U.S. job growth slowed, with weaker-than-expected payrolls but a declining unemployment rate.

Stock markets fluctuated due to tariff uncertainties, with Trump postponing tariffs on Mexico and Canada but maintaining those on China.

Strong corporate earnings supported equities, with the S&P 500 showing 16.4% earnings growth versus 11.9% expected.

U.S. Treasury yields declined, pricing in slower growth and potential Fed rate cuts.

Eurozone inflation remains sticky, delaying European Central Bank rate cuts.

Japan’s hawkish policy stance strengthened the yen, impacting exporters.

China’s retail and travel data showed strong Lunar New Year spending, but manufacturing PMI indicated slower growth.

Markets

Stocks

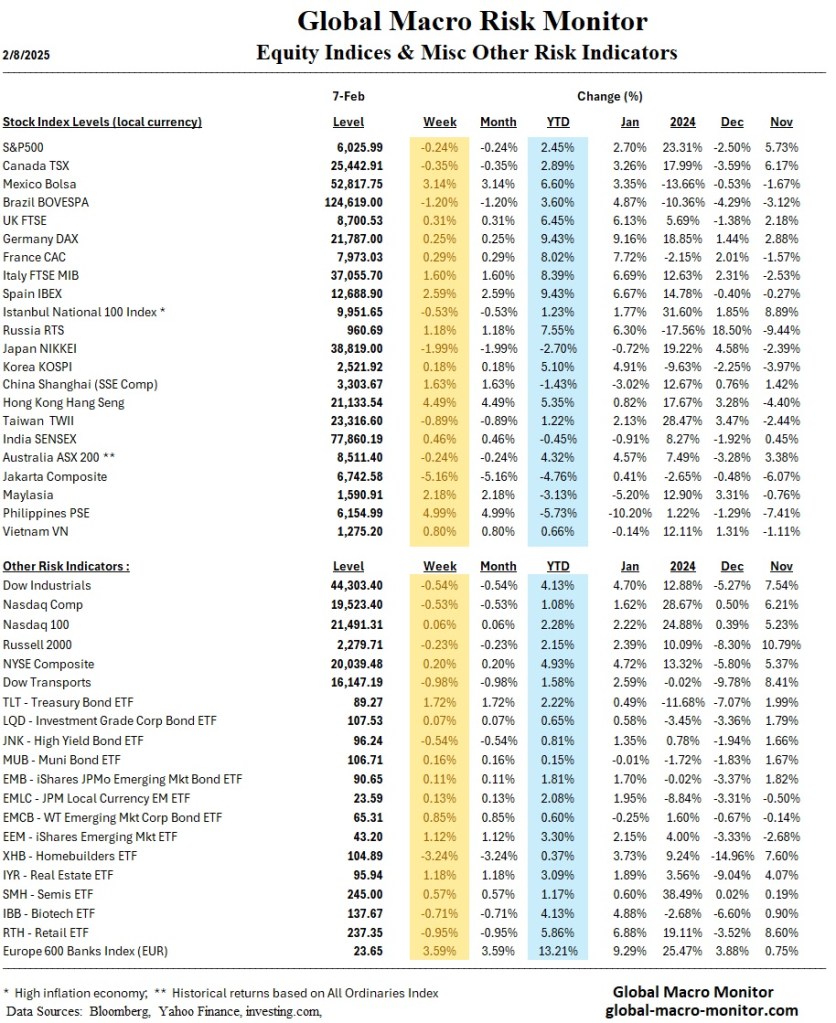

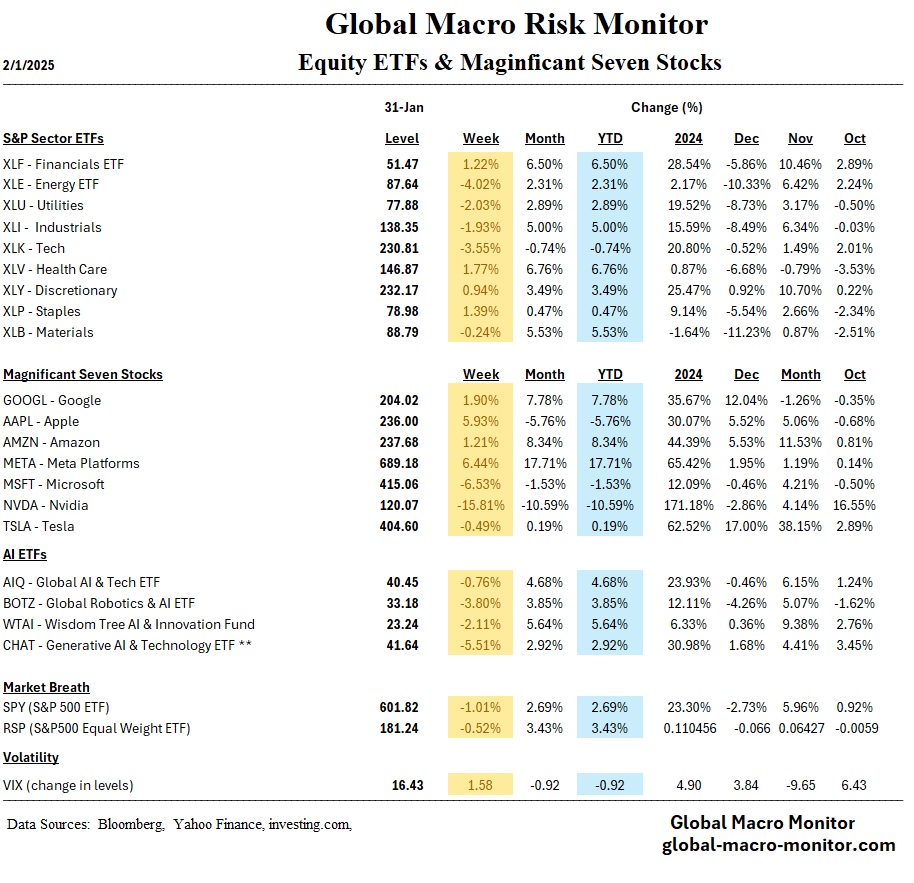

Markets experienced a volatile week as investors reacted to trade policy developments, economic data, and earnings reports. U.S. equities opened lower following the White House’s announcement of sweeping tariffs on imports from Mexico, Canada, and China. However, stocks rebounded after President Trump postponed tariffs on North American trade partners, easing fears of an imminent trade war. The S&P 500 declined 0.24%, while the Dow Jones Industrial Average and Nasdaq Composite also finished in negative territory. Strong corporate earnings helped limit losses, with 77% of S&P 500 companies surpassing expectations.

Globally, European stocks posted gains, with Italy’s FTSE MIB rising 1.6% and Germany’s DAX up 0.25%. Japan’s Nikkei 225 fell 2%, pressured by a stronger yen as the Bank of Japan (BoJ) shifted to a more hawkish stance. China’s Shanghai rose 1.63% in a shortened trading week, bolstered by robust Lunar New Year spending despite weak PMI data.

