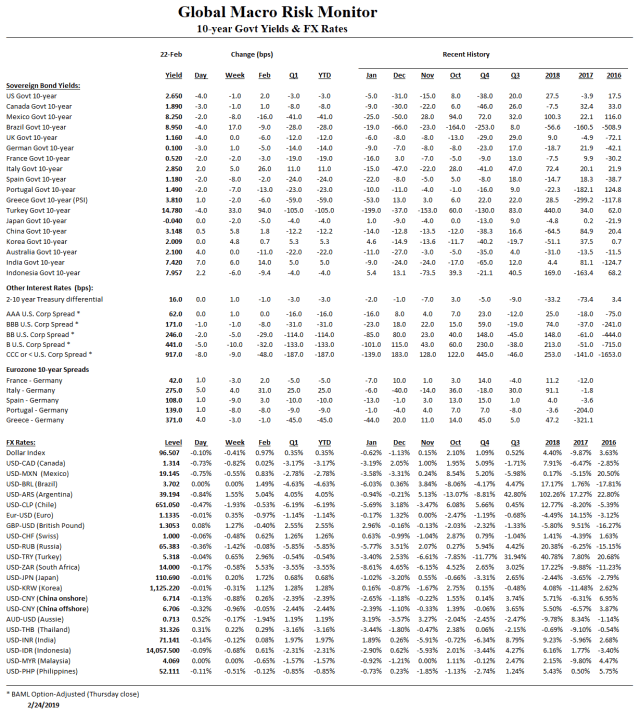

In what we consider one of our best and most timely all-time posts, The Gathering Storm In The Treasury Market 2.0, a must-read tome on the structural changes taking place in the U.S. Treasury market, we warned at the end of last September,

Crowding Out Begins

Therefore, it is no surprise, at least to us, global markets, beginning with the most vulnerable twin deficit EMs, are experiencing significant pressure from the crowding out caused by the U.S. Treasury’s massive increase in market borrowing.

U.S. Government Hoovering Up Global Funding

The following table illustrates the Treasury borrowed close to $1 trillion from the public in the first eight months of 2018, more than a trillion dollar swing from the same period last year. – GMM, September 24th

We also noted that the traditional buyers of U.S. Treasury securities were disappearing:

- The Treasury has to increase its market borrowing as the Fed rolls off its SOMA Treasury portfolio

- Social security has moved into deficit and borrowing from its trust funds to finance the on-budget deficits is over

- Globalization is under threat, and foreign capital flows into the U.S., particularly the Treasury market, are declining

We warned that long-term interest rates were about to spike, which they did breaking out to 3.26 percent causing the fourth quarter collapse in stocks. The one thing that Mr. Market really fears, in our opinion and inference from the price action, is a spike in long-term interest rates.

The sharp compressed collapse in stocks triggered haven flows and stock short sellers back into the Treasury market at the expense of other assets putting downward pressure on long-term rates. We did anticipate this,

All bets off given a geopolitical shock — we are concerned how quickly U.S.-China relations are moving south; a collapse in stock prices, or a sharp slowdown in economic activity. Haven flows will likely swamp the structural factors pressuring yields higher. – GMM, September 24th

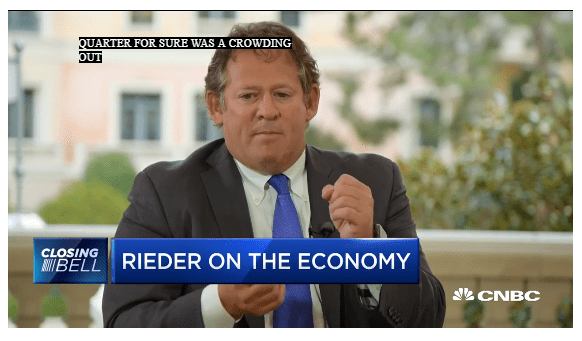

BlackRock Weighs In

Today, in an interview with CNBC, the well respected Rick Rieder of BlackRock confirmed our analysis, albeit after the fact,

By the way, the thing we saw in the last quarter for sure was a crowding out effect. When the Treasury has to issue an immense amounts of debt, it crowds out. We saw this play out in December in a profound manner. That what happened was interest rates moved up and people say gosh I could be in the two-year Treasury at 3 percent, why do I need to buy high yield, why do I need to invest in equities. There is a crowding out dynamic that is profound. When people say, gosh, I think we can absorb more debt in the country, I think that is a very dangerous thing. – Rick Rieder, BlackRock, Feb 26th (6:48 minutes)

