Farmworker Justice estimates that 70 percent of farmworkers are immigrants (about 40 percent of which are undocumented). Within agriculture, crop production employs the most immigrants (59 percent of farm laborers) while approximately 45 percent of livestock workers are foreign-born.- farmsaid.org

The S&P 500 CAPE (Cyclically Adjusted Price-to-Earnings) ratio, a metric developed by economist Robert Shiller, measures stock market valuation by averaging earnings over the past ten years and adjusting for inflation. It provides a long-term perspective on whether the market is overvalued or undervalued compared to historical norms. As shown in Charlie Bilello’s most excellent chart, Trump 2 begins its administration in 2025 with a CAPE ratio 37.8, the highest in modern history, surpassing the peak valuation under George W. Bush’s first term in 2001.

This record-high CAPE ratio signals a challenging environment for generating positive and above-average equity market returns. Historically, elevated CAPE ratios have been associated with subdued long-term returns as high valuations leave little room for further expansion. The U.S. stock market has consistently priced in robust corporate earnings growth, but achieving these growth rates becomes harder when valuations start at such lofty levels. In this context, the Trump 2 administration faces a critical test: steering economic policies to sustain market confidence amid such expensive conditions.

As highlighted in our recent analysis, “Presidential Stock Returns,” the new administration will likely depend on a higher-than-average inflation environment to maintain stock market momentum. A moderate increase in inflation can benefit equities by supporting corporate revenue growth, but excessive inflation risks eroding consumer purchasing power and undermining profitability. Striking this delicate balance is vital.

The data also contextualizes broader market trends. For example, CAPE ratios were substantially lower during economic recoveries such as under FDR in 1933 (7.9) or Reagan in 1981 (9.3). In contrast, the elevated valuations of 2025 reflect an era of expansive monetary policies and tech-driven growth expectations, further emphasizing the risks and constraints the administration will need to navigate. This market landscape leaves little margin for policy or economic missteps.

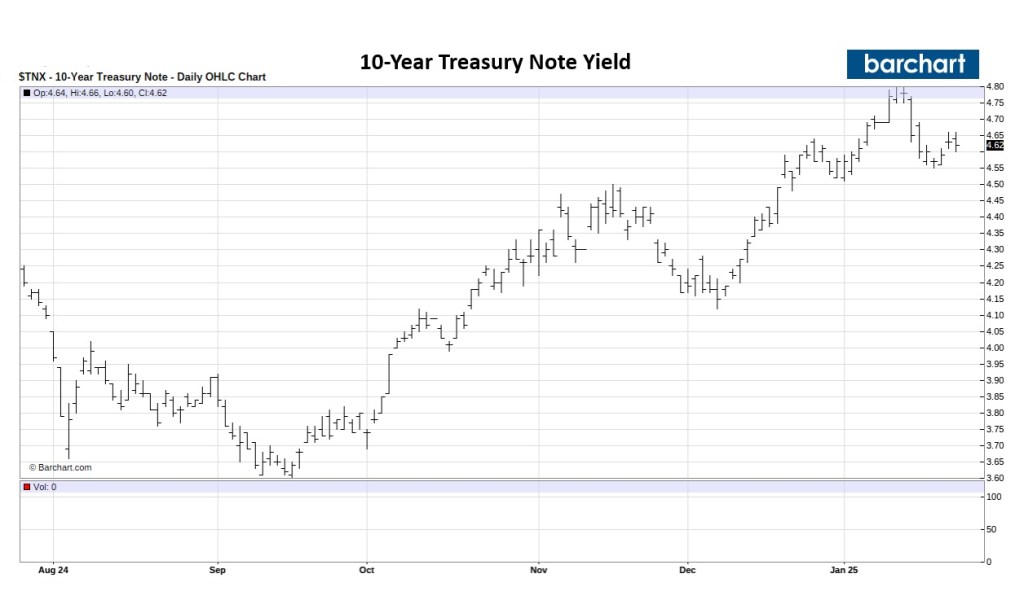

…financial markets and official economic indicators over the past few weeks have given policymakers around the world plenty to contemplate. Were the recent bond-market alarm bells a sufficient warning to Trump and his team, or will they still pursue large-scale stimulus in the form of a tax cut, across-the-board import tariffs, and a crackdown on immigration? As I wrote in November, most economists would describe this as an inflationary agenda. And now, it appears that ordinary Americans and bond markets agree. – Jim O’Neil