Bonds

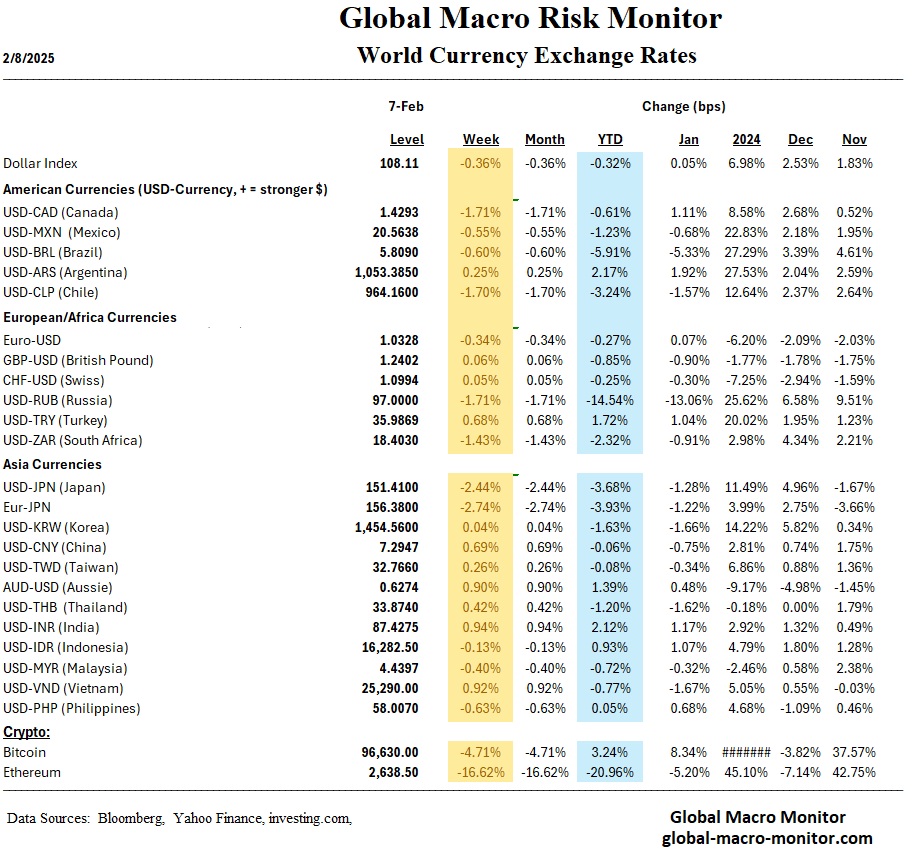

U.S. Treasuries rallied as weaker-than-expected jobs data reinforced expectations of a dovish Federal Reserve. The 10-year Treasury yield fell to 4.50%, reflecting concerns over slowing growth. Municipal bonds and investment-grade corporate debt saw strong demand, with high-yield issuance remaining active. In Europe, the Bank of England cut rates by 25 basis points, while the Czech National Bank also eased policy but signaled caution moving forward.

United States

The U.S. labor market showed signs of gradual cooling, with 143,000 jobs added in January, well below December’s revised 307,000. However, the unemployment rate fell to 4.0%, suggesting underlying resilience. Job openings declined to a three-month low, reinforcing the view that hiring is stabilizing. Wage growth accelerated, with average hourly earnings rising 0.5%, which could complicate inflation control. Meanwhile, manufacturing PMI expanded for the first time in over two years, but business sentiment remained fragile amid ongoing trade policy uncertainty.

International

Europe’s economy presented a mixed picture. Eurozone inflation remained elevated at 2.5%, delaying expectations for European Central Bank (ECB) rate cuts. Germany’s factory orders surged 6.9%, but industrial production declined, highlighting economic imbalances. The Bank of England cut interest rates for the third time since August, citing slowing growth and persistent inflation risks.

In Asia, Japan’s BoJ signaled a more hawkish stance, strengthening the yen and pressuring exporters. China’s economy showed resilience in consumption, with Lunar New Year retail spending up 7% and travel demand hitting record levels. However, manufacturing PMI indicated slowing production growth, raising concerns over longer-term economic momentum.

Week Ahead

Looking ahead, tariff negotiations remain a key market driver, with potential trade developments between the U.S., China, Mexico, and Canada likely to impact sentiment. Investors will also watch inflation data, with the Consumer Price Index (CPI) and Producer Price Index (PPI) due next week. The Federal Reserve’s policy stance will continue to be a focus, particularly as market expectations for a 2025 rate cut cycle evolve. Meanwhile, corporate earnings season continues, with major reports from firms in the technology, consumer, and industrial sectors.