Click here for the full interview

Treasury Warned Foreign Buying Drying Up

In their end-January report to the Steven Mnuchin, the Treasury Borrowing Advisory Committee of the Securities Industry and Financial Markets Association (TBAC) also raised concerns of the structural changes taking place in the marketplace,

The Committee next discussed a charge on potential innovations in Treasury products and tools. The presenting member estimated borrowing needs to exceed $12 Trillion without factoring in the possibility of a recession which would pose a unique challenge for Treasury over the coming decade. Additionally, given stagnation in international reserves, there is likely an increased need for this debt to be financed domestically. – TBAC, Jan 29th

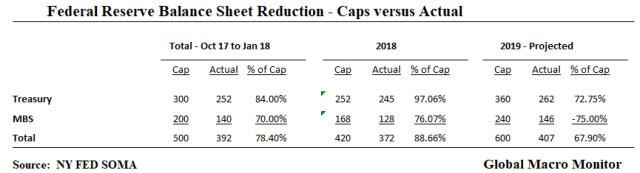

The Fed’s Balance Sheet Run-off

We noted in several posts that quantitative tightening (QT) is more of a fiscal event than a monetary one as it has had almost no impact on credit and loan creation but has greatly increased the size of the monthly Treasury auctions and thus “crowding out” other asset markets. We have also posted several pieces on how the market has it wrong on the actual amount of the annual balance sheet roll-off.

The market still seems obsessed with the $600 billion number ($50 b per month) which drives the animal spirits, price action, stock market volatility, and ultimately the Fed. The December stock market volatility caused the Fed to effectively change their dual mandate in January to support the S&P and Nasdaq, after extreme pressure from the “Market Socialists” led by Mr. President, Mr. Market, and Mr. Cramer. Ergo an earlier exit from its balance sheet reduction.

The Fed does not know the correct level of reserves that should be in the financial system, nor does anyone else, and Jerome Powell admitted so in his last press conference. Note the emphasis on “unnecessary market turmoil.”

…so the Committee is—what we’re looking to do is create a whole plan that will bring us to our goal, our longer-run goal, which is a balance sheet no larger than it needs to be for us to efficiently conduct—efficiently and effectively conduct monetary policy, but to do so in a way that doesn’t put our goals at risk or result in unnecessary market turmoil. So there are a lot of pieces to that, and we’ve learned over time that it’s—when making these—when designing these plans, like, for example, the original normalization plan, it’s good to take your time. Let the best ideas rise to the top. – Chairman Powell, Jan 30th

We agree the level of reserves certainly should be higher than before the crisis as banks won’t quickly forget their near-death experience and runs on liquidity.

Katy bar the door, however, if the financial system normalizes and bank credit takes off with all the “high powered money” out there.

Nevertheless, the quicker the end of QT the less pressure on Treasury funding, diminishing, on the margin, of impact of the crowding out effect. Probably, a major motivation for the Fed to reverse course. I have confidence they get it but yet down another rabbit hole we go.

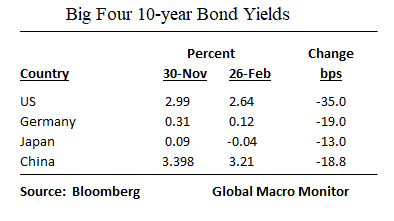

Upshot

Markets have recovered smartly as long-term yields of the Big Four have moved down sharply since the end of the November, some due to global growth downgrades and some the result of haven flows.

Negative yielding debt throughout out the world is all the rage again and thus provides an anchor for U.S. Treasury yields.

Negative-yielding government bonds outstanding through mid-January have risen 21% since October, reversing a steady decline that took place over the course of 2017 and much of last year, according to data from Bank of America Merrill Lynch. While the stock of negative-yielding debt still remains below its 2016 high, the proliferation of these bonds—which guarantee that a purchaser at issuance will receive less in repayment and periodic interest than they paid—underscores the uncertainty over the growth prospects in much of the developed world. – WSJ, Feb. 18th

Seriously, Cyprus funding itself with negative yielding 13-week Treasury bills? The country that blew up its banking system and bailed in large depositors just six years ago? Europe, potentially on the eve of another existential crisis, and Cyprus with negative yields? You have got to be shitting me.