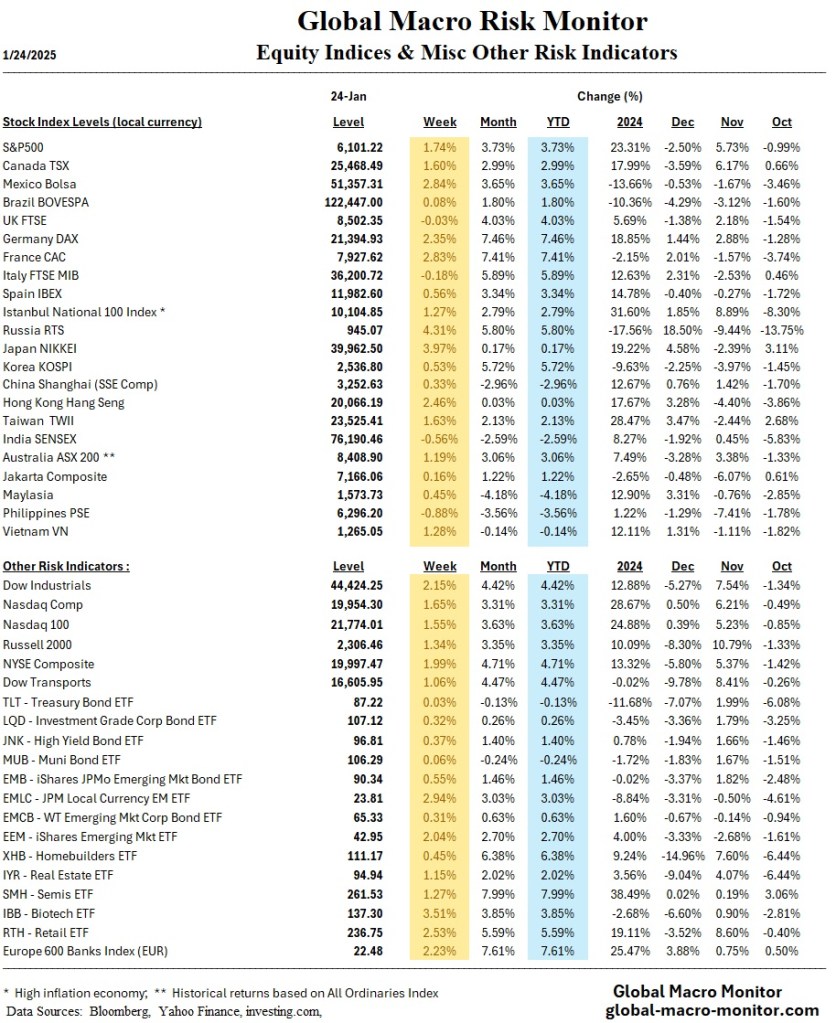

U.S. equity markets rallied, with the S&P 500 gaining 1.74% and setting a record high.

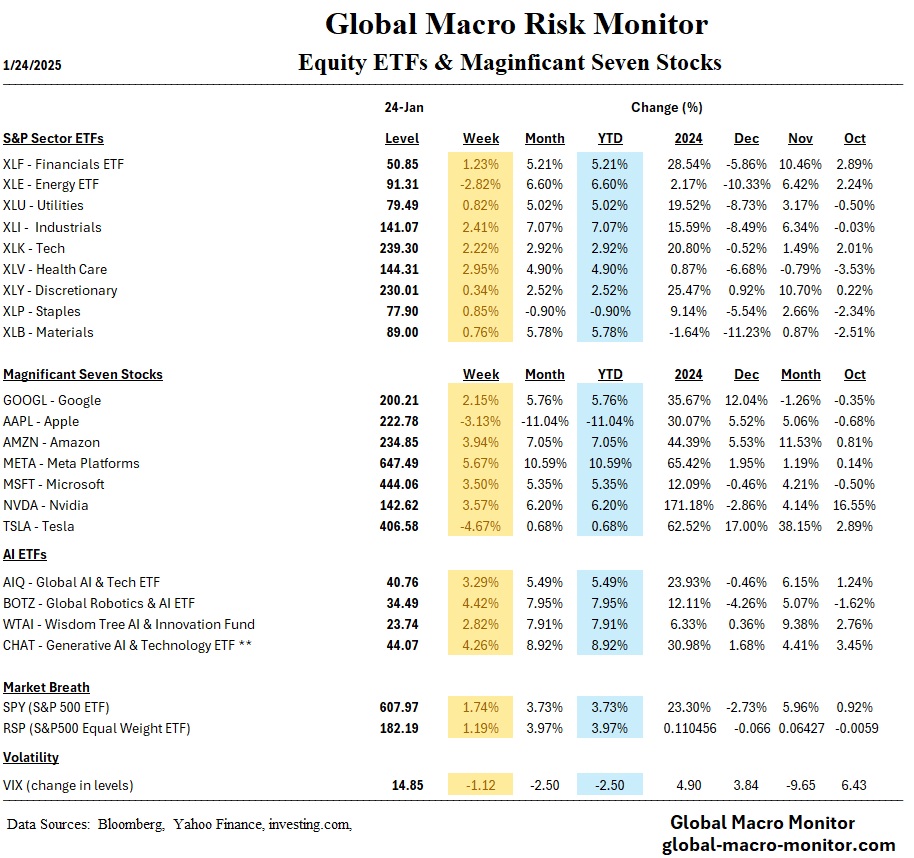

AI investments of $500 billion are expected to fuel U.S. growth.