Global attention will also be on central bank decisions in emerging markets, particularly Turkiye, Poland, and Czechia, as policymakers navigate inflationary pressures. In Latin America, Ecuador’s elections will be watched for potential policy shifts amid regional political uncertainty. With markets navigating geopolitical risks, economic data, and corporate earnings, volatility is likely to persist in the near term.

Across the globe, in the United States and Uruguay, in Italy and India, families are getting smaller. To some, this may seem like good news. In an era of human-induced climate change, it’s hard for many liberal, environmentally minded people to rally around having more children — harder still for many young Americans of all political stripes to imagine raising and supporting three children when rent can eat nearly a third of their paycheck.

But economists, demographers and government leaders are increasingly alarmed about the downward trend. According to the latest United Nations projections, the world’s population will peak in 60 years. After that, experts say, humanity will face an unprecedented decline — and, along with it, profound social and geopolitical consequences.

The average fertility rate in the United States has not been above the 2.1 replacement rate since 2007, according to World Bank data. Currently, no country in the developed world, barring Israel, has a fertility rate above replacement level, and, based on U.N. projections, by the end of the century, almost every country will have a shrinking population.

A McKinsey report exploring falling fertility rates says that the trend is “propelling major economies toward population collapse in this century,” pushing society into “uncharted waters.” Think empty schools and crowded retirement homes; dwindling Social Security; and a voting public that skews far older than generations past. Further down the line, shrinking populations could spur mass migration and new global conflict. – Washington Post

Today is Groundhog Day, and it feels like it, with the Trump Administration starting another trade war. This war will end when the countries appear to make some minimal concession so the president can declare victory. Or maybe this is the big kahuna.

Recall during his first administration NAFTA was tinkered with to allow the president to declare:

The USMCA is the largest, most significant, modern, and balanced trade agreement in history. All of our countries will benefit greatly. – Donald J. Trump

The IMF analysis of that deal was essentially, “big hat, no cattle.”

Chalk up another meaningless, photo-op trade agreement with the recent U.S.-Japan Trade Agreement. The country and, especially, American farmers would have been much better off staying in the Trans Pacific Partnership (TPP).

The Japan deal is just another Potemkin trade agreement that will not move the needle one centimeter in bringing jobs back to the United States as was promised.

The dominant loop in the algo to predict President Trump’s behavior with respect to just about everything is to reject all things Obama even if it damages the country. It’s really not rocket science, folks.

If you’re looking for evidence that a U.S.-China trade agreement is a pointless exercise in economic futility, consider Donald Trump’s non-deal with Japan.

…Late last month, he [Abe] gave Trump a “deal.” That, Trump figured, would enable him to claim a much-needed win on the global stage and get his impeachment troubles out of the headlines. Knowing this, Abe’s team skillfully watered down the deal—essentially to TPP levels. All it means is that U.S. farmers missed out on nearly three years of increased access to Japan, Australia, Singapore, Malaysia, Chile and elsewhere.

Yes, the man famed for the ghostwritten bestseller Art of the Deal got played by Japan’s negotiators. And soon, Xi Jinping’s trade team will be able to make the same boast. Any U.S.-China deal will be a cosmetic affair that gives Trump a “win” and President Xi clearance to make China’s rise great again.

Trump is desperate for a face-saving way to end the trade war. Fallout on U.S. farmers and consumers paying higher import prices is imperiling Trump’s reelection odds for 2020. Yet backing down to Beijing would create its own problems with Trump’s base. Xi’s men are well aware of this, just like Abe’s. – Forbes, Oct 8th

We have been very critical of the Administration’s trade policy simply because there is none.

