Because we get a lot of things wrong in the trading business as nobody knows the future, and every decision to buy or sell is really just a probability adjusted or calculated guess, we thought we would take a victory lap on a few of our calls this year. We backed these calls with real money.

The Midterm

We are students of politics, as all traders should be, and constantly trying to sense the mood of the body politic, keeping our political bias at bay. Note we predicted Trump would win the electoral college and HRC would win the popular vote the night before the election. We know of no one making that specific prediction.

Took a lot of heat in our household on election night, as it was our fault!

Our February Midterm Bet

Because so many allow emotions to cloud their judgements and base their opinions on noise from political pundits, it is easy to pick off the gullible.

Here is a bet we made with a Trump supporter waaaaaay back in February that the Dems would take more than 36 House seats. Many large institutional investors would know our counterparty’s name:

On Feb 27, 2018, at 6:10 AM, P…… <> wrote:

I’ll bet better than average for $100

From: G…. <>

Sent: Tuesday, February 27, 2018 6:15 AM

To: P

Subject: Re:

Done. P…. = less than 36 loss; G.. > 36. Push at 36.

Sent from my iPad

He just conceded yesterday. It looks like Dems are going to flip 37-39 House seats.

Our friend was betting Trump would weather the midterms based on the strong economy. We knew the day after the Inauguration, with hundreds of thousands women marching in the street, the XX chromosome demographic, who are the majority and more likely to vote, had woke and their energy and revulsion toward the president would carry into the midterm.

President Trump’s polling numbers with women was the political metric we followed the most over the past 18 months.

The Lavender Wave & Political Earthquake

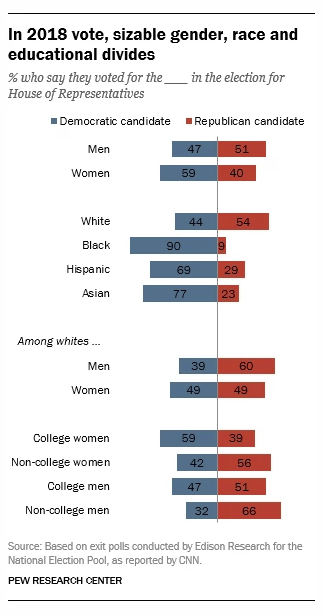

We posted several pieces on the Lavender Wave, that is combination of pink (women) and blue (Democrat), sweeping the Republicans from the House.

Look for the wave to crest and break in early November when women and millennials, in general, come to the polls in droves to express their revulsion for President Trump. No level of the S&P or GDP growth will matter. – GMM, Sept 4th

Also see here and here.

Our model based prediction came in right on the money,

Dems Likely To Pick-up 27-47 House Seats

Our prediction is based, not on our personal politics, but on inference from the polling data, history, and simple factor models. Recall, we predicted Trump would win the electoral college and Clinton, the popular vote, on the eve of the 2016 election. – GMM, October 9th

Though to be honest, our model did increase the upper end of the range after President Trump began to tank in the polls in the last few weeks before election day,

President Trump enters the week before the midterm election with the lowest approval rating of any full first-term president in modern day polling — 4 points below President Obama before losing 63 House seats in 2010, and 6 points lower than President Clinton before losing 54 House seats in 1994.

The presidential approval model predicts the Republicans are set to lose 53 House seats next Tuesday. – GMM, October 29th

Clock Cleaning

Though many looked at the headlines on election night and were disappointed their long-shot bets – Beto, Stacy, and Andrew Gilliam – lost, the Republicans got their clock cleaned.

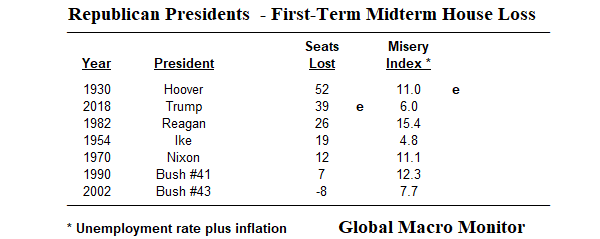

President Trump lost the most House Seats of any first-term Republican president since Herbert Hoover, who was sitting on an economy sliding fast into the Great Depression. Conversely, President Trump lost 40 House seats with a strong economy boasting a Misery Index of just 6.0, the second lowest of any recent president in his first-term.

Unless power changes from one party to the other or puts one party over the 60 vote threshold, Senate pickups are pretty marginal and signify little. It was historic, however, in that the Republicans picked up Senate seats while losing the House.

It was the first time since the nation started directly electing senators in 1914 that a party has won control of the House without gaining seats in the Senate. – USA Today

We have been pounding the table for months about how a Lavender Wave – women voting Democrat – would determine the outcome of the midterm. The wave crested on election day and swept Republicans from the House. The 2018 midterm was the Year of the Woman, and their slogan?

Exit the BREXIT

So, folks, how many analysts do you know who were predicting after the American political earthquake pressure would build in the U.K for a second referendum on BREXIT? You certainly did here:

BREXIT ain’ gonna happen. The political extremes on both ends have “woke” the sleepy and complacent middle, women, and the young. We believe you will see the results in the upcoming “November to Remember” midterms.

