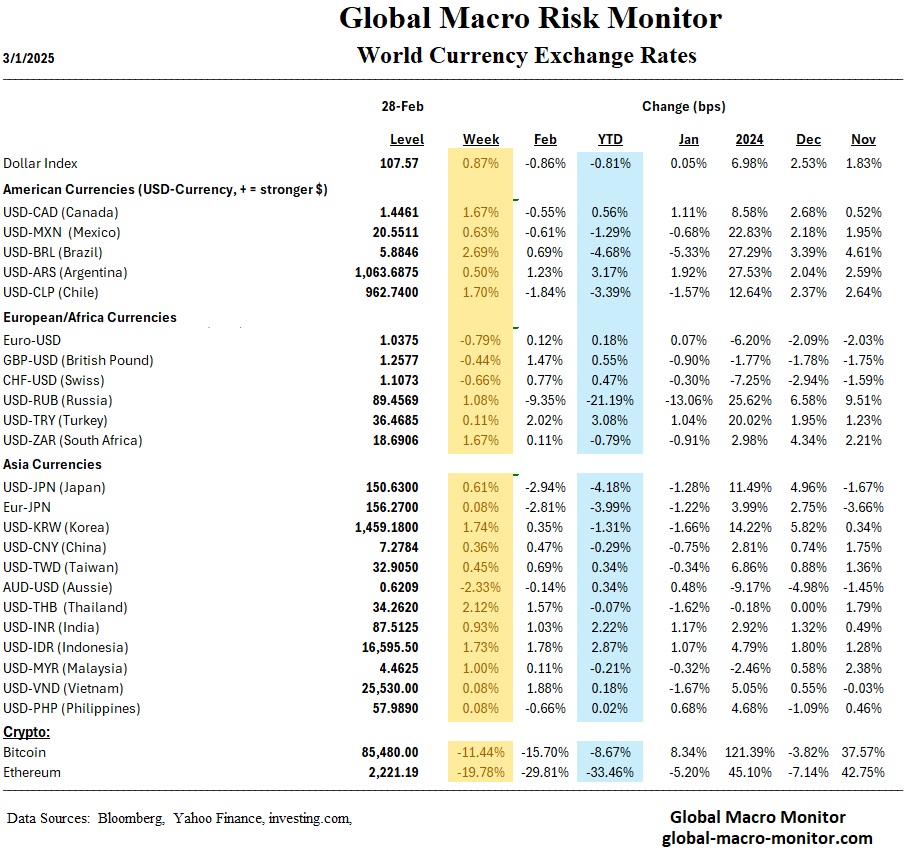

Brazilian markets faced sharp losses, with its stock market falling 3.41%, the real depreciating 2.7%, and bond yields surging 60 basis points amid concerns over rising interest rates and a shift to leftist populist economic policies. Meanwhile, Japan’s Nikkei dropped 4.21%, weighed down by a tech sell-off and U.S. tariff fears, while European equities posted modest gains.

Looking ahead, the market will focus on U.S. labor data, Fed rate expectations, and the March 4 tariff deadline. With risks rising, a defensive stance seems prudent, focusing on value stocks, liquidity, and hedging strategies.

Watch these levels, folks. This one feels like it is ready for a deep correction. Market volatility can signal instability before a major downturn, just like a speed wobble on a bicycle or motorcycle—when the handlebars start shaking uncontrollably before a crash. Sharp price swings, erratic sentiment, and liquidity imbalances indicate that investors struggle for control. While a deep correction often follows, sometimes markets regain balance if conditions stabilize. Volatility is an early warning, not a guarantee of collapse, but when the wobble intensifies, the risk of a full-blown selloff increases. Stay alert—key support levels will determine the outcome.