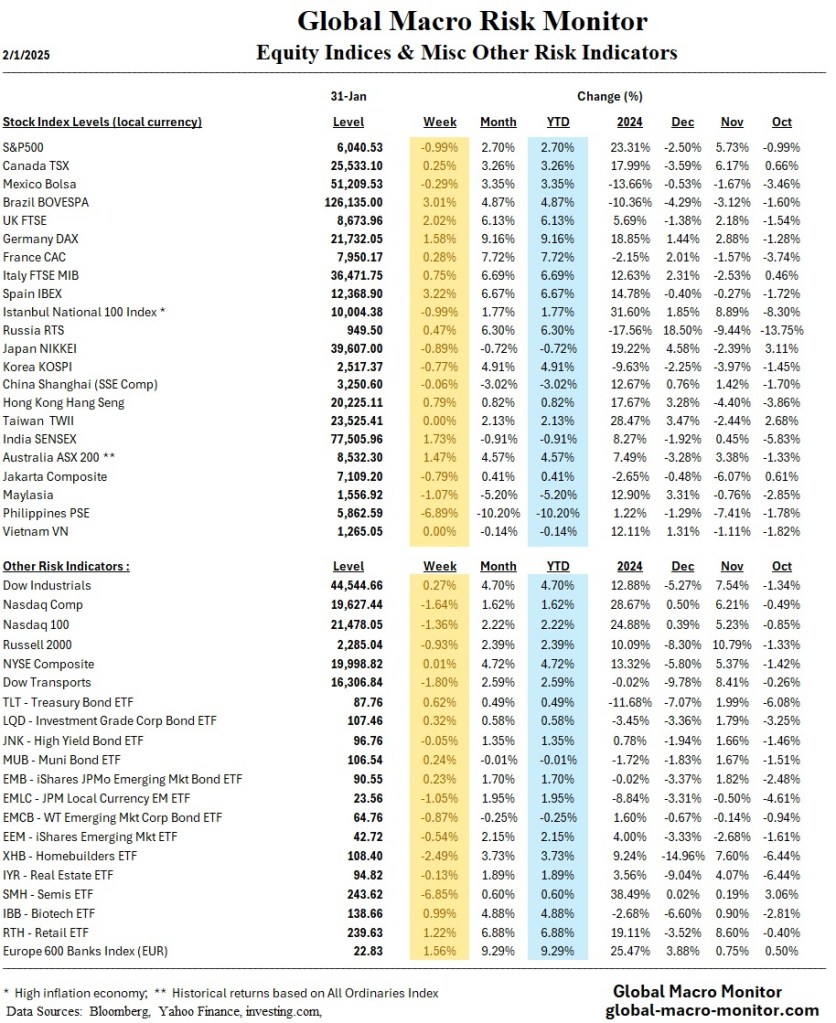

The financial markets are poised for heightened volatility following President Donald Trump’s decision to impose broad tariffs on Mexico, Canada, and China. The move, which includes a 25% tariff on imports from Mexico and Canada and a 10% tariff on energy imports from Canada and goods from China, has injected uncertainty into global trade relations. Investors now face two key risks: potential retaliation from U.S. trading partners and the impact on inflation, corporate earnings, and economic growth.

Markets typically react swiftly to major geopolitical and policy shifts before evaluating the long-term consequences. While some may view the tariffs as an aggressive opening stance in negotiations, markets tend to “shoot first and ask questions later.” The latest measures come at a time when global growth is already fragile—China’s economic data showed contraction across multiple sectors, and the eurozone reported stagnation in Q4 GDP.

Market and Economic Recap (Week Ending January 31, 2025)

Equity Markets: U.S. stocks were volatile, with the Dow Jones rising modestly for the third consecutive week (+120 points) while the S&P 500 (-60 points) and Nasdaq (-326 points) faced losses. Tech stocks were particularly hit after AI competition concerns from DeepSeek.

Federal Reserve Policy: The Fed held rates steady at 4.25%-4.50%, signaling patience in policy adjustments. Core PCE inflation remained at 2.8% YoY.

Economic Growth: U.S. GDP grew at 2.3% in Q4 and 2.8% for the full year, slightly below expectations but ahead of long-run forecasts.

Fixed Income Markets: Treasury yields fell for most of the week but rebounded after the tariff announcement.

Earnings Season: Roughly 40% of S&P 500 firms reported, with notable earnings beats from Meta and Apple, while Microsoft and Tesla provided mixed results.

