As Julius Caesar crossed the Rubicon River with the 13th legion into Italy to march on Rome, he turned to one of his deputies, quite possibly, Marc Antony, and made the famous remark, “alea iacta est.” Historians translate this as “the die is cast,” the decision is made, there is no going back.

Yields Cross The Rubicon

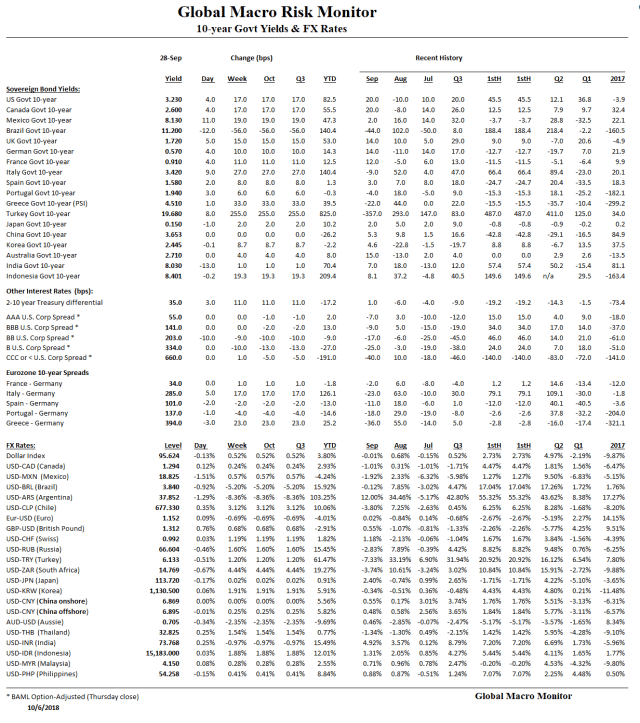

Today the U.S. bond market crossed the Rubicon with the 10-year yield breaching major resistance at, let’s call it, 3.12 percent, a high that hasn’t been seen since July 2011, ironically the month named in honor of Julius Caesar.

July 2011 was also just before or in anticipation of “Operation Twist,” the Fed’s program to manipulate longer-term rates lower.

You know what we think about the Treasury market.

We laid out all the reasons why the structural factors that have kept long-term interest rates low and risk premia suppressed are fading in our September 23rd beast of a post, The Gathering Storm In The Treasury Market 2.0.

Also, have a look at our Monday piece on the massive short build in 10-year note futures.

Though it’s too early to tell, the move in the 10-year yield today may be the signal that global bond yields are awakening from their QE-induced slumber. The flow of long-term notes and bonds is rising, as the Treasury issues more securities to finance larger budget deficits, but the big short in 10-year note futures remains, and the relative stock/float of long-term Treasuries is still low.

It may take a few days of trading above the breached resistance level to bolster the confidence of the bond bears.

Nevertheless, a more “normal” long-term yield would be closer to a 3 percent real rate, which is more than a chip shot from here, and, at the very least, two drivers away from today’s 3.16 percent close. We expect the first drive to hit the the 4.25 to 4.40 percent range, which is a measured move of the inverse head and shoulders pattern in the above chart, probably sooner rather than later.

Even the 10-year Japanese bond yield is pressing up against two-year highs, albeit at a poultry 15 bps.

QE Induced Asset Market Psychosis

Supply shortages, induced mainly by central bank quantitative easing have been a major factor driving asset markets, in our opinion. Not all, but a big part.

Risk-free bonds have been in short supply as central banks have hoovered up their home country government bonds with quantitative easing.

Equity Float Shrinkage

The float of total U.S. equities has shrunk dramatically, in part, due to cheap financing to fund share buybacks. The technical shortage of stocks have helped boost U.S. equity markets and killed off the most of the bears and short sellers.

We have no idea if short sellers can push the market lower on a sustained basis as rates rise, forcing some real selling in the near term. Probably not, if we define near term, say, as in the next month.

It’s possible, but our recency bias tells us no, unless rates move to our target range more rapidly than we even expect. Today’s increase in yields did cause selling into the close.