The Bank of Japan raised interest rates to 0.5%, the highest since 2008.

Eurozone services activity expanded, but manufacturing remained sluggish.

U.S. consumer sentiment fell due to inflation and job market concerns.

Chinese youth unemployment declined to 15.7%.

The ECB is expected to continue rate cuts to support growth.

Global markets experienced a significant shift in the past week, with optimism over U.S. trade policy — no big tariff announcements — and central bank actions driving investor sentiment. In the U.S., major indices, including the S&P 500, soared to record highs, supported by renewed confidence in economic growth (Q4 GDP to be released on Thursday) and a $500 billion AI infrastructure project spearheaded by OpenAI, Oracle, and SoftBank. Growth stocks outpaced value stocks, and large-cap indices generally outperformed their smaller-cap counterparts. Meanwhile, U.S. Treasuries remained stable, though municipal bonds saw robust demand amid elevated issuance volumes.

Global Markets

Internationally, markets displayed mixed performances. European equities rose as optimism about potential European Central Bank (ECB) rate cuts grew, with Germany and France leading gains. The Bank of Japan (BoJ) made headlines by raising interest rates by 0.25 percent to 0.5%, the highest level since 2008, signaling confidence in achieving its inflation targets. This move bolstered investor optimism and lifted Japanese equities, with the Nikkei 225 climbing nearly 4%, though the strengthening yen tempered some gains for exporters. In China, equities edged higher as monetary policy remained accommodative, and U.S. trade tensions appeared to ease.

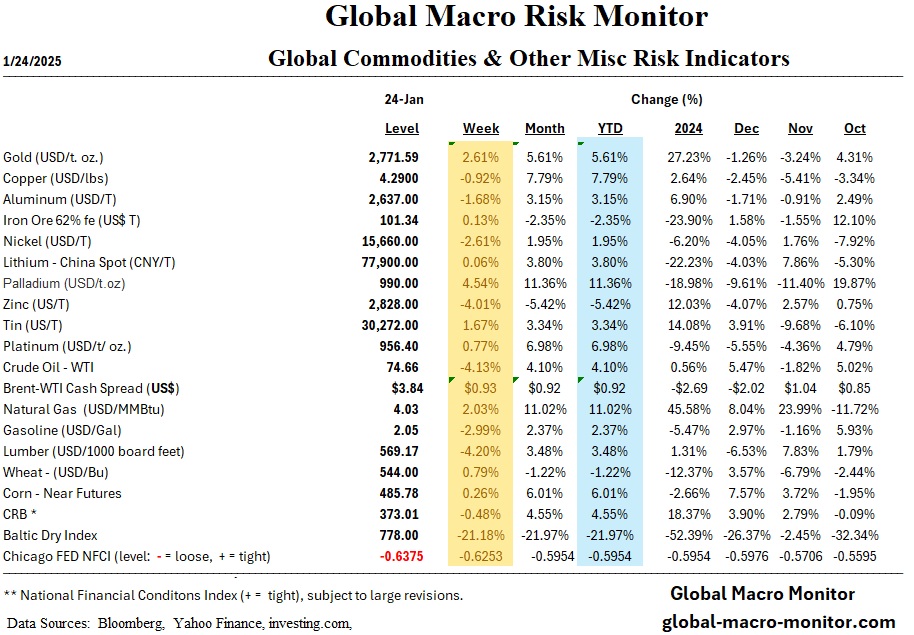

The dollar index was weaker by 1.77 percent. Mexico, Brazil, Korea, Malaysia, and Russia’s currencies rallied significantly against the dollar. Oil prices fell over 4 percent on the week and gold rose to $2,771 per ounce.

Economics

U.S.

Economic indicators reflected a mixed picture. Manufacturing activity expanded for the first time in six months, while services sector growth slowed. December’s existing home sales rose 2.2%, ending 2024 on a high note, but annual sales hit a 30-year low, weighed down by high mortgage rates. Consumer sentiment dipped, with concerns over inflation and unemployment emerging as key drivers.

Foreign

In the Eurozone, business activity showed signs of recovery, driven by modest growth in the services sector, while manufacturing remained weak. The BoJ’s rate hike reflected growing confidence in its inflation trajectory, supported by rising wages and higher consumer prices, which hit 3.0% annually in December. In China, a continued decline in youth unemployment and stable loan prime rates hinted at economic stabilization.

The Week Ahead

In the U.S., key economic data, including Q4 GDP and the Federal Reserve’s policy decision, will dominate the agenda. Markets have priced a 99.8 percent probability that the Fed will make no move. Internationally, all eyes will be on China’s PMI data, the ECB’s anticipated rate cut, and the Bank of Canada’s policy meeting, offering critical insights into global growth and monetary trends.