European Markets: The ECB cut rates by 25 basis points to 2.75% amid weak eurozone growth.

China’s Economy: PMI data pointed to worsening conditions across manufacturing, services, and construction.

Market Outlook: Higher Volatility Ahead

The immediate concern is whether this tariff escalation will lead to retaliatory measures from Canada, Mexico, or China. If so, supply chain disruptions and inflationary pressures could prompt renewed Fed scrutiny. Investors should brace for increased volatility in equity and fixed income markets as the implications of Trump’s tariff strategy unfold.

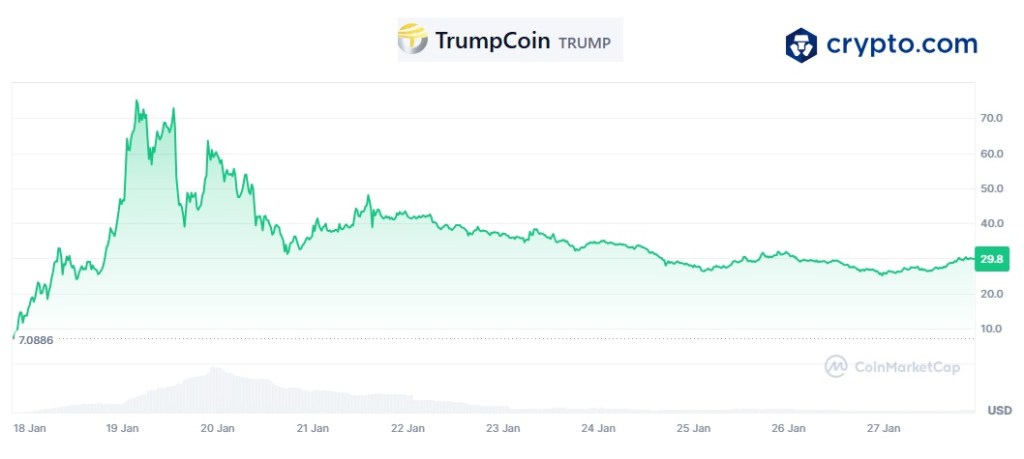

The launch of $Trump, a cryptocurrency unveiled during President Donald Trump’s inauguration festivities, has stirred both excitement and skepticism, shining a harsh light on the flaws in the cryptocurrency market. Promoted as a revolutionary token, $Trump initially surged to a $15 billion market cap within hours, only to lose over half its value days later. For critics like Global Macro Monitor, the $Trump saga epitomizes why cryptocurrencies lack credibility: they have no intrinsic value and fail to meet John Maynard Keynes’ definition of a currency—1) a store of value, 2) a medium of exchange, and 3) a unit of account.

A Gimmick-Driven Launch

Announced during the star-studded Crypto Ball, $Trump entered a market already rife with speculation. Backed by a Trump-affiliated entity controlling 80% of the supply, the memecoin promised supporters a way to share in the “crypto revolution.” However, the launch was followed swiftly by Melania Trump’s competing token, $Melania, and later by the Reverend Lorenzo Sewell’s $Lorenzo coin, introduced just hours after his inauguration benediction. Sewell, a Detroit pastor, pitched $Lorenzo as a funding tool for charitable initiatives, only to see its value spike briefly before collapsing—mirroring $Trump’s trajectory.

The ease with which these tokens were minted highlights the fundamental problem with crypto scarcity. While Bitcoin is touted as “digital gold” due to its fixed supply, the flood of memecoins—ranging from $Trump to celebrity coins like $LeBron (LeBron James) and $Leo (Leonardo DiCaprio)—reveals that cryptocurrencies can be created out of thin air, eroding the foundation of the investment thesis tied to scarcity.

A Questionable Wealth Boom

The broader cryptocurrency market now exceeds $3 trillion in capitalization, creating vast wealth for some without producing anything of tangible value. This speculative boom is undeniably inflationary on the margin, as money flows into unproductive assets rather than contributing to real economic output. For Global Macro Monitor, this wealth accumulation, untethered to intrinsic value — or a value anchor, for that matter — amplifies concerns about cryptocurrencies’ long-term sustainability.

Failing Keynes’ Test of Currency

While Bitcoin enthusiasts argue that crypto represents financial innovation, it fails Keynes’ test of currency. Its extreme volatility makes it a poor store of value, few merchants accept it as a medium of exchange, and its fluctuating prices undermine its role as a unit of account. The chaotic launches of $Trump and $Lorenzo only exacerbate these weaknesses, reducing the market to a speculative playground.

Industry and Public Reactions

Critics within the crypto community were quick to decry the $Trump coin. Nic Carter, a Trump supporter and crypto investor, called the move a cash grab that undermined the industry’s credibility. Ethereum creator Vitalik Buterin went further, warning that political and celebrity coins are tools for manipulation and a threat to democracy. Social media backlash was swift, with many accusing the Trump family of exploiting their positions for personal enrichment while tarnishing the industry.

Despite the controversy, the Trump administration continues to champion crypto, with executive orders aimed at easing regulations. Anyone counting on regulation to bring stability should think again. The next four years in the cryptocurrency market are set to make the “Wild West look like a Sunday picnic,” as new tokens and speculative ventures flood the space, testing the limits of both investors and regulators. In addition, the crypto industry is hoping for a “takeout” by the U.S. G. by means of the creation of a U.S. Bitcoin strategic reserve.

A Cautionary Tale

The $Trump coin also highlights the fragility of the cryptocurrency market and the dangers of unregulated speculative assets. For Global Macro Monitor, cryptocurrencies’ lack of intrinsic value and inability to function as currencies per Keynesian theory make their long-term appeal dubious. That said, we do trade Bitcoin, recognizing its unique position as the most established cryptocurrency and the trading opportunities it presents.

The fundamental value of Bitcoin is ambiguous at best and entirely untethered to any notion of “fair value.” There is no fair value because there is no intrinsic value. Price is dictated purely by flows, driven by investor and trader psychology, with no underlying anchor to ground it. As a result, Bitcoin’s price can go anywhere—soaring to unimaginable highs or crashing just as quickly—because it is detached from any tangible economic or financial foundation.

Still, the $Trump saga serves as a sobering reminder that without foundational reforms—and perhaps even with them—cryptocurrencies may remain financial mirages rather than revolutionary innovations.

Nevertheless, at the end of the day, what ultimately matters to the crypto industry and its investors can be summed up by paraphrasing the late Al Davis, former owner of the Oakland Raiders:

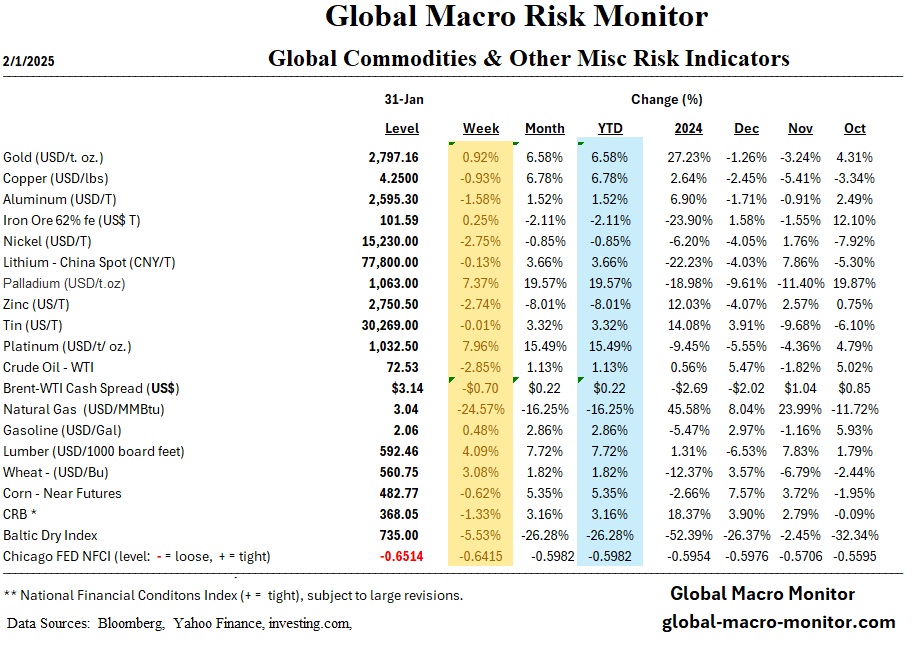

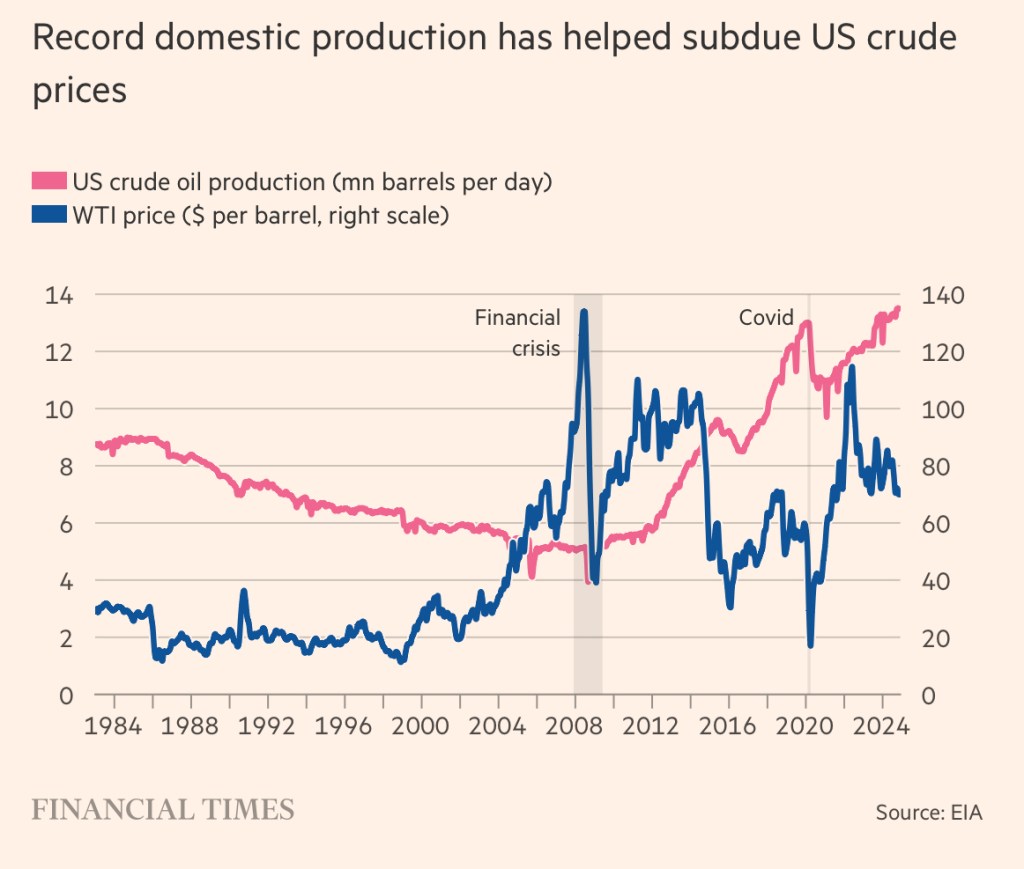

But weak global demand and market caution could deter investment in additional supply. “The oil and gas industry is reluctant to produce more than global markets can absorb right now. Precisely because they know that will cause commodity prices to drop sharply,” said James Lucier, managing director at Capital Alpha Partners, adding that there was “quite a lot of market discipline” constraining fresh drilling. – FT