Source: Yardeni Research

Housing Market

Even the housing market suffers a dearth of supply.

Private equity, now the largest single holder of single-family residential real estate, has taken a massive supply of homes off the market and converted them to rentals, partly due to the lower cost of capital caused by the manipulation of the Treasury yield curve. Will these investors start to sell down their inventory as rates move higher, or just continue to raise rents, which could create a real political problem?

…one-fourth of the country’s single-family rental homes are now owned by institutional investors, with more than 200,000 families paying their rent to just nine giant Wall Street-backed firms. According to a report by the Harvard Joint Center for Housing Studies, the majority share of all U.S. rental units (52.2 percent) are owned by institutional investors, and the investor-owned share of single-family homes increased by nearly 40% from 2001 to 2015.5 – ACCE

We suspect a populist message from a 2020 presidential candidate railing against the “Wall Street firms, who were bailed out then bought your homes in bankruptcy and are now raising your rents” would resonate with the hoi polloi. Even if it’s true, or not.

In California, rent increases by some of the largest Wall Street landlords have been astronomical. For example, Colony Starwood Homes reported that in Northern California rental renewal rates increased by 9-13%, the largest in the nation. This means that if tenants already living in a Colony Starwood home want to continue to rent, they must pay between 9 to 13% more each year. A survey conducted in early 2017 of Los Angeles County tenants renting from Invitation Homes and Colony Starwood shows consistently high rental increases in the Southern California market as well. Of the 100 tenants surveyed, 77% reported rental increases and the average reported increase was 9% or $171 per month. – KCET

Does “truth” even matter today? It’s only true if you believe it to be true in our postmodern Trumpian era.

Vulnerable Markets

The structural factors that have kept U.S. long-term interest rates low are now fading and yields are set to move significantly higher. That is back to normal.

The markets, which look the most vulnerable on a technical basis in the near-term, are those that have seen a significant increase in supply since the financial crisis. Such as emerging market debt and U.S. corporate bonds and debt at the lower end of the investment grade spectrum.

Commercial Real Estate

Also keep the commercial real estate sector on your radar,

With investors acquiring $30.5 billion in industrial assets in the first half of 2018, JLL’s H1 2018 U.S. Investment Outlook report notes that the industrial sector is on pace for a new record year in terms of transaction volume and is expected to surpass the previous high point of $67.8 billion in 2015. That momentum, coupled with $20 billion in large scale transactions that are under contract and set to close in the second half of 2018, serves as evidence of the intensity of investor competition for industrial assets.

As a result, the national average cap rate across all classes of industrial assets has dipped to a record low of 7.0 percent. Average cap rates are even lower in the five industrial markets with the most supply constraints: 4.5 percent in Orange County, Calif.; 5.0 percent in San Francisco; 5.2 percent in Los Angeles; 5.3 percent in the Inland Empire and 5.4 percent in Seattle.

At the peak of the last cycle, the average cap rate for industrial assets was 7.2 percent, according to Chang. But starting with 2010, when the figure reached 8.7 percent, industrial cap rates have continued to drop, driven by economic expansion and growth in e-commerce sales. – National Real Estate Investor

Recall our “Cranes of Dubai” comment after returning from summer break.

Euro Sovereign Bonds

The market to closely monitor now is European sovereign bonds. The ECB’s QE is set to end in December and inflationary pressures are building. The yield spread between U.S bond and German bunds is approaching long-term highs.

Source: Frederik Ducrozet

Italy is the wild card, but we suspect the government has enough leverage with the EU due to the country’s importance in the euro and the sheer size of its bond market. Though it will upset many Germans, the EU will likely calculate that bigger budget deficits in Rome are not worth blowing up Europe. In other words, lot’s of noise to come.

We expect European interest rates to rise significantly over the next year, reinforcing the global bond bear market.

Upshot

All of the above will take time to unfold, with the usual ebb and flow of markets, providing traders with many profitable opportunities.

Rome wasn’t built in a day. Alea iacta est!