A second vote on BREXIT is an uphill battle, but if the Trump administration gets “bitch slapped” in the November midterms the momentum and pressure for a new BREXIT vote will build, in our opinion. – GMM, October 20th

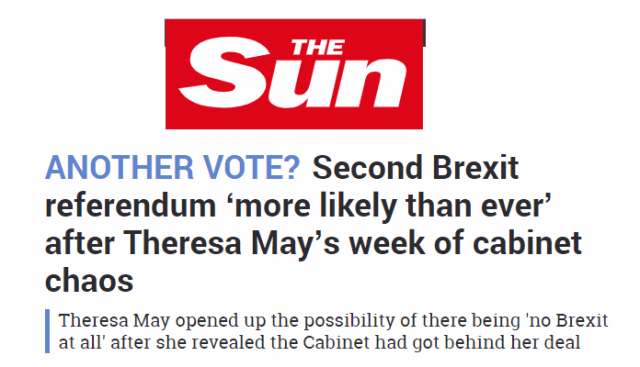

Exit the BREXIT is hardly a done deal but we direct you to today’s headline in The Sun.

Politicians are no more than weathervanes of popular opinion, which is especially true in a parliamentary system, such as the U.K. Unlike America’s political system, particularly its archaic electoral college and upper chamber, the Senate, where the tyranny of the minority can, and often, do rule.

The total cumulative population of the bottom twenty least populated states in the U.S. have 40 votes in the Senate, for example, whereas California, with the same population as the bottom twenty, only has two votes in the Senate. Is that a fair and democratic way to pick, say, Supreme Court justices, the third branch of the American government, for example? Just askin’.

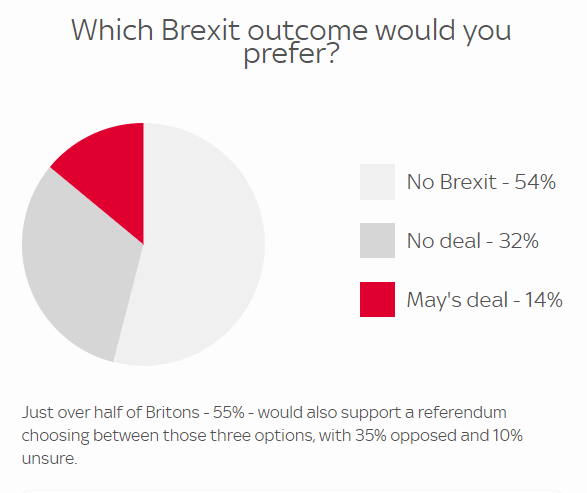

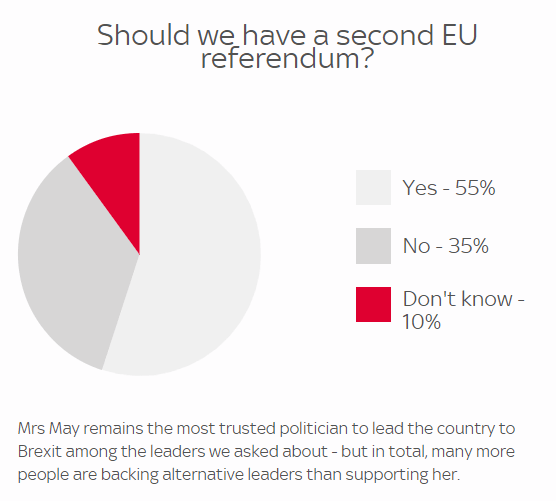

Polls Moving Against A BREXIT

Nevertheless, check out the latest polls on BREXIT in the U.K.. The pressure for a second vote on BREXIT is going to grow and about to get intense. We wouldn’t bet against the U.K. staying in the European Union.

Source: Sky Data poll

Will the British pols thwart the will of the people?

We seriously doubt it, especially given that British policymakers seem to have no idea what the hell to do on this issue.

We stand by our prediction. No BREXIT

Apple

Finally, you know we have been critical of Apple’s strategy of driving revenues through inflating iPhone prices and strongly believe it is unsustainable.

Apple’s market cap hit 1012 dollars today.

Impressive but no pom-poms here at Global Macro Monitor. We would be more impressed if Apple’s main businesses were doing better and the company was more focused on electrical engineering rather than financial engineering. – GMM, August 2nd

Apple continues to rely on iPhone inflation for revenue growth as unit sales quarterly year-on-year growth was flat for the 12th consecutive quarter. The almost 30 percent increase in iPhone revenue is due to price increases.

…Assuming, for example, iPhone prices rose at the rate of inflation of 3 percent (and, of course, assuming away quality upgrades), the company revenues would have increased by only 5.7 percent instead of 20 percent.

Relying on price increases is not sustainable and may be why the stock is taking a beatdown after the close.

…We suspect if unit sales do not increase this holiday season, the stock could be in trouble. Just our calculated guess. – GMM, November 1st

The Street is coming around to our view and the stock is under pressure.

We received this email from a golf buddy and friend a few days ago.

Johnpaul <>

Wed 11/14/2018, 7:45 PM

You

G…, hope you’re doing well. Just wanted to let you know that in early August you gave me some advice on Apple stock shares I was holding. You said despite Apple’s recent share price run up Apple relied heavily on their iPhones sales making them a “one trick pony” and very vulnerable long term. I took your advice and sold my shares of Apple. Glad I did. Thanks!

JP 🙏😊

Sent by my Labrador

Always feels good to help a friend save a few bucks ($30-40 per share to be exact).

Upshot

There you have it folks.

We could add more, such as our calls where we stood alone on various issues: China trade, the Taiwan Strait, Trump and North Korea, the U.S. Treasury market, just to name a few. Many of our views are now becoming conventional wisdom.

We could lay out many of the calls we got wrong, especially the call on a stock bear market earlier this year, though we believe we were just early. But you must admit, we provide a different perspective and angle on the economy, the markets, and current events.

This is exactly why the Global Macro Monitor is must read. Turn off the cheerleaders and stay tuned.