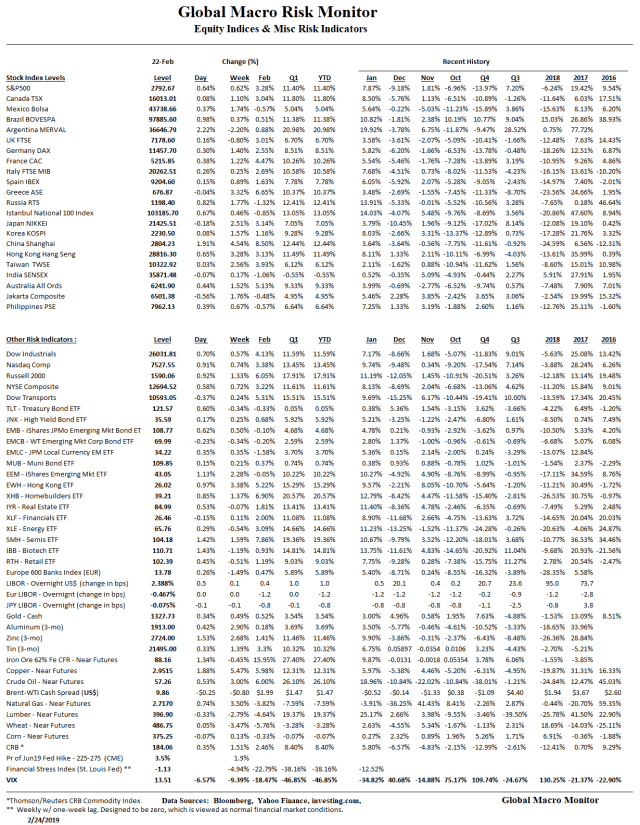

What, I ask my EMH brothers and sisters, are markets signaling with Cypriot 13-week bills yielding -0.10 percent and similar U.S. bills yielding 2.39 percent? What is the “message of the market” of you still believe in markets?

China Trade Deal

There is also the now all priced in China-U.S. trade deal. Unless economic activity collapses, which doesn’t seem to be what the commodity markets are signaling, it’s going to be harder for rates to move much lower. The easy money has been made.

Total Public Capitulation On Debt And Deficits

We find it ironic, and a bit disconcerting, the Q4 stock flop, was caused by the rise in real yields resulting from rising deficits and the diminishing demand of traditional Treasury buyers at the same time we hear many have learned to love the bomb ballooning budget deficits.

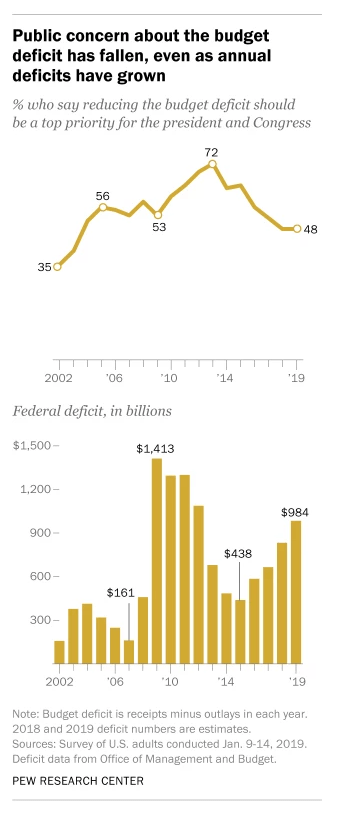

The above chart is yet another indication the country is shifting left. No judgment, no political statement, just an observation, and one that investors should keep on their radar.

We also recommend the market pundits and geniuses do a better autopsy on the Q4 stock market crash. Don’t just blame the lack of liquidity in December but ask and explain what triggered the initial selling impetus.

More startling is that a growing, more than a boys chorus now believe a significant increase in government spending can easily be financed by the Fed ala the printing press as long as it doesn’t cause inflation — enter MMT. True, just as an increase in the consumption of, say, opioids are beneficial as long as it doesn’t cause addiction.

Time to be patient and wait for lower prices, folks. It’s getting more and more Kafkaesque out there, everywhere. Public debt has become so large and ubiquitous, sovereign yields in many G20 countries can’t clear and move to their true equilibrium level lest the world blows up. We got a glimpse of the window into the future with the stock market crash in Q4 2018.

Some are betting Modern Monetary Theory (MMT) can, will, and is about to abolish the crowding out effect.

There is no doubt, in our book, how this movie ends. The trick is to determine how long it lasts.

Finally, as always we reserve the right to be wrong. Strong convictions, weakly held